Treasuries posted a substantial belly-led rally Thursday, as more modest gains of 2 to 3 bp along the curve through most of the day accelerated after 2:30 into month/quarter/Japanese fiscal year end, leaving yields down as much as 5 bp at 3:00 and a bit more in late trading. There wasn’t any further near-term adjustment in Fed pricing in futures, so a 3 bp 2-year Treasury rally widened the 2-year swap spread 2 bp to 12 bp. The market continues to price only about a 25% chance of a June rate hike and 75% chance of one hike by year end going into payrolls on Friday. The mediumterm Fed rate view took another meaningful step down, though. A 6 bp rally in the Jan 19 fed funds contract to 0.975% now prices only two more 25 bp hikes through 2018 as more likely than three, and the 5-year/5-year forward swap rate rallied 5 bp to a three-week low of 2.14%, closer to the record low close of 1.97% on February 11 than the 2.70% it entered the year. Equities, credit, and oil prices were little changed on the day, and the broad trade weighted dollar fell a bit more on strengthening in the renminbi and euro, but there was a modest pullback in TIPS inflation breakevens after big gains Tuesday and Wednesday. The mild partial reversal in breakevens accounted for a portion of the rally in nominals, but the market-implied longer-run neutral real rate also continued to decline, indicating rising conviction that the Fed is right to be increasingly concerned that their base case outlook for a gradual drift higher in the neutral real fed funds rate isn’t going to happen. Economic data released Thursday had no market impact as investors focused on positioning for month end and payrolls. Jobless claims rose to a two-month high in the latest week, and the Challenger survey showed a another large rise in job-cutting plans, warning of less favorable job growth numbers going forward. For Friday’s employment report, however, claims hit a record low earlier in the month during the survey week for March payrolls, and the weather was quite favorable after having been a drag in a couple of big March payrolls misses in recent years. A rebound in the Chicago PMI, meanwhile, added to a across the board improvement in the early regional surveys for March, supporting expectations for the ISM to move above 50. At 3:00, benchmark nominal Treasury yields were 3 to 5 bp lower after a lot of month-end related buying kicked in from a range of investors after 2:30, extending what had been more modest gains along the curve to that point. The 2-year yield fell 3 bp to 0.73%, 3-year 4 bp to 0.86%, 5-year 5 bp to 1.22%, 7-year 5 bp to 1.55%, 10-year 4.5 bp to 1.78%, and 30-year 3.5 bp to 2.62%. While there was a burst of portfolio adjustments Thursday related to month end, generally our desk sees investor positions as quite light going into payrolls and generally focused on looking for carry trades on the curve or in volatility, with this employment report seen as one of the least important recent ones and unlikely to change much in the near-term Fed or market outlook. The lagging performance of TIPS breakevens was driven by real yield selling at the long end that our desk saw as just profit taking and position lightening ahead of Friday. Benchmark breakevens were down 1 to 2 bp, with 10’s lagging, but that still meant another day of declining real yields to the lows in nearly a year, with the 5-year yield down 3 bp to -0.41%, 10-year 2.5 bp to 0.15%, and 30- year 1.5 bp to 0.83%, accompanying the market’s further ratcheting down the implied longer-run neutral/terminal fed funds rate. The 4 bp decline in the 5-year/5-year forward swap rate to 2.14% came with a slightly smaller 3 bp drop in the 5-year/5-year forward inflation swap to 2.07%

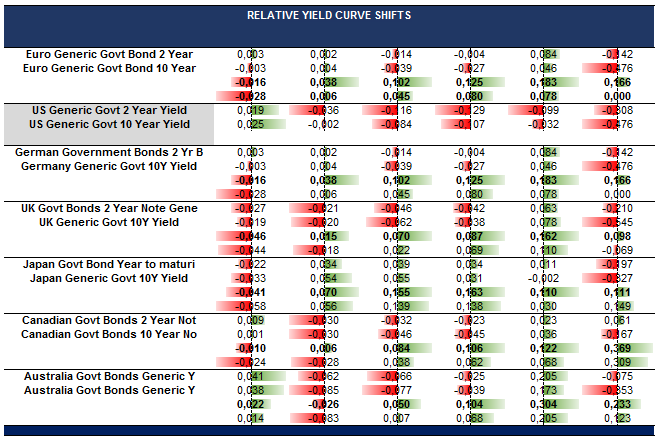

Trading Guide")