|

6+ anos

experiência

|

0

produtos

|

0

versão demo

|

|

0

trabalhos

|

0

sinais

|

0

assinantes

|

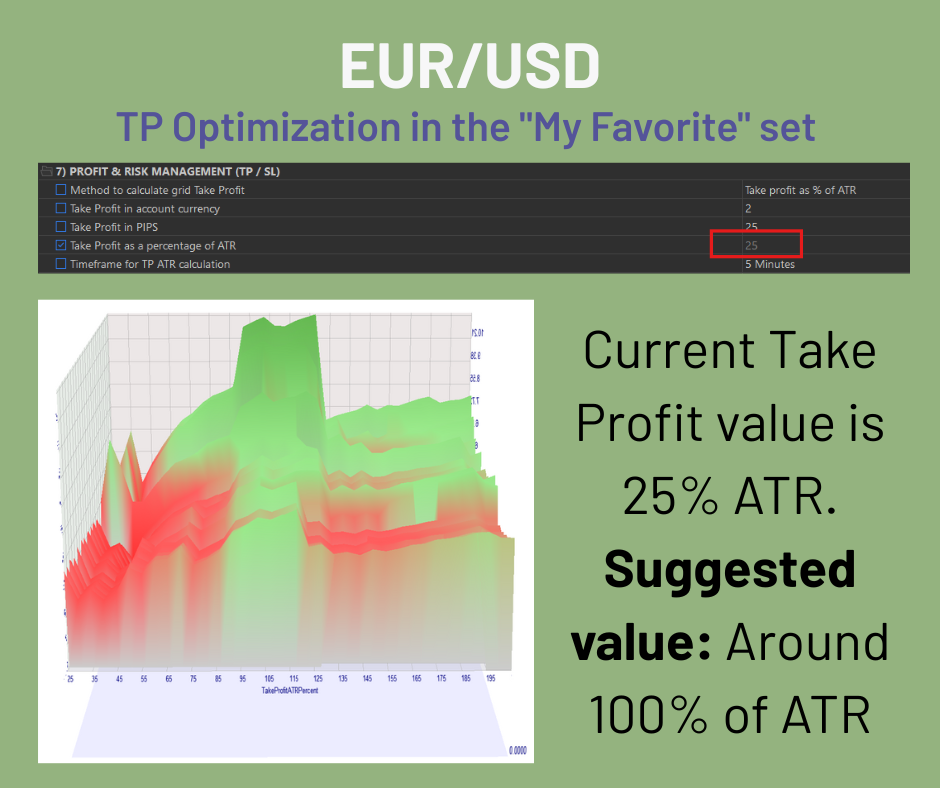

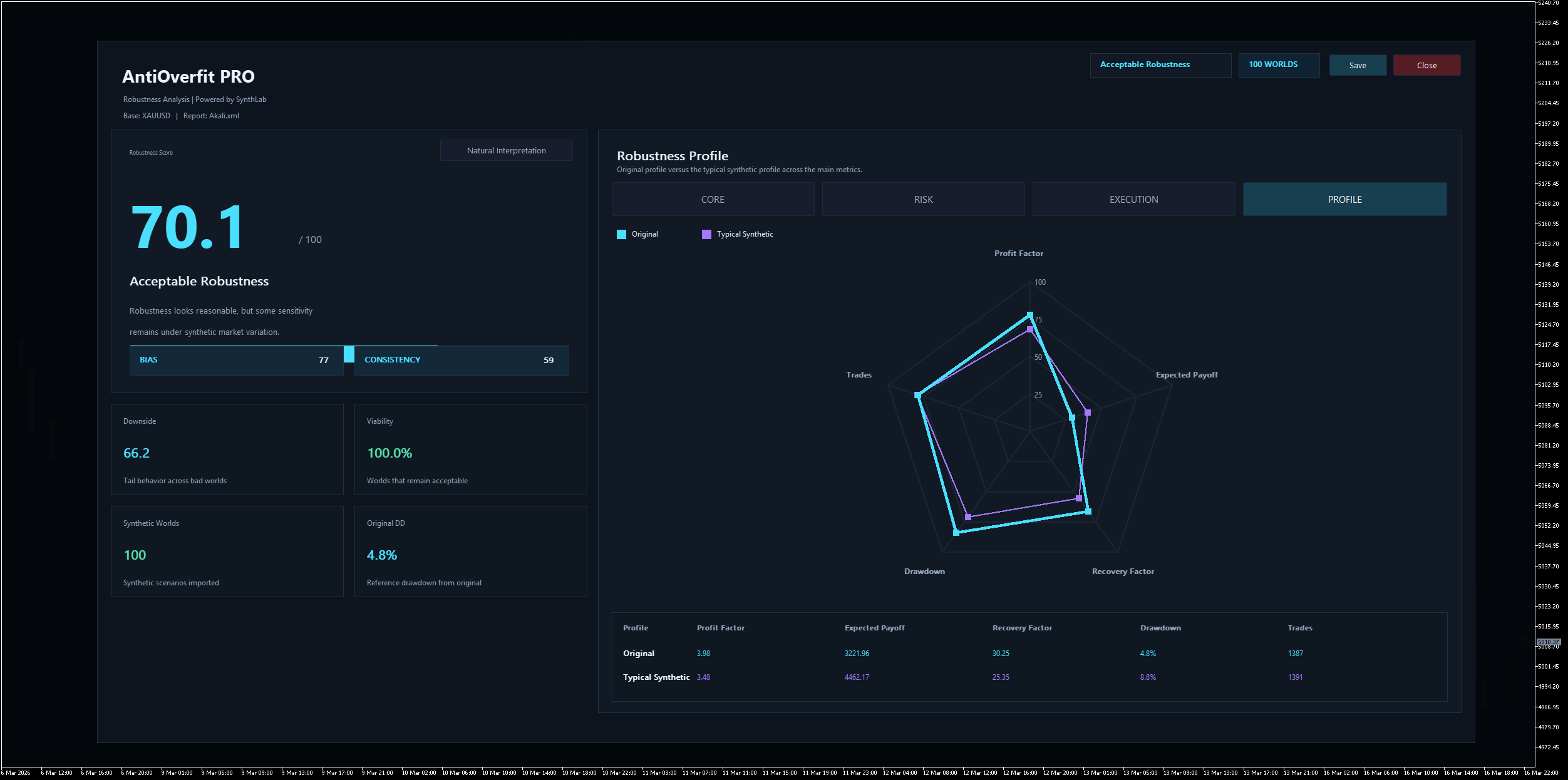

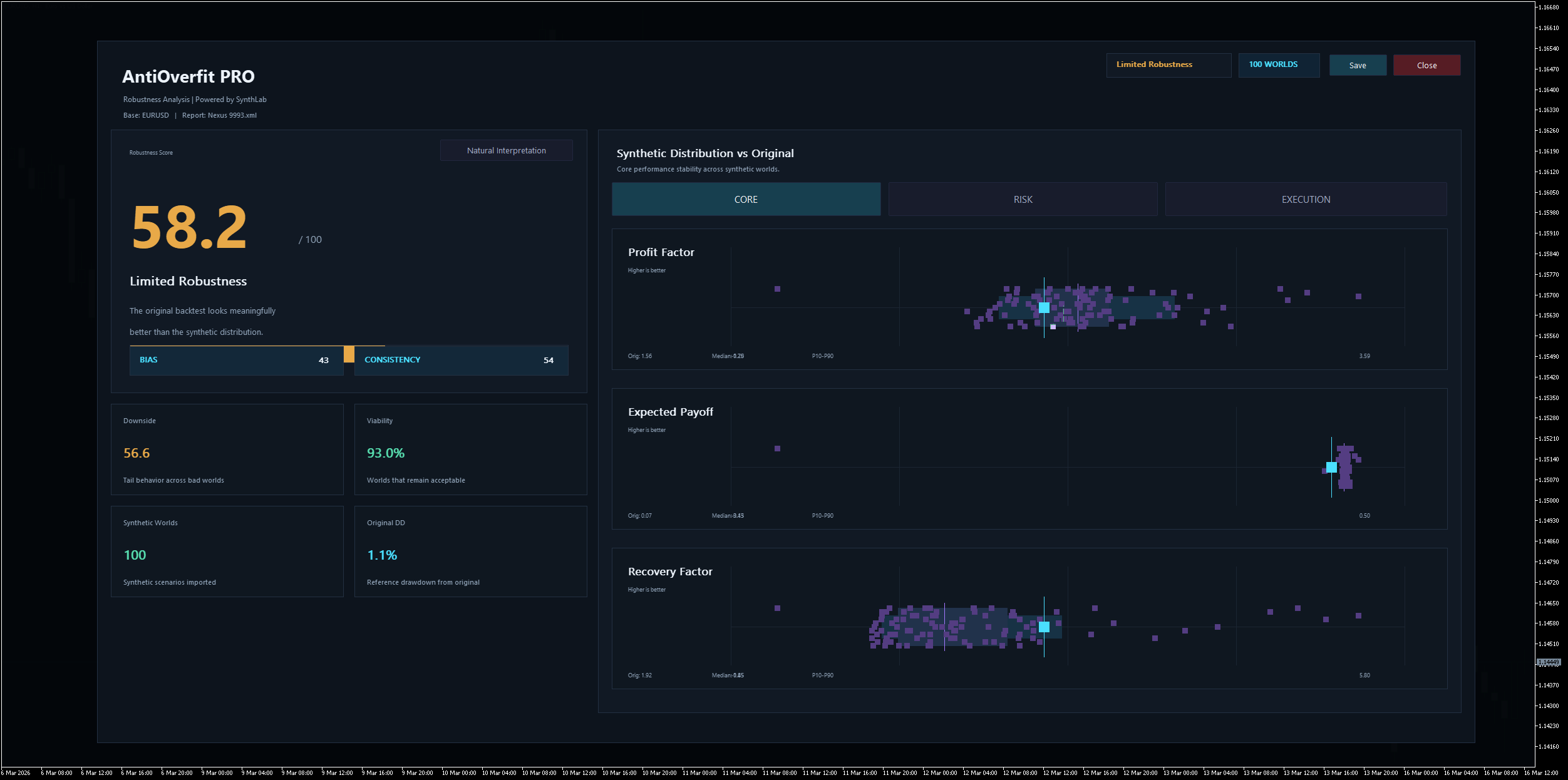

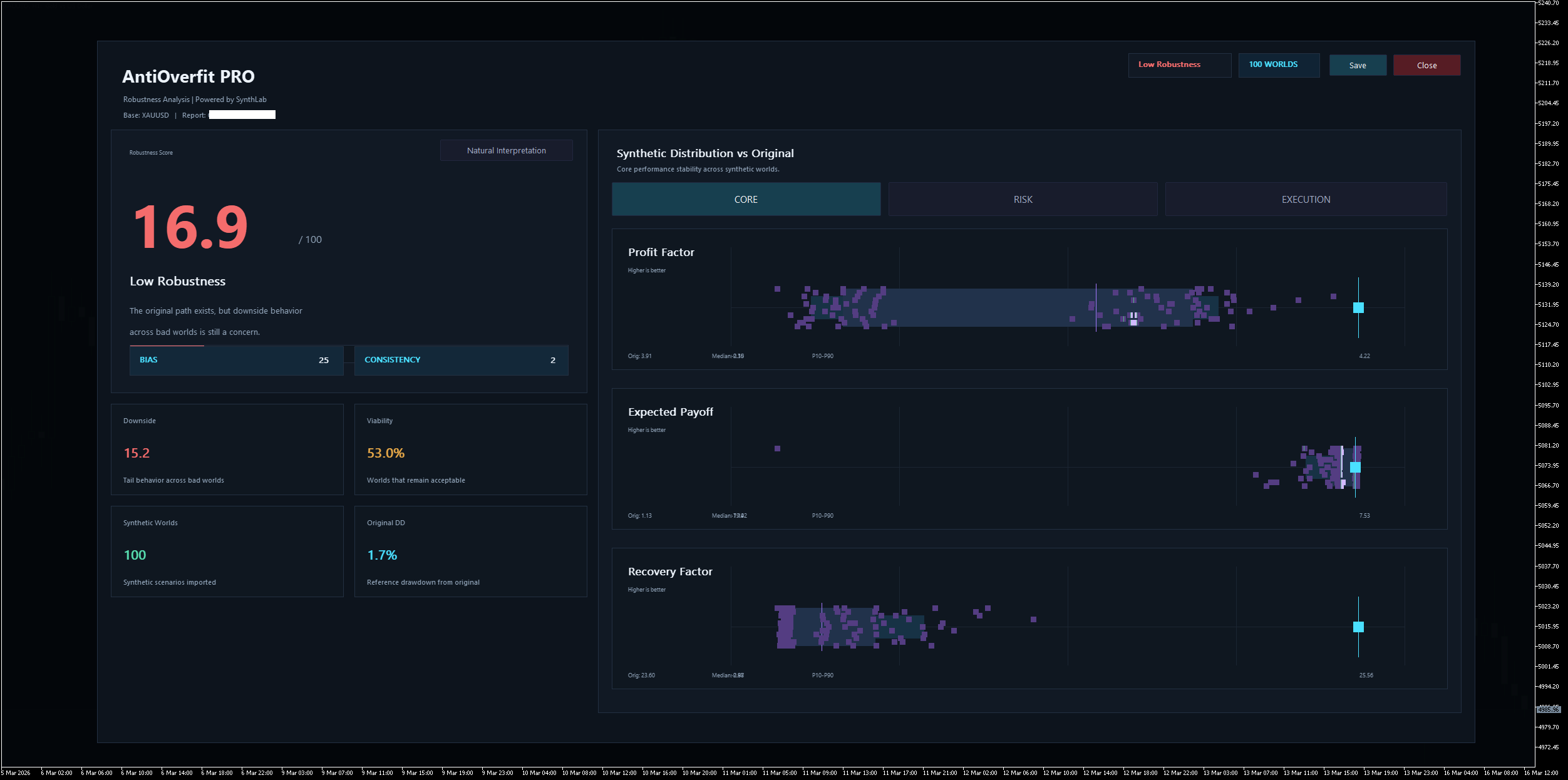

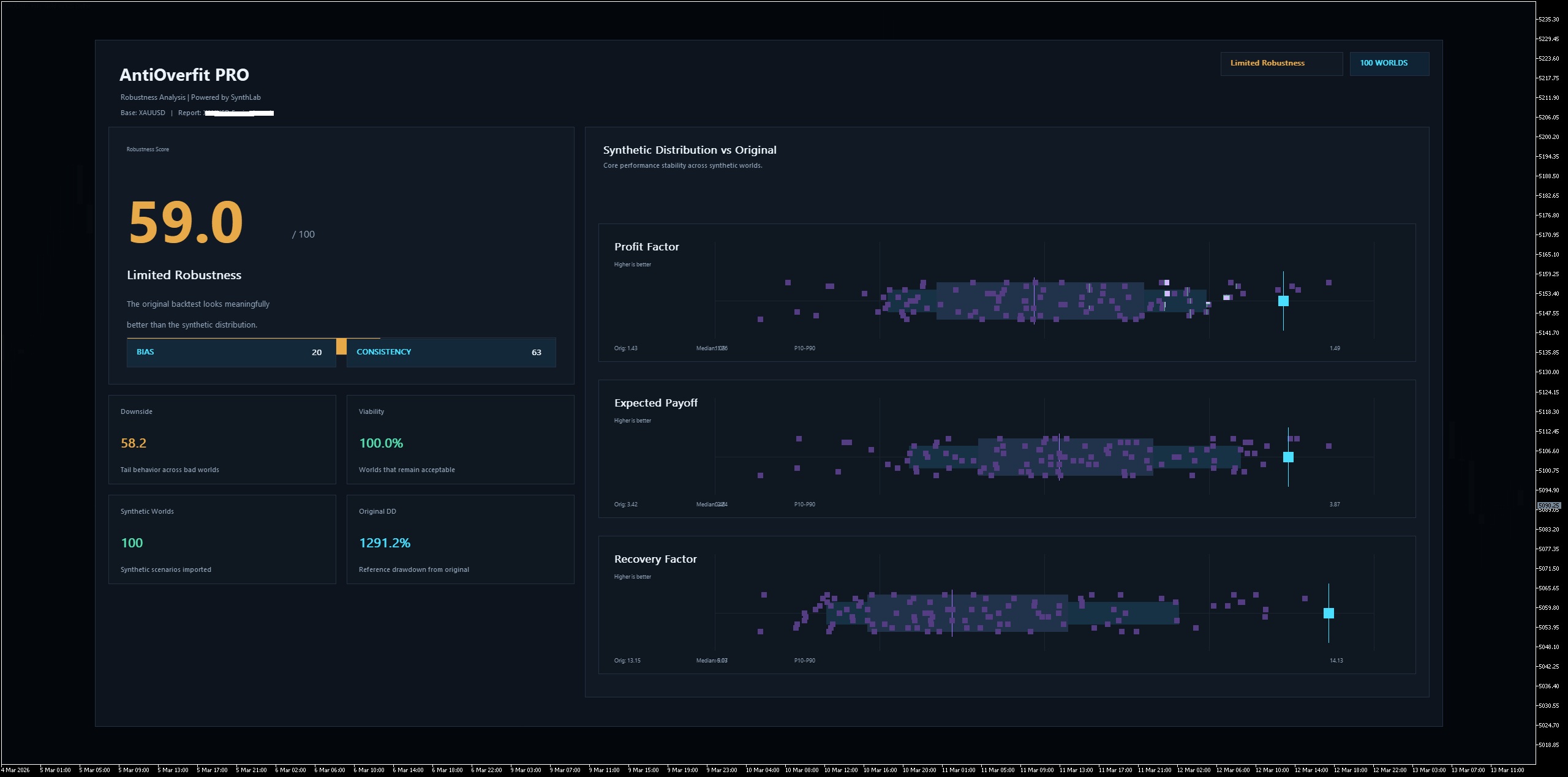

AntiOverfit PRO guide: https://www.mql5.com/en/blogs/post/768007

Enrique Enguix

· 1

Enrique Enguix

2026.03.16

There's a small error in this image; the DD is 12.91%. The image is from a beta version, and there was an error reading the file.