How to create a profitable strategy?

Here is some advice based on my own experiences, but there are many other traders offering similar advice.

- The most important aspect of any trading strategy in order for it to be profitable, is money management. Even if your win-rate is only 50/50 and RRR of 1:1 (which can easily be achieved), it is your money management rules that can make it it a profitable strategy (or not). I repeat this is the most important part — Money Management!.

- Your risk per trade should be based primality on your stop-loss size, and not only on your margin requirements. Your risk per trade should be as low as possible and you should always aim to have as low a drawdown as possible. Aim to NOT lose money, before you consider your profit.

- Exit rules are extremely important for a profitable strategy. Things like the stop-loss size, trailing-stops, partial close, scaling-out, etc.

- The most important indicator for all of this, is the Average True Range (ATR). Master its use.

- And always consider how the spread and commission costs affects the above. There is no advantage in making a small profit, if the spread and commission wipe it out.

That is it!

Did you notice I did not mention anything about your entry signals?

That is because that is secondary. As long as you can get at least a 50/50 win rate and a 1:1 Risk to Reward ratio, the above points can make it reasonably profitable.

Obviously, the better your win rate and RRR, the better your profits, but is the points above that really make it happen.

Your aim should be to approach a Profit Factor of 2.0 or higher, and a Recovery Factor of 2.0 or higher.

And also, diversify your trading. Don't depend on trading just one symbol or just one strategy, otherwise you could have long drawdown periods. Having multiple strategies and trading multiple symbols helps when one is in drawdown and the other not.

Also read the following ...

Take a few lessons from Prop Firms (Part 1) — An introduction

Fernando Carreiro, 2023.04.19 16:20

In this introductory article, I address a few of the lessons one can take from the challenge rules that proprietary trading firms implement. This is especially relevant for beginners and those who struggle to find their footing in this world of trading. The subsequent article will address the code implementation.

Here is some advice based on my own experiences, but there are many other traders offering similar advice.

- The most important aspect of any trading strategy in order for it to be profitable, is money management. Even if your win-rate is only 50/50 and RRR of 1:1 (which can easily be achieved), it is your money management rules that can make it it a profitable strategy (or not). I repeat this is the most important part — Money Management!.

- Your risk per trade should be based primality on your stop-loss size, and not only on your margin requirements. Your risk per trade should be as low as possible and you should always aim to have as low a drawdown as possible. Aim to NOT lose money, before you consider your profit.

- Exit rules are extremely important for a profitable strategy. Things like the stop-loss size, trailing-stops, partial close, scaling-out, etc.

- The most important indicator for all of this, is the Average True Range (ATR). Master its use.

- And always consider how the spread and commission costs affects the above. There is no advantage in making a small profit, if the spread and commission wipe it out.

That is it!

Did you notice I did not mention anything about your entry signals?

That is because that is secondary. As long as you can get at least a 50/50 win rate and a 1:1 Risk to Reward ratio, the above points can make it reasonably profitable.

Obviously, the better your win rate and RRR, the better your profits, but is the points above that really make it happen.

Your aim should be to approach a Profit Factor of 2.0 or higher, and a Recovery Factor of 2.0 or higher.

And also, diversify your trading. Don't depend on trading just one symbol or just one strategy, otherwise you could have long drawdown periods. Having multiple strategies and trading multiple symbols helps when one is in drawdown and the other not.

Also read the following ...

Recently, I've developed several trading strategies and found that creating a profitable one is quite challenging.

One of the strategies involves numerous conditions, but I've noticed that these conditions affect the trading volume.

However, relaxing these conditions results in losses instead.

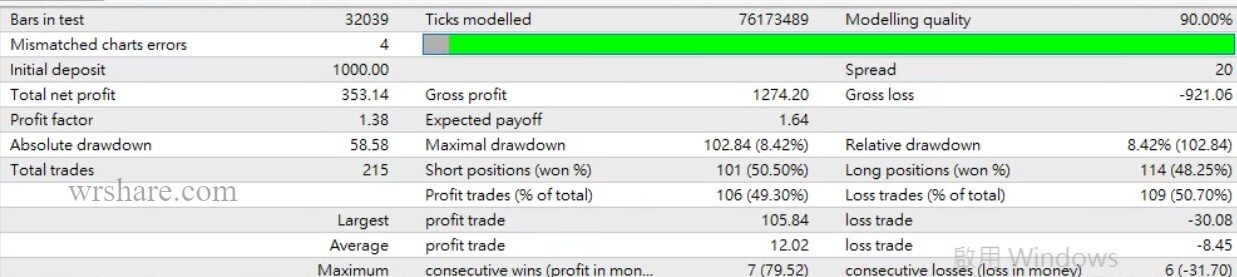

Below are the entry conditions and backtesting results.

I would greatly appreciate any advice from experts in this field. Thank you very much.

Entry conditions:losing price is above the upper Bollinger Band.

- The second upper Bollinger Band is greater than the first upper Bollinger Band.

- The closing price is above the 200-period weekly moving average (200MA).

- The 50-period daily moving average (50MA) is greater than the 200-period moving average (200MA).

- Matches the defined candlestick pattern.

Consider simple rules and optimization as a way to understand the market behavior and sync with It.

If the trading volume is too low because of filters or because You must trade an higher time frame, diversify trading more less correlated instruments.

When I set the risk-reward ratio, I've noticed that using a 500-point stop loss and a 1000-point take profit often leads to hitting the stop loss.

However, what I want to emphasize isn't just the size of the stop loss and take profit, but rather that this particular setup tends to result in losses during backtesting.

I suspect this outcome might stem from other issues rather than solely the size of the stop loss and take profit.

Have others encountered similar situations?

Are there any methods available to optimize this risk-reward setup and enhance the probability of successful trades?

There is a fallacy that one should use a high reward to risk ratio of 2:1 or 3:1, etc.

However, one should not forget that the probability of the take profit being hit reduces greatly as one makes the reward greater than the risk, which results in the win rate dropping as well. They are directly related.

One should not strive to have a large reward compared to the risk. Keeping them similar (i.e. close to 1:1) is much better as the probability of either being hit stays close to the 50/50 probability.

Instead, focus on how you should handle the Money Management and exit strategies.

Here is an example of exit rules:

- If favourable, close half the volume at 1:1 take-profit, move the stop to break-even, and then trail the rest of the volume and let it ride out the trend as far as it will go.

- If adverse, close out half the volume when price reaches 2/3 the way to the stop-loss.

This was just one simple example. There are many other exit strategies that can be considered.

Once you have this in place, you can then focus on the signal and filtering selection to improve the probability of the trades going favourably, thus increasing the win rate.

Is the result from running for five years indicating too little trading volume and insufficient profit?

{kind=link}

Since MetaTrader 4 Strategy Tester (without 3rd party tools) is unable to test with real tick data, such a report can sometimes be misleading if your strategy rules are not specifically adjusted to take that into account.

Also, only 215 trades in five years seems too small a sample size for an adequate appraisal.

Since MetaTrader 4 Strategy Tester (without 3rd party tools) is unable to test with real tick data, such a report can sometimes be misleading if your strategy rules are not specifically adjusted to take that into account.

Also, only 215 trades in five years seems too small a sample size for an adequate appraisal.

That depends on the strategy rules and the time-frame you use. There are no set rules, unfortunately.

I'm assuming your time-frame is daily or higher, which makes it difficult to get a decently large sample size.

My own experience is mostly trading hourly or lower, so it is much easier for me to get a very large sample size in tests.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Recently, I've developed several trading strategies and found that creating a profitable one is quite challenging.

One of the strategies involves numerous conditions, but I've noticed that these conditions affect the trading volume.

However, relaxing these conditions results in losses instead.

Below are the entry conditions and backtesting results.

I would greatly appreciate any advice from experts in this field. Thank you very much.

Entry conditions:losing price is above the upper Bollinger Band.