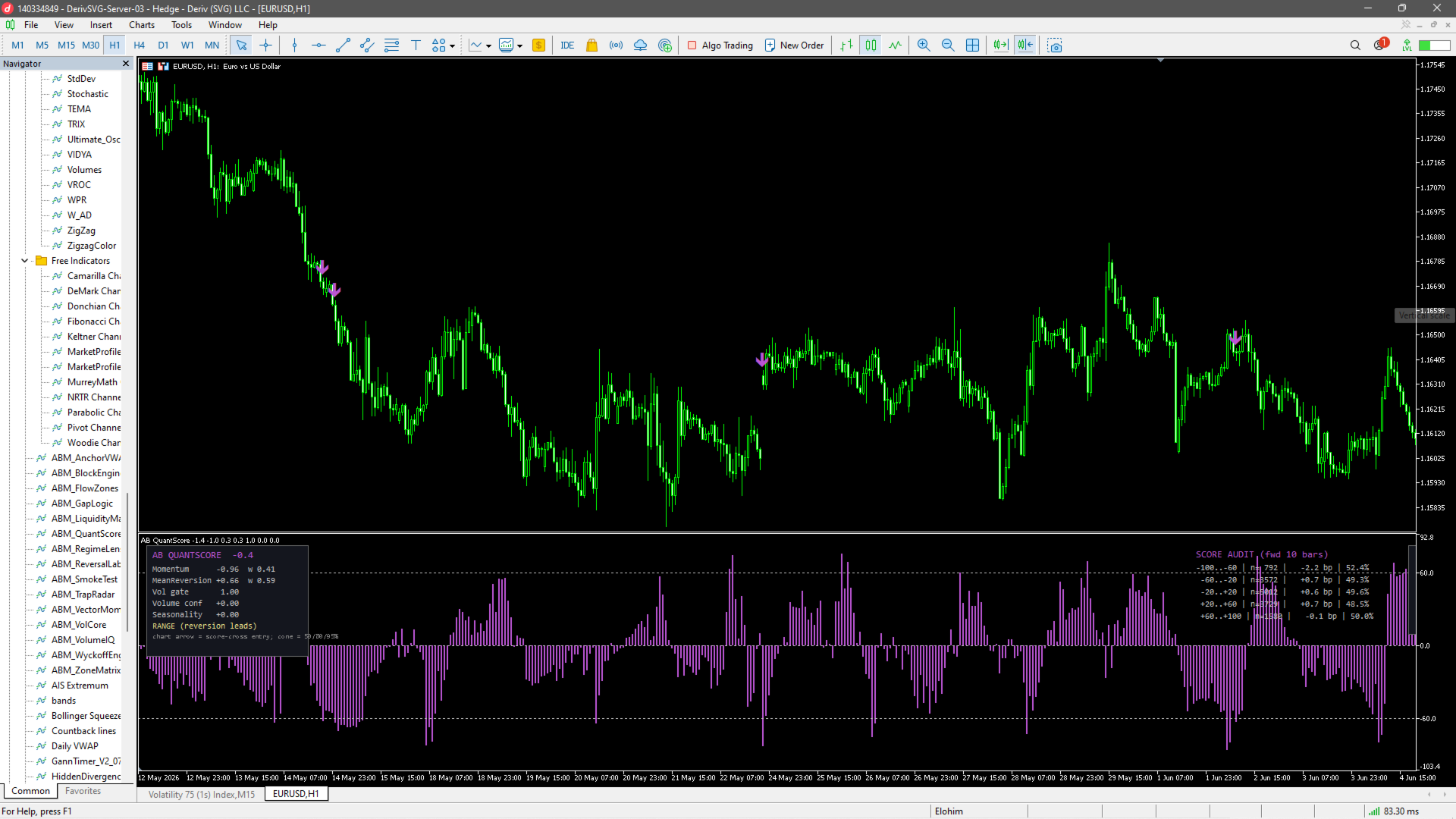

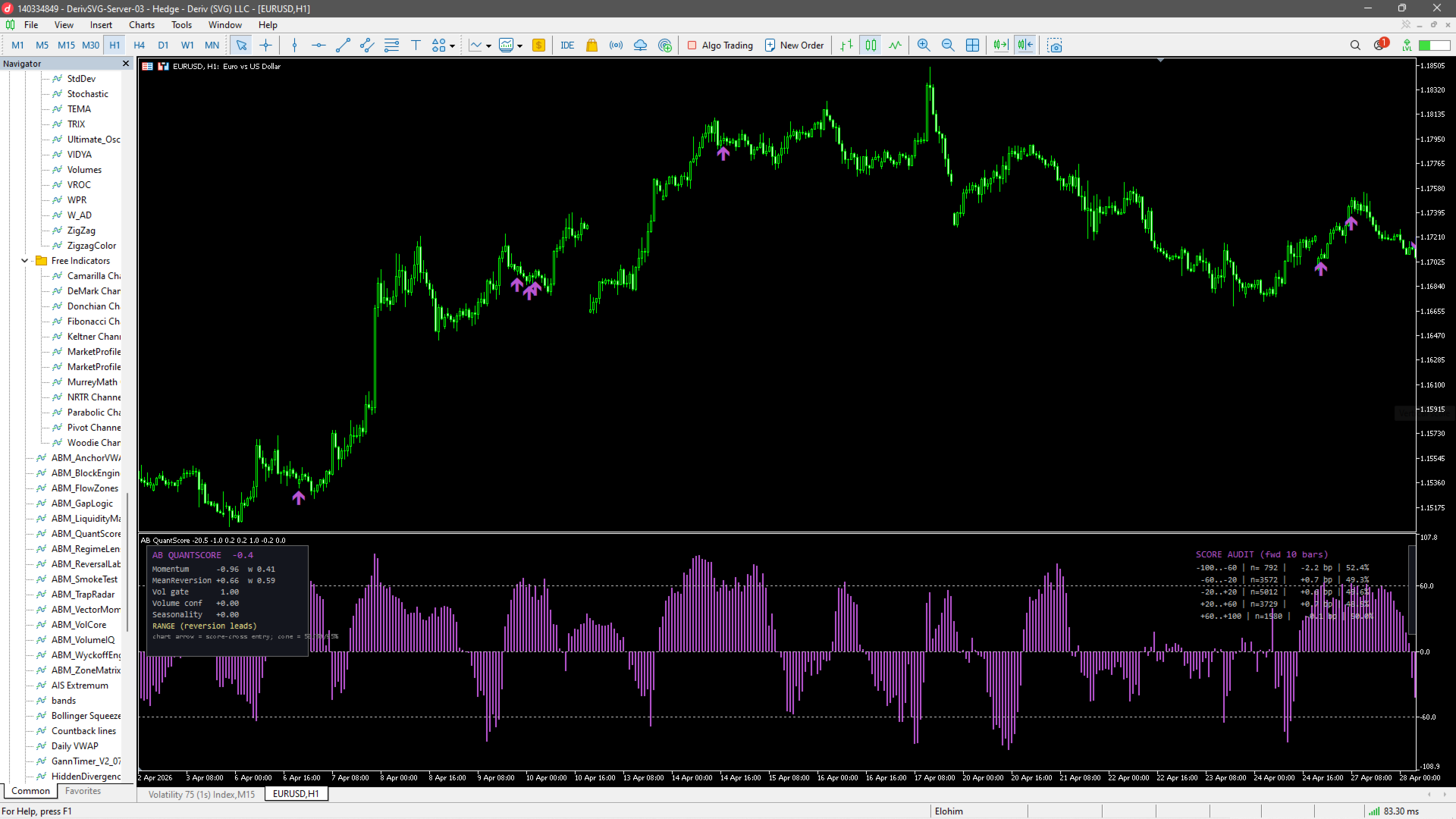

AB QuantScore

- Indicatori

- Versione: 1.0

- Attivazioni: 5

How it works

QuantScore is the suite's flagship: a multi-factor model compressing six independent measurements into one −100…+100 edge score.

– Momentum factor — the regression t-stat from the VectorMomentum core.

– Mean-reversion factor — z-score of price versus its volume-weighted mean, contributing against stretch when the regime is mean-reverting.

– Regime factor — the RegimeLens state sets the weighting between momentum and reversion. This dynamic weighting is the secret sauce; static-weight composites fail because the right factor depends on regime.

– Volatility factor — a Vol-Rank gate that dampens the score in extreme volatility, where edge decays.

– Volume factor — delta-pressure agreement with the score's direction.

– Seasonality factor — hour-of-day and day-of-week bias learned from the symbol's loaded history.

Extras: a probability cone projecting the expected price distribution N bars ahead, and a transparent score-audit table showing how the symbol actually behaved at each score band on your loaded history.

Marketplace description

| This is not another arrow indicator. QuantScore is a genuine multi-factor model: statistical momentum, mean-reversion stretch, market regime, volatility state, volume confirmation and time-of-day seasonality — six independent factors fused into one −100 to +100 edge score, with factor weights that adapt to the detected regime (momentum leads in trends, reversion leads in balance, the way real quant systems are built). The probability cone projects the expected price distribution ahead of you, and the built-in score-audit table shows you, from your own chart's history, how price actually behaved at every score level. A full factor-breakdown panel means you always know why the score is what it is. Non-repainting, all factors in EA-ready buffers. |