Unisciti alla nostra fan page

- Visualizzazioni:

- 7266

- Valutazioni:

- Pubblicato:

-

Ti stai perdendo delle opportunità di trading:

Ti stai perdendo delle opportunità di trading:- App di trading gratuite

- Oltre 8.000 segnali per il copy trading

- Notizie economiche per esplorare i mercati finanziari

Registrazione AccediAccetti la politica del sito e le condizioni d’uso

Se non hai un account, registrati -

Hai bisogno di un robot o indicatore basato su questo codice? Ordinalo su Freelance

Vai a Freelance

Hai bisogno di un robot o indicatore basato su questo codice? Ordinalo su Freelance

Vai a Freelance

The idea and the simplest algorithm are provided in the article "Random decision forest in reinforcement learning"

The library has advanced functionality allowing you to create an unlimited number of "Agents".

In addition, variations of the "Arguments group accounting method" are used

Using the library:

#include <RL gmdh.mqh> CRLAgents *ag1=new CRLAgents("RlExp1iter",1,100,50,regularize,learn); //created 1 RL agent accepting 100 entries (predictor values) and containing 50 trees

An example of filling input values with normalized close prices:

void calcSignal() { sig1=0; double arr[]; CopyClose(NULL,0,1,10000,arr); ArraySetAsSeries(arr,true); normalizeArrays(arr); for(int i=0;i<ArraySize(ag1.agent);i++) { ArrayCopy(ag1.agent[i].inpVector,arr,0,0,ArraySize(ag1.agent[i].inpVector)); } sig1=ag1.getTradeSignal(); }

Training takes place in the tester in one pass with the parameter learn=true. After training, we need to change it to false.

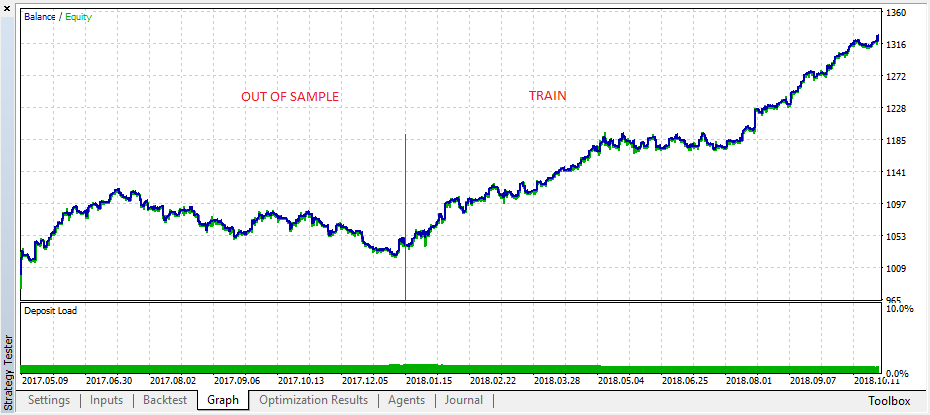

Demonstrating the trained "RL gmdh trader" EA operation on training and test samples.

Tradotto dal russo da MetaQuotes Ltd.

Codice originale https://www.mql5.com/ru/code/22915

Contrarian trade MA

Contrarian trade MA

Working by iMA (Moving Average, MA) and OHLC of W1 timeframe

Exp_XFisher_org_v1

Exp_XFisher_org_v1 Expert Advisor based on XFisher_org_v1 oscillator signals.