당사 팬 페이지에 가입하십시오

- 게시자:

-

MetaQuotes

MetaQuotes Ltd is the software development company. One of our products is the MetaTrader 5 trading platform intended for trading in different financial markets.

MetaQuotes Ltd is the software development company. One of our products is the MetaTrader 5 trading platform intended for trading in different financial markets.

Use the links below to download the latest builds: - 조회수:

- 1235

- 평가:

- 게시됨:

- 업데이트됨:

-

이 코드를 기반으로 한 로봇이나 지표가 필요하신가요? 프리랜스로 주문하세요

프리랜스로 이동

이 코드를 기반으로 한 로봇이나 지표가 필요하신가요? 프리랜스로 주문하세요

프리랜스로 이동

실제 저자:

Sergey Bochkanov. ALGLIB 프로젝트 웹사이트 - http://www.alglib.net/. 라이브러리는 1999년부터 시작되었습니다.

ALGLIB는 가장 크고 완벽한 수학 라이브러리 중 하나입니다.

푸리에 변환이나 미분 방정식 시스템을 빠르게 만들고 싶은가요? 모든 메서드를 소스 코드로 한곳에 모으기 위해 복잡한 데이터 분석을 수행해야 하나요? 그렇다면 ALGRIB 수학 메서드 라이브러리를 사용해 보세요!

ALGLIB는 현재 다국어 알고리즘의 최고의 라이브러리 중 하나입니다. 다음은 공식 웹사이트에 언급된 ALGLIB에 대한 소개입니다:

ALGLIB는 크로스 플랫폼 수치 분석 및 데이터 처리 라이브러리입니다. 여러 프로그래밍 언어(C++, C#, Pascal, VBA)와 여러 운영 체제(Windows, Linux, Solaris)를 지원합니다. ALGLIB 기능은 다음과 같습니다:

- Linear algebra (direct algorithms, EVD/SVD)

- Solvers (linear and nonlinear)

- Interpolation

- Optimization

- Fast Fourier transforms

- Numerical integration

- Linear and nonlinear least-squares fitting

- Ordinary differential equations

- Special functions

- Statistics (descriptive statistics, hypothesis testing)

- Data analysis (classification/regression, including neural networks)

- Multiple precision versions of linear algebra, interpolation optimization and others algorithms (using MPFR for floating point computations)

왜 ALGLIB를 사용해야 할까요? 왜냐하면:

ALGLIB 라이브러리는 지속적으로 향상되고 있으며 사용자의 의견에 따라 새로운 기능과 개선 사항이 정기적으로 구현됩니다. 최신 버전은 4.0입니다.

또한 라이브러리에는 제안된 메서드의 기능 주요 부분을 다루는 테스트 케이스의 모음이 포함되어 있습니다. 그렇게 하면 테스트를 수행할 수 있고 프로젝트의 저자에게 감지된 오류를 보고 할 수 있습니다.

CAlglib 클래스의 정적 함수는 라이브러리와 함께 사용해야 합니다. 모든 라이브러리 함수는 정적 함수로 CAlglib 시스템 클래스로 이동됩니다.

testclasses.mq5 and testinterfaces.mq5 테스트 케이스 스크립트는 간단한 usealglib.mq4 데모 스크립트와 함께 첨부됩니다. 동일한 이름의 Include 파일(testclasses.mqh 및 testinterfaces.mqh)은 테스트 케이스를 시작하는 데 사용됩니다. 이들은 \MQL5\Scripts\Alglib\Testcases\에 놓아야 합니다.

참고: testclasses.mq5 스크립트를 실행하는데는 꽤 오랜 시간(약 8분)이 걸립니다.

다음은 포트된 ALGLIB MQL5 라이브러리 패키지에 대한 자세한 정보입니다.

| 패키지 | 설명 |

|---|---|

| alglib.mqh | 기본 라이브러리 패키지에는 사용자 정의 기능이 포함되어 있습니다.라이브러리를 사용하기 위해서는 이러한 함수가 호출되어야 합니다. |

| alglibinternal.mqh | 다른 라이브러리 패키지 작업을 위한 추가 클래스. |

| alglibmisc.mqh | 패키지에는 다음 클래스가 포함되어 있습니다.

|

| ap.mqh | 패키지에는 다른 패키지에 필요한 추가적인 클래스도 포함되어 있습니다. |

| bitconvert.mqh | MQL5에서 기본으로 제공되지 않는 С++ 기본 클래스 및 기능:

|

| dataanalysis.mqh | 데이터 분석 클래스:

|

| delegatefunctions.mqh | 패키지에는 대리자를 대체하기 위해 생성된 클래스가 포함되어 있습니다. 이들 클래스의 객체는 여러 라이브러리의 메서드에서 최적화된 함수입니다. |

| diffequations.mqh | 상미분 방정식을 풀기 위한 클래스:

|

| fasttransforms.mqh | Fast Transformation 클래스:

|

| integration.mqh | 적분용 클래스:

|

| interpolation.mqh | 보간, 근사 및 수치 미분 클래스:

|

| linalg.mqh | 선형 대수 연산 계산을 위한 클래스:

|

| matrix.mqh | 행렬 클래스: 정수, 연속 및 복소수. |

| optimization.mqh | 차원 및 다차원 최적화 클래스:

|

| solvers.mqh | 선형 및 비선형 방정식 시스템을 풀기 위한 클래스:

|

| specialfunctions.mqh | 분포 함수, 적분 및 다항식의 클래스:

|

| statistics.mqh | 통계 데이터 분석 클래스:

|

Code:

라이브러리 함수에는 사용방법에 대해 자세한 설명이 있습니다.

//+------------------------------------------------------------------+ //| Calculation of the distribution moments: mean, variance, | //| skewness, kurtosis. | //| INPUT PARAMETERS: | //| X - sample | //| N - N>=0, sample size: | //| * if given, only leading N elements of X are | //| processed | //| * if not given, automatically determined from | //| size of X | //| OUTPUT PARAMETERS | //| Mean - mean. | //| Variance- variance. | //| Skewness- skewness (if variance<>0; zero otherwise). | //| Kurtosis- kurtosis (if variance<>0; zero otherwise). | //+------------------------------------------------------------------+ static bool CBaseStat::SampleMoments(const double &cx[],const int n,double &mean, double &variance,double &skewness,double &kurtosis) { //--- check if(!CAp::Assert(n>=0,__FUNCTION__+": the error variable")) return(false); //--- check if(!CAp::Assert(CAp::Len(cx)>=n,__FUNCTION__+": length(x)<n")) return(false); //--- check if(!CAp::Assert(CApServ::IsFiniteVector(cx,n),__FUNCTION__+": x is not finite vector")) return(false); //--- create variables double v=0; double v1=0; double v2=0; double stddev=0; //--- Init, special case 'N=0' mean=0; variance=0; skewness=0; kurtosis=0; //--- check if(n<=0) return(true); //--- Mean for(int i=0;i<n;i++) mean+=cx[i]; mean/=n; //--- Variance (using corrected two-pass algorithm) if(n!=1) { //--- calculation for(int i=0;i<n;i++) v1+=CMath::Sqr(cx[i]-mean); for(int i=0;i<n;i++) v2+=cx[i]-mean; v2=CMath::Sqr(v2)/n; variance=(v1-v2)/(n-1); //--- calculation stddev=MathSqrt(variance); } else variance=EMPTY_VALUE; //--- Skewness and kurtosis if(stddev!=0) { //--- calculation for(int i=0;i<n;i++) { v=(cx[i]-mean)/stddev; v2=CMath::Sqr(v); skewness+=v2*v; kurtosis+=CMath::Sqr(v2); } //--- change values skewness=skewness/n; kurtosis=kurtosis/n-3; } //--- successful execution return(true); }

라이브러리를 사용하기 위해서는 CAlglib 클래스 정적 함수를 사용해야 합니다. 다음은 통계 트레이딩 매개변수 계산을 위한 usealglib.mq5 함수 스크립트의 소스 코드입니다.

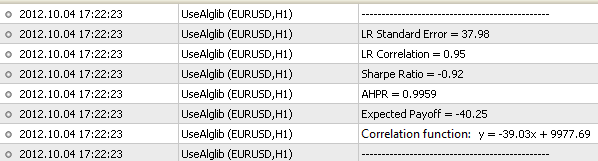

//+------------------------------------------------------------------+ //| UseAlglib.mq5 | //| Copyright 2012, MetaQuotes Software Corp. | //| https://www.mql5.com | //+------------------------------------------------------------------+ #property copyright "Copyright 2012, MetaQuotes Software Corp." #property link "https://www.mql5.com" #property version "1.00" //+------------------------------------------------------------------+ //| Connecting the libraries | //+------------------------------------------------------------------+ #include <Math\Alglib\alglib.mqh> #include <Trade\DealInfo.mqh> #include <Arrays\ArrayDouble.mqh> //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { //--- object to access data on deals CDealInfo deal; //--- object for storing profit/loss of each deal CArrayDouble *profit=new CArrayDouble; //--- objects for storing the balance CArrayDouble *balance_total=new CArrayDouble; //--- initial balance double balance=0; //--- receive history HistorySelect(0,TimeCurrent()); //--- total amount of deals int deals_total=HistoryDealsTotal(); //--- receive data on deals' profit and balance for(int i=0;i<deals_total;i++) { //--- move to the deal having i index deal.SelectByIndex(i); //--- receive initial balance if(deal.DealType()==DEAL_TYPE_BALANCE) { if(NormalizeDouble(deal.Profit()+deal.Swap(),2)>=0.0) if(balance==0.0) balance=deal.Profit(); } //--- receive profit and balance if(deal.DealType()==DEAL_TYPE_BUY || deal.DealType()==DEAL_TYPE_SELL) if(deal.Entry()==DEAL_ENTRY_OUT || deal.Entry()==DEAL_ENTRY_INOUT) { profit.Add(NormalizeDouble(deal.Profit()+deal.Swap()+deal.Commission(),2)); balance_total.Add(balance); balance=balance+NormalizeDouble(deal.Profit()+deal.Swap()+deal.Commission(),2); } } balance_total.Add(balance_total.At(balance_total.Total()-1)+profit.At(balance_total.Total()-1)); //--- copy data on the balance to double type array double arr_balance[]; ArrayResize(arr_balance,balance_total.Total()); for(int i=0;i<balance_total.Total();i++) arr_balance[i]=balance_total.At(i); //--- copy data on profit to double type array double arr_profit[]; ArrayResize(arr_profit,profit.Total()); for(int i=0;i<profit.Total();i++) arr_profit[i]=profit.At(i); //--- linear regression //--- number of independent variables int nvars=1; //--- sample volume int npoints=balance_total.Total(); //--- create the matrix of parameters for the linear regression CMatrixDouble xy(npoints,nvars+1); for(int i=0;i<npoints;i++) { xy[i].Set(0,i); xy[i].Set(1,arr_balance[i]); } //--- variable for detecting calculations result (successful, unsuccessful) int info; //--- class objects necessary for storing data on calculations CLinearModelShell lm; CLRReportShell ar; //--- arrays for storing regression results double lr_coeff[]; double lr_values[]; ArrayResize(lr_values,npoints); //--- calculate linear regression ratios CAlglib::LRBuild(xy,npoints,nvars,info,lm,ar); //--- receive linear regression ratios CAlglib::LRUnpack(lm,lr_coeff,nvars); //--- receive recovered linear regression values for(int i=0;i<npoints;i++) lr_values[i]=lr_coeff[0]*i+lr_coeff[1]; //--- calculate Expected Payoff double exp_payoff,tmp1,tmp2,tmp3; CAlglib::SampleMoments(arr_profit,exp_payoff,tmp1,tmp2,tmp3); //--- calculate HPR array double HPR[]; ArrayResize(HPR,balance_total.Total()-1); for(int i=0;i<balance_total.Total()-1;i++) HPR[i]=balance_total.At(i+1)/balance_total.At(i); //--- calculate standard deviation and math expectation from HPR double AHPR,SD; CAlglib::SampleMoments(HPR,AHPR,SD,tmp2,tmp3); SD=MathSqrt(SD); //--- calculate LR Correlation double lr_corr=CAlglib::PearsonCorr2(arr_balance,lr_values); //--- receive LR Standard Error double lr_stand_err=0; for(int i=0;i<npoints;i++) { double delta=MathAbs(arr_balance[i]-lr_values[i]); lr_stand_err=lr_stand_err+delta*delta; } lr_stand_err=MathSqrt(lr_stand_err/(npoints-2)); //--- calculate Sharpe Ratio double sharpe_ratio=(AHPR-1)/SD; //--- print PrintFormat("-----------------------------------------------"); PrintFormat("Correlation function: y = %.2fx + %.2f",lr_coeff[0],lr_coeff[1]); //--- parameters PrintFormat("Expected Payoff = %.2f",exp_payoff); PrintFormat("AHPR = %.4f",AHPR); PrintFormat("Sharpe Ratio = %.2f",sharpe_ratio); PrintFormat("LR Correlation = %.2f",lr_corr); PrintFormat("LR Standard Error = %.2f",lr_stand_err); PrintFormat("-----------------------------------------------"); //--- delete objects delete profit; delete balance_total; } //+------------------------------------------------------------------+

다음과 같은 결과를 얻게 됩니다:

MetaQuotes Ltd에서 러시아어로 번역함.

원본 코드: https://www.mql5.com/ru/code/1146

IndicatorParameters() 사용 예

IndicatorParameters() 사용 예

이 Expert Advisor는 IndicatorParameters() 함수를 사용하여 입력 매개변수의 수, 유형 및 값에 대한 정보를 얻는 방법을 보여줍니다.

실시간 최적화 결과의 시각화

최적화의 결과를 실시간으로 시각화하는 예를 소개합니다(균형 곡선 역학 및 Expert Advisor 통계 매개변수).

SMA(no loop)

SMA(no loop)

Fast way to calculate Simple moving average.

Trailing Star

Set Trailing Stop only when profit