FX Outlook 2015 – General (Weekly) Update – 25 April 2015

adt_fx FX Outlook 2015 – General (Weekly) Update – 25 April 2015

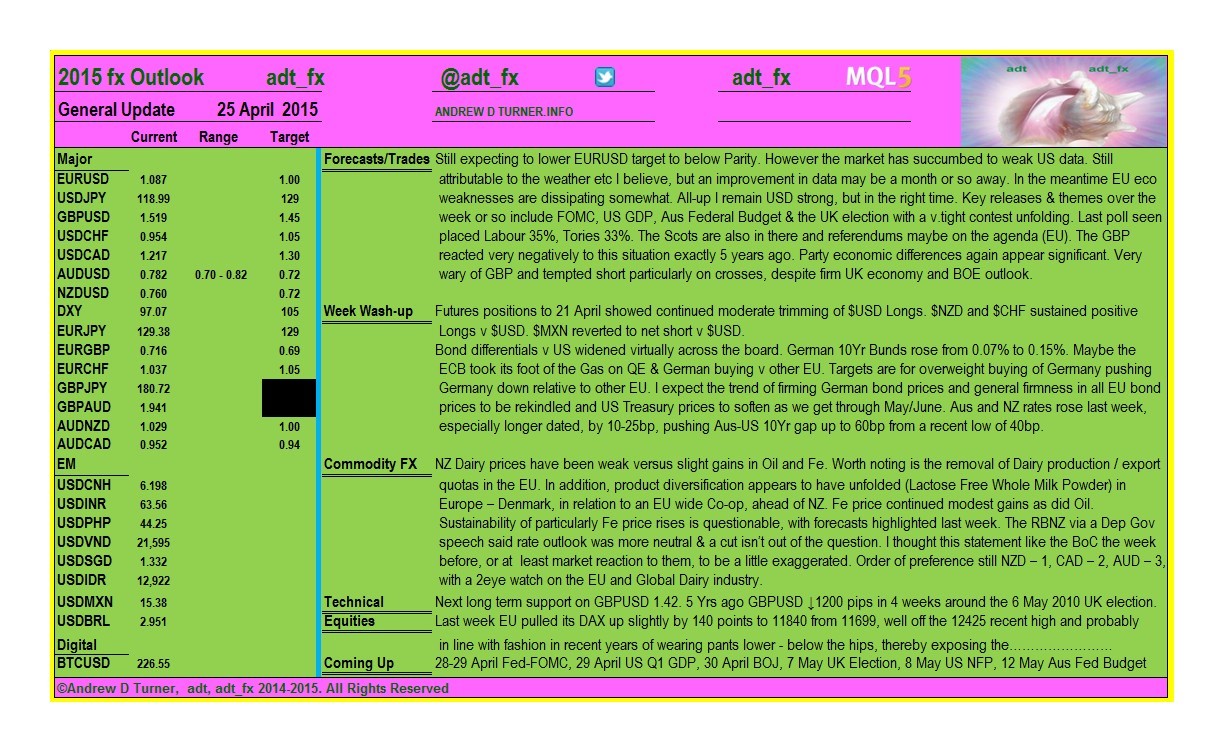

Forecasts, Trades & Outlook - Summary

I Still expect to lower EURUSD target to below Parity. However the market has succumbed to weak US data. Still attributable to the weather etc I believe, but an improvement in data may be a month or so away. In the meantime EU economic weaknesses are dissipating somewhat. Regional economic momentum appears to have swung a little toward EU / UK relative to North America, although again this may be largely attributable to weather obviously in addition to Oil, both perhaps somewhat temporary. All-up I remain USD strong, but in the right timeframe.

Key releases and themes over the next week or so include FOMC, US GDP, BOJ, deadline for Greek Reform Outline by early May, Aus Federal Budget and the UK election with a very tight contest unfolding. Last UK election poll seen, placed Labour 35%, Tories 33%. The Scots are also in there and referendums maybe on the agenda (EU and Scotland). The GBP reacted very negatively to this situation exactly 5 years ago. Party economic differences again appear significant. I am very wary of GBP and tempted short particularly on crosses, despite firm UK economy and BOE outlook.

The Fed-FOMC is unlikely to shed anything too significant this week. My sense has been that a significant proportion of the Fed has been considerate of monetary policy normalisation. My preference has been to distinguish between normalisation and tightening although I don’t think the Fed has taken this step………….yet. I would make the distinction because the US key discount rate of 0-0.25% seems anomalous given economic recovery and relative to say Canada and UK, both of which have seen some sort of economic recovery as well. BoC and BOE key rates are both 0.5%. I don’t see that US monetary policy should be easier at this stage than both these, although BOE continues some sort of APP / QE as well. So US monetary policy normalisation would appear in order. What then unfolds regarding US monetary policy tightening could be considered a separate consideration. This attitude would possibly ensure a rate rise of 25bp in June-ish, followed by tightening, if it is in order - dependant on data, through H2 2015. In the absence of the US taking this distinctive stance and official Fed interest rate rises remaining rolled effectively into the broad category of tightening, and therefore being data dependant, the first rate rise might be any time June-Dec 2015, in turn perhaps dependant on how quickly the US economic heaters crank up after being frozen for a few months.

The BOJ has its Semi Annual Outlook meeting on 30 April. It will be reviewing its inflation targeting and outlook again. The Japan economy remains a little sluggish to me and ex the 2014 sales tax increase, which has probably served to create a volatility around consumer and business planning and expectations and ultimately dampen the inflation outlook, the overall outlook is tepid at best; Japan economic gains being a little sporadic and the balance of trade gains looking to me to be in large part through import reduction, which is probably due to rising import prices through yen depreciation, but which in any event reflects a weakness in domestic demand. Accordingly I don’t know the BOJ is going to be glowing about achieving their targets. At the same time Japan BOJ QE is already monstrous relative to GDP and I don’t see the market will be greeted with further easing. A huge amount is already in place taking into account Government Pension Fund adjustments etc as well.

Last Week Wash-up

USD closed the week out near its one week lows. Futures positions to 21 April showed continued moderate trimming of $USD Longs. $NZD and $CHF sustained positive Longs v $USD. $MXN reverted to net short v $USD.

Bond differentials v US more or less widened across the board. German 10Yr Bunds rose from 0.07% to 0.15%. Maybe the ECB took its foot of the Gas on QE and German buying versus other EU countries. Targets are for overweight buying of Germany pushing German rates down relative to other EU rates. I expect the trend of firming German bond prices and general firmness in all EU bond prices to be rekindled and US Treasury prices to soften as we get through May. Australian and NZ rates rose last week, especially longer dated, by 10-25bp, pushing Aus-US 10 Year gap up to 60bp from a recent low of 40bp.

Commodity FX

NZ Dairy prices have been weak versus slight gains in Oil and Iron Ore. Worth noting is the removal of Dairy production / export quotas in the EU in April. In addition, product diversification appears to have unfolded (Lactose Free Whole Milk Powder) in Europe – Denmark, in relation to an EU wide Co-op, ahead of NZ. Iron Ore price continued modest gains last week as did Oil. Sustainability of particularly Iron Ore price rises is questionable, with forecasts highlighted last week ($GS and $C $30-$40 pt). The RBNZ via a Deputy Governor speech said the NZ rate outlook was more neutral and a cut isn’t out of the question. I thought this statement like the BoC the week before, or at least market reaction to them, to be a little exaggerated. My order of preference across the major commodity currencies is still NZD – 1, CAD – 2, AUD – 3, but with a 2eye watch on the EU and Global Dairy industry.

Technical

Next long term support on GBPUSD is 1.42 as I highlighted earlier this year. Five Years ago GBPUSD fell 1200 pips over four weeks around the 6 May 2010 UK election.

Equities

Last week the Nikkei 225 broke through and sustained 20K. The EU pulled its DAX up slightly by 140 points to 11840 from 11699, well off the 12425 recent high and probably in line with fashion in recent years of wearing pants lower - below the hips, thereby exposing the……………………………… As I have previously suggested, the EU, like a lot of other regions / countries remains torn between EUR depreciation or appreciation and Equities appreciation or decline, respectively. I don’t think we will see real stability in exchange rates or equities. This then begs the question of what happens with effectively liquidity driven price changes generating a wealth effect, or not? I believe ECB QE will continue to drive EURUSD decline, when the US economy is feeling a little warmer, and that there will be further EU equities rallies and some sort of wealth effect following. The temptation of this outcome is probably too great to the relevant authorities for them to seek anything else, particularly given EU recovery is in all reality still only embryonic and therefore far from cemented and possibly if anything still a little fragile.

Coming Up

28 April UK Q1 GDP, 28-29 April Fed-FOMC, 29 April US Q1 GDP, 30 April BOJ, 1 May Labour/Workers Day Holidays, Early May Greek Reforms Outline, 5 May Aus RBA MPM, 7 May UK Election, 8 May US NFP, 12 May Aus Fed Budget

")

{kind=link}