Exchange arbitrage, is it worth digging into?

Your trading scheme involves getting quotes from a faster broker and opening orders from a slower broker. Legally, there is no violation because you take several brokers, compare quotes and make a trade with one of them. Both of them do not know about each other, the order is the same, there are no violations.

In terms of technical possibility it is there too. You need to modify two terminals. Choose two brokers, one is the main and one is a dependent. On the main one we will receive the quote and on the second one we will implement it. To check the quote and open quotes instantly without losing precious fractions of a second, the entire system should be implemented on net framework 3.5 or higher. Thus, we will obtain one working system with two terminals, just with two brokers and different accounts.

What else we have to consider.

1. Your location and ping from you to broker #1 and to broker #2.

2. What kind of hardware you have. If even a 2004 Pentium 4 will do for manual trading, then you have to build something faster.

That's all in a nutshell.

Now look at the result of this work = 0 or so, since we need to optimize it.

1. Optimize the ping.

We find out where the server of our broker is, rent a VPS server somewhere nearby and I think we have to do this close to the main broker.

2. Rent a server, we solved the problem with the hardware (if not stingy on the parameters). But this is not enough for us, with a normal connection to the broker, the client-broker-broker-broker-client scheme of work. You need to exclude the broker from the link to further reduce the ping, the scheme is client-broker-broker. You should use PLAZA2 protocol service and in this case the broker will be informed about your trades and the orders will be immediately sent to the exchange in the market.

Now we consider the main question is the financial component, so to speak, of this startup.

1. The cost of the programmer. For a good programmer. Who will be able to assemble two terminals in one system working with framework, and give all this API to work with plaza 2 through the CGate protocol.

2. Plaza2 service itself is paid, if I'm not mistaken about 3000r monthly.

3. You need an unlimited data plan. Your idea is only scalping and it's a lot of deals per day. If I am not mistaken brokers unlimited costs about 50k RUR. (I can't say for sure).

This is the roughest and most superficial plan.

If you go deeper and take a more ideal model for installation of such system, you need to put it in the collocation zone of the exchange. And rent a server there is a completely different cost. In this case, the time is reduced to nanoseconds.

Your trading scheme involves getting quotes from a faster broker and opening orders from a slower broker. Legally, there is no violation because you take several brokers and compare quotes and make a trade with one of them. Both of them do not know about each other, the order is the same, there is no violation.

100ms, for a real account, is somehow too much. On forex at my broker ping 100-150ms on demo account, on real account less than 40ms. Now I am testing on another demo account with 50ms on the real account and they promise even less, within 10ms.

For the perceptibility of delays I can not say, in theory you need to have a minimum ping between the receipt of quotes from the main broker and you, between you and the dependent broker as a minimum ping, but between the dependent broker and the exchange should be higher than the ping of the main and you. Then I suspect that there is a point in these delays.

Specify whether you are interested in such a scheme for forex or for the exchange?

100ms, for a real account, is somehow too much. On forex at my broker ping 100-150ms on demo account, on real account less than 40ms. Now I am testing on another demo account with 50ms on the real account and they promise even less, within 10ms.

For the perceptibility of delays I can not say, in theory you need between the receipt of quotes from the main broker and you have a minimum ping, between you and the dependent broker as a minimum ping and here between the dependent broker and the exchange should be higher than the ping of the main and you. Then I suspect that these delays make sense.

This scheme is interesting for Forex or for Stock market?

For exchange, for forex I have already done. I think, 100 ms ping will be not less, because both terminals will stand in one place. (+ I live in Tomsk. But you can rent a WPS closer to Moscow.) Between them, they are very fast exchange, but the ping to the servers + the execution time is yes...

It turns out that in this way, the dependent broker (or the main one) must have a delay to the servers of the exchange. For example, if you take forex, there are different liquidity providers, everything is decentralized. There may be delays for other reasons, and in general, different quotes. And in the case of Forts, there is only one exchange...

The exchange is the same and I think it is the work between the broker and the exchange that counts.

There is also a nuance. Of course I can't say for sure, because I don't trade on the exchange, but there are also rules for execution of orders in the market, take it into account.

If I'm not mistaken, the first to execute is the one that was put in the book the last, and it also takes into account the volume of the order, those that are larger they are executed in the first place. If I'm not mistaken here the time for order execution is also necessary to take into account. Since you will always lose to similar schemes that work through Plaza2 and even more worth collocation exchange servers.

I read that there are robots set up to put their request at the last micro or even nanoseconds. To be executed in the first place.

I have got a similar system, I just need to configure it and find 2 brokers with delay.

It would also be interesting to see the results of your system.

If you don't want to do it here, please send me an answer in a private message.

The exchange is the same and I think it is the work between the broker and the exchange that counts.

There is also a nuance. Of course I can't say for sure, because I don't trade on the exchange, but there are also rules for execution of orders in the market, take it into account.

If I'm not mistaken, the first to execute is the one that was put in the book the last, and it also takes into account the volume of the order, those that are larger they are executed in the first place. If I'm not mistaken here the time for order execution is also necessary to take into account. Since you always lose to similar schemes that work through Plaza2 and more so in collocation exchange servers.

I read that there are robots set up to put their request at the last micro or even nanoseconds. To be executed in the first place.

I have got a similar system, I just need to configure it and find 2 brokers with delay.

It would also be interesting to see the results of your system.

If you don't want to do it here, please send me an answer in a private message.

For forex, I downloaded a sample here a while ago https://www.mql5.com/ru/forum/72662/page5.

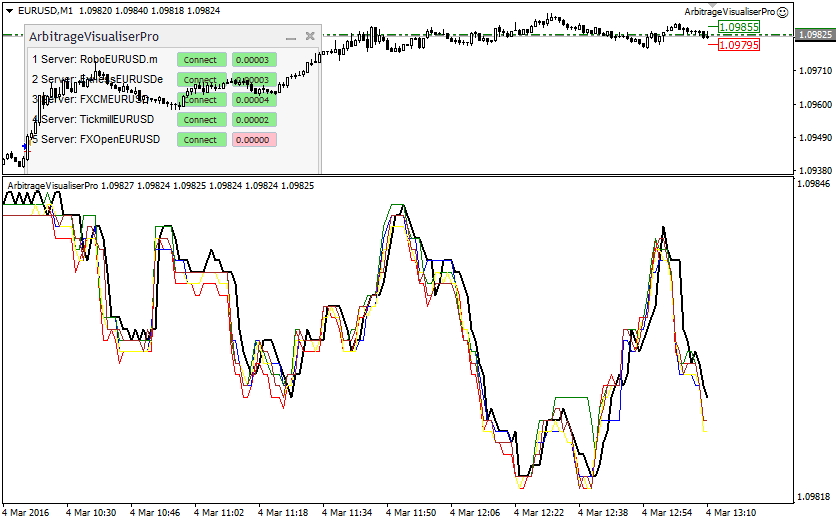

I have not finalized the system yet, especially how to determine the quote lag more accurately. Now my system looks like this: I connect to several brokers, the indicator displays tick-plots of all brokers, and the lag is clearly visible. The Expert Advisor selects the broker that is ahead of the one we trade on. At a certain lag of one of the subordinate brokers to the current one trades are opened.

Lags do happen, it's already seen. But slippages too :) In the end a lag of 3 points can be compensated by a slippage. But there are more profitable trades, though loss trades are more powerful.)

I do not have any results yet, I am experimenting. But the system potential is evident in that there is no need to reinvent the wheel in the form of an amorphous strategy. The rules are clear, the important thing is to implement them properly and find brokers.

I don't really believe in conspiracy theories and there is nothing to hide. I have seen several such systems for sale and monitoring. They all die for different reasons, mainly because of sticks in the wheels on the part of dealers. I have already cited one link before - the guy simply did not get his money back. The fact that his system is arbitrage is obvious; all you have to do is analyse the trades.

- www.mql5.com

...

...

I agree, the potential is there.

I haven't tested my system yet, but if I don't get bored and get stuck in some shooting at the weekend I'll try to set it up and test it. I'll share the results later.

Are you guys really gifted or are you just pretending? Execution on moex is strictly centralised. All transactions are consolidated in a single exchange core. Hence, there is no concept of delays in quotes, like on decentralized Forex, where different liquidity providers offer rates. Man, you should have studied the issue first, and then invented the "infrastructure".

I wonder if anyone has encountered lagged quotes from different brokers on FORTS? Is it worth digging in this direction, or everything has been clear for a long time and there is no need to play around? :)

Are there any differences or delays in quotes from different brokers? How it all corresponds to the rules of the exchange, will this trading be cheating or everything is within the law, "the one who had the time, ate it"?

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

I wonder if anyone has encountered lagged quotes from different brokers on FORTS? Is it worth digging in this direction, or everything has been clear for a long time and there is no need to play around? :)

Are there any differences or delays in quotes from different brokers? How it all corresponds to the rules of the exchange, will this trading be cheating or everything is within the law, "the one who had the time, ate it"?