The current JPY decline offers JPY buying opportunities. Thetrend towards a higher JPY will remain intact unless Japan radically changes its monetary policy strategy to boost inflation expectations. An example of such change would be if Japan were to introduce a helicopter money programme that would bea form of debt monetization, however, we are not expecting this so the JPY uptrend should remain in place. We would sell against the 105.55 level in USDJPY.

This morning Japan’s authorities were distancing themselves from the idea of helicopter money. The Sankei newspaper reported earlier that officials around Abe are considering helicopter money as a policy option. Government adviser Hamada called helicopter money a ‘very risky gamble’, noting history illustrating dangers of unstoppable inflation. These comments suggest that the costs of a potential failure of ‘Abenomics’ are not yet high enough for Japan taking the next step towards an even more aggressive monetary policy approach. When Abe came to power its ‘three arrow’ policy approach was revolutionary enough to push inflation expectations higher and bond yields lower allowing via lower real yields the JPY to weaken. The three arrows contained expansionary monetary policy, an initial impulse to kick start the economy and structural reforms. The first two arrows were easy to implement while structural reforms were implemented slowly. History may judge that it may have been the slow implementation of structural reform putting Abenomics at risk.

The Hamada comments making clear that there will be no helicopters flying over Tokyo any time soon made markets speculate about a ‘soft helicopter’ approach with fiscal authorities issuing a‘bold’ fiscal package and the BoJ taking the opportunity to use increased JGB issuance to prop up the volume of QE, thus adding to the stock of base money. Fiscal authorities placing the announcement of the fiscal package near the 29 July BoJ meeting seems to support this view. The bad news for JPY bears is that there is very little substance to this argument in respect of its impact on the JPY. For QE to work it must rely on the ‘announcement effect’ to boost inflation expectations and the related bond supply absorbing effect pushing nominal yields lower. The ‘announcement effect’ has become smaller as initial QE programs failed to lift inflation sufficiently. Instead, core inflation has eased once again dragged lower by a 20% decline of import prices. The Japanese yield curve is flat and mostly negatively yielding. Pushing bond yields lower via additional QE is unlikely to impact the yield curve sufficiently to weaken JPY. Moreover, falling bond yields tend to undermine the profitability of bank and insurance companies which itself weakens the local credit multiplier.

For the JPY to weaken, inflation expectations need to rise thus pushing real JPY yields lower. This takes us to the next option, namely boosting inflation expectations via pushing asset prices higher. Nowadays, Japan’s private sector is more exposed to asset holdings compared to pre-Abenomics days. Hence ,an asset price boom may create an inflation expectation supportive impact weakening the JPY from this angle. This approach would require the BoJ to use additional ETF purchases. Here too we may have to distinguish between initial and long-term effects. Initially, a boost of JPY denominated risky assets could weaken the JPY as the FX market has been often used as a ‘quasi-hedge’ for asset long positions. An asset price boost could spark foreigners to reduce their JPY exposure, which was previously used as a risk hedge in their portfolio, and would send the JPY lower initially. However, a valuation driven boost of asset prices bears additional long-term deflationary risks should the asset price boost not find support via higher earnings.

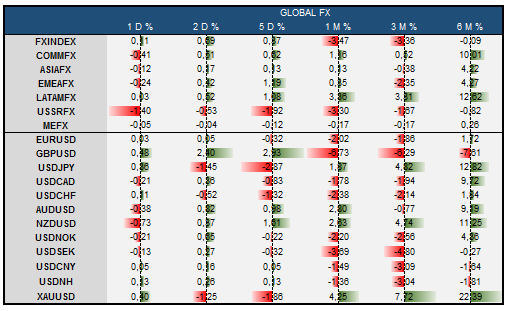

Yesterday’s GBP rebound triggered by hopes the UK economy may not suffer full ‘Brexit blues’ as government stability returns with the steady hand of incoming PM Theresa May has helped the JPY to weaken too as GBP has been an important carry vehicle of Japan based retail investors. However, we think the GBP rally will run out of steam once investors learn that the economy is likely to slow down from the investment side, weakening employment and then finally consumption. Yesterday’s upbeat headlines suggesting strong post Brexit retail demand provided the excusefor a sharp GBP short-covering rally, but thetrend remains down. Note that we believe it is too early to make consumption related judgements from so few data points. The chart below shows that previous episodes of GBP weakness developed similar patterns compared to yesterday’s move but did not indicate a trend reversal.