FX Outlook 2015 – General (Weekly) Update – 18 April 2015

adt_fx FX Outlook 2015 – General (Weekly) Update – 18 April 2015

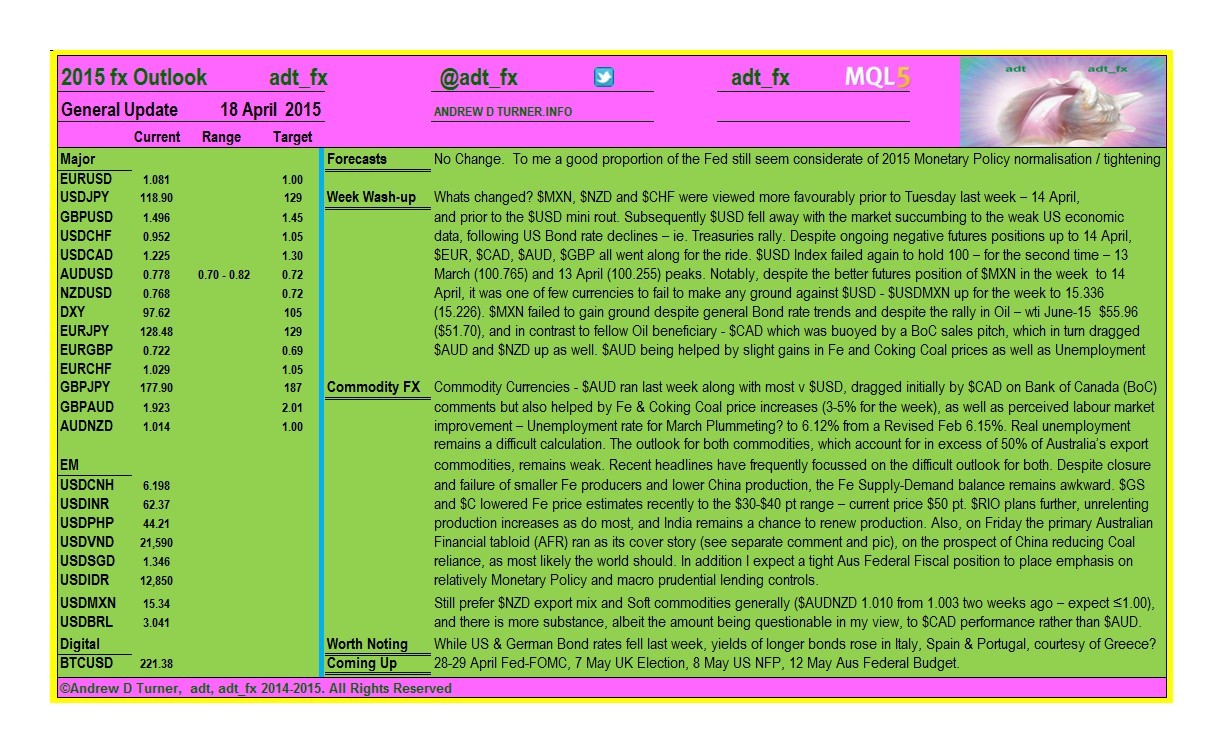

No Change. Still expecting to lower EURUSD target to below Parity. Despite relative AUD strength last week, prefer NZ export composition and soft commodities generally and also expect to lower AUDNZD target to below Parity. To me a good proportion of the Fed still seem considerate of 2015 Monetary Policy normalisation / tightening.

What has changed? $MXN, $NZD and $CHF were viewed more favourably prior to Tuesday last week – 14 April, and prior to the $USD mini rout. Subsequently $USD fell away with the market succumbing to the weak US economic data, following US Bond rate declines – ie. Treasuries rally. Despite ongoing negative futures positions up to 14 April, $EUR, $CAD, $AUD, $GBP all went along for the ride. $USD Index failed again to hold 100 – for the second time – 13 March (100.765) and 13 April (100.255) peaks. Notably, despite the better futures position of $MXN in the week to 14 April, it was one of few currencies to fail to make any ground against $USD - $USDMXN up for the week to 15.336 (15.226). $MXN failed to gain ground despite general Bond rate trends and despite the rally in Oil – wti June-15 55.96 (51.70), and in contrast to fellow Oil beneficiary - $CAD which was buoyed by a Bank of Canada (BoC) sales pitch, which dragged $AUD and $NZD up also. $AUD being helped by slight gains in Fe and Coking Coal prices and unemployment.

Commodity FX - Commodity Currencies - $AUD ran last week along with most v $USD, dragged initially by $CAD on BoC comments but also helped by Fe and Coking Coal price increases (3-5% for the week), as well as perceived labour market improvement – Unemployment rate for March Plummeting? to 6.12% from a Revised Feb 6.15%. Real unemployment remains a difficult calculation. The outlook for both commodities, which account for in excess of 50% of Australia’s export commodities, remains weak. Recent headlines have frequently focussed on the difficult outlook for both. Despite closure and failure of smaller Fe producers and lower China production, the Fe Supply-Demand balance remains awkward. $GS and $C lowered Fe price estimates recently to the $30-$40 pt range – current price $50 pt. $RIO plans further, unrelenting production increases as do most, and India remains a prospect to renew production. Also, on Friday the primary Australian Financial tabloid (AFR) ran as its cover story (see twitter @adt_fx comment and pic), on the prospect of China reducing Coal reliance, as most likely the world should. In addition I expect a tight Aus Federal Fiscal position to place emphasis on relatively easy Monetary Policy and macro prudential lending controls.

Still prefer $NZD export mix and Soft commodities generally ($AUDNZD 1.010 from 1.003 two weeks ago – expect ≤1.00), and there is more substance, albeit of questionable amount in my view, to $CAD performance relative to $AUD.

EM FX Amidst the turmoils in Global Financial Markets, which Central Banks have done incredibly well to control at all, I have been interested in $PHP and $INR Long positions, probably against $EUR and / or $AUD. They are two economies achieving 6%+ GDP growth, and which are net oil importers, thereby deriving considerable benefit from the lower oil prices, and are relatively stable by EM terms. These positions would have worked so far this year although less so last week with the two – Majors – correcting bouncing. EM Debt generally is some sort of issue, as is General Market Sentiment and the “Safe Haven” concept. Yemen, Iran and EU-Greece negotiations (technical talks on putting together Greek Reforms were occurring this weekend) remain concerns. So I am just having trouble pushing these positions over the line. Perhaps better safe than sorry in market conditions like these.

Technically Speaking

USD Index failed at 100 for the second time - 13 March (100.765) and 13 April (100.255) peaks.

DAX also failed at 12,425 twice – in the one week – on consecutive days.

Equities Last week EU had its DAX pulled down by the rising $EUR and despite falling German bond rates. DAX ↓700+ from 12.4K to 11.7K last week. Other Equities markets have also come under pressure including throughout EU. Equities globally are interestingly placed with growth concerns, earnings impact from currency translation effect in US, rising oil price? and the most recent rises in QE country currencies; Probably with a backdrop of full-ish valuations? There may be a lull in QE driven liquidity and foreign currency translation earnings effect which has been driving Equities Markets in different Regions at any time, for three years? Which is better, the Smoke & Mirrors set to derive a Wealth Effect and which Equities Managers Love / Or Real Currency-Unadjusted Earnings Growth? And are EU Equities Markets now inversely hinged to the $EUR for the next 18 months? And what effect via Wealth-Effect does this then have on EU economies? And what of the Nikkei225 hitting up against 20K amidst Japans’ massive QE (relative to GDP) and while the Japanese economy, in broad terms, languishes?

So what do we have? “The Best of Both Worlds? And “The Magic Pudding.” Or “Creeping Reality.” The world is awash with liquidity which moves at the speed of lightyears and it is effecting all markets – Fixed Income, Equities, FX and probably Commodities amongst others. Where will it head next?

Coming Up 23 April PMI's Manufacturing, 28-29 April Fed-FOMC, 29 April US Q1 GDP, 7 May UK Election, 8 May US NFP, 12 May Aus Federal Budget

")

")

{kind=link}