Discussion of article "How to Develop a Profitable Trading Strategy"

Great article Yuri. i really i learnt here some missed informations regards startegy.

Happy Piping..

Hello

Thanks for the article. It is very interesting.

I has one doubt about the number of points taken from indicator. In the test, you used 4 points with a interval of 7 bars from each other.

How we calculate the number of points and the interval from each other? This is calculated empirically or mathematically?

Thanks

I don't know why, but I cannot reproduce the same results. The MetaQuote's history data has been used for this backtest. Any idea what I'm doing wrong?

Hello

Has any form to train the neural network with other algorithm method? Like Standard backpropagation?

I read that the genetic algorithm used by the tester is not the best one.

Thanks

I don't know why, but I cannot reproduce the same results. The MetaQuote's history data has been used for this backtest. Any idea what I'm doing wrong?

I get the same poor results?

Any thoughts?

great great great article

Yury is pure master

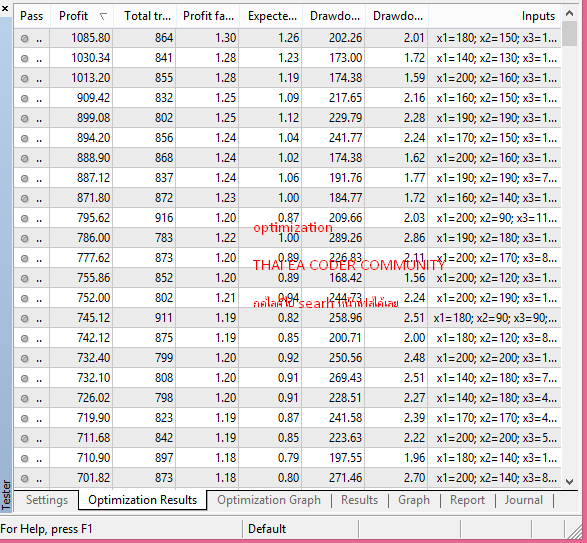

i'm running optmization base on the code.

well, it is profitable.

Great article! Thanks for sharing.

People like Yury are the backbones of this community. We newbies need to read more of these and pay our attention to learning the skills rather than trolling through the "Market" tab in MT.

Saludos a todos.

Señor Yury Reshetov me puede decir por favor ¿porqué en el indicador del Perceptron (AC) usted escribe "symbol()" en lugar de "NULL"?.

=======================================================================================================

Greetings everyone.

Sir Yury Reshetov please tell me ¿why in the Perceptron indicator (AC) you write "symbol()" instead "NULL"?

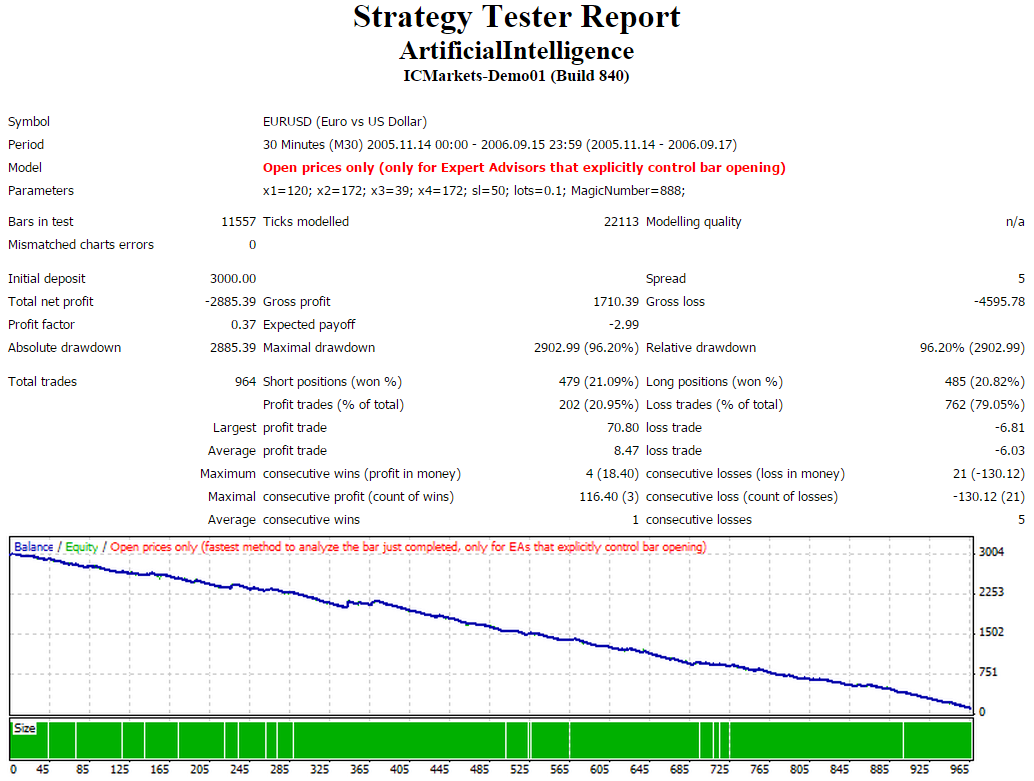

can anyone confirm the backtest? im getting different results when optimising it. Then when I tried the results that he "got" to the testing period, it is different also.

1. Optimise period is 2005.11.14 to 2006.09.17. M30, EURUSD, openprices, Maximal DD < 35%.

2. results from optimise is. "We will obtain the results for the input parameters: x1 = 146, x2 = 25, x3 = 154, x4 = 121, sl = 45."

3. Testing period is "3 months after optimization period". So 2006.09.18 to 2006.12.18. correct?

4. result is supposedly profitable, but not to me.

really interested in knowing this but the backtest is not consistent.

Thanks!

regards,

Francis

great great great article

Yury is pure master

i'm running optmization base on the code.

well, it is profitable.

hi can you share what did you do, parameters, etc? im getting different results. Would really appreciate it

Thank you!

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

New article How to Develop a Profitable Trading Strategy has been published:

This article provides an answer to the question: "Is it possible to formulate an automated trading strategy based on history data with neural networks?".

The process of developing successful trading strategies with implementation of technical analysis can be divided into several stages:

Let's see what happens, if we try to computerize the whole process.

This article analyzes the use of a simple single-layer neural network for identifying the future price movements based on the readings of the Acceleration/Deceleration (AC) Oscillator.

Author: Yury Reshetov