From theory to practice - page 79

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

I have, for example, compiled what I call technical passports of probability densities of currency pair increments.

These datasheets do not describe the pairs, but the filter settings. Try to check how they change, especially during the summer holidays.

Thank you.

But... I really don't know how to graph SB. Not only that, I don't trust any of the pseudo-random number generators at all until I check them myself. And that's an extremely hard thing to do, so I never compare with graphs.

It's a whole branch, I've been tortured to find it. Is there really a standard defining what "SB" is?

is to move a point by a distance +1 or -1 with probability p. Where (0<p<1).

In the case of a coin p is always strictly 1/2.

Forced to repeat the question, "This is a whole branch, tortured to find. Is there really a standard that defines what "SB" is?

I was interested in the availability of a standard. GOST, ROST, CEB, IEEE, finally. Is there a standard?

P.S. While I was repeating the question, the answer was that there are no standards, the link does not lead to them. This is the case. Was this answer correct? I don't know.

The standards that are supposed to account for variance instability, I've gathered, but haven't read it yet

GOST_R_54500_1-2011.pdf

GOST_R_54500_3-2011.pdf

GOST_R_54500_3_1-2011.pdf

GOST_R_54500_3_2-2013.pdf

I do not answer, but at first glance they do not contain the words "accidental wandering".

And the most complex?

And the most complicated one is modelling the market stack with the order matching algorithm and the market maker algorithm, only on incoming flows of buy and sell market orders you feed PRNG.

only immediately rushed to price deviations from the average, not increments. And the process of the price itself, in contrast to the increments, has become non-stationary! It is more difficult to analyse. Give it up. Analyze ONLY the increments. It will give you a great deal.

I have, for example, compiled what I call technical passports of probability densities of currency pair increments. It makes sense because the process of increments is stationary.

Where did you see that increments are tested for stationarity.

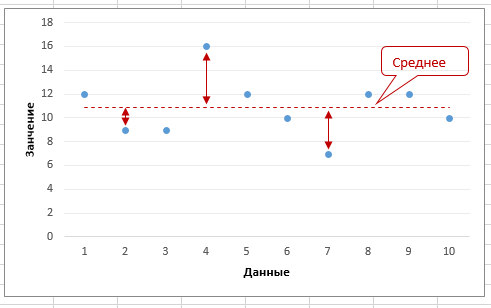

Stationarity is usually checked for a process.

deviations from the mean.

We're not going to flip a coin 20,000 times to generate a row ourselves.)

And the most complex you simulate a market stack with an order-matching algorithm, and a market maker algorithm, only on the incoming streams of buy and sell market orders you feed PRNG.

Forced to repeat the question, "It's a whole thread, tortured to find. Is there really a standard defining what "SB" is?

I was interested in the availability of a standard. GOST, ROST, CEB, IEEE, finally. Is there a standard?

P.S. While I was repeating the question, the answer was that there are no standards, the link does not lead to them. This is the case. Was this answer correct? I don't know.

The standards, which are supposed to take into account variance instability, have collected, but haven't read it yet

GOST_R_54500_1-2011.pdf

GOST_R_54500_3-2011.pdf

GOST_R_54500_3_1-2011.pdf

GOST_R_54500_3_2-2013.pdf

I do not answer, but at first glance they do not contain the words "accidental wandering".

https://dic.academic.ru/dic.nsf/enc_mathematics/5137/СЛУЧАЙНОЕ

Yes, you can! Just trade not increments, but ON increments. Many people use it, it's called "pipsing". But they are ruined by spread and commission. I understood it at once, so I gave up this method.

I already told you, what will it give you if you know that the next most probable gain is 1 pip.