From theory to practice - page 134

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

If someone successfully uses this idea (returning to the mean from distribution tails that need to be seen in time) - great.

I'm just theorising this fact here. At the same time many interesting points from physics-mathematics have come up. I got carried away by the theory, what can I say... I'm a theorist by education - please, make allowances for this fact.

Now I've just disabled TS from trading - computer with it is 100% loaded and I have new ideas... - need to test them out. Well, a hobby of sorts has emerged.

But, this thread is no bullshit, as some people say. You can not read my posts, God forbid, but you read other people here, you should be able to read and you will find answers to many questions.

You have few deals and this is not enough to draw conclusions.

Here is the bare minimum you need:

//---

But actually this is not enough. You need to test on all available history and on all symbols and timeframes.

Such systems are very much dependent on the spread and stop levels. Therefore, the tests should be conducted in different conditions at different brokers.

Only in this way there is a chance to build a stable system. But this requires a lot of resources and power. Otherwise, tests and the search for the optimal parameters will take forever.

I use a different approach. I never try to make a grail for all characters at all times. Finding, optimizing and testing such a grail can really take forever. As soon as I obtain reasonable results in the tester, I place the Expert Advisor for real trading. I use it as long as it shows profit. Otherwise I change parameters or modify them. The main thing is that loss limitation must be implemented. I usually limit the loss at a level a little larger than the maximum drawdown at testing.

That's not a good approach. It just means that you are playing blind and you will always have a loss or a perpetual spin around zero. You probably didn't put yourself in this position on purpose. You simply do not have enough resources for that.

If you test this type of algorithm on the whole available history, you will know all its weaknesses, and that is the only way to improve the results.

That's not a good approach. It just means that you are playing blind and you will always have a loss or a perpetual spin around zero. You probably didn't put yourself in this position on purpose. You simply do not have enough resources for that.

If you test this type of algorithm on all available history, you will know all of its weaknesses, and that is the only way to improve your results.

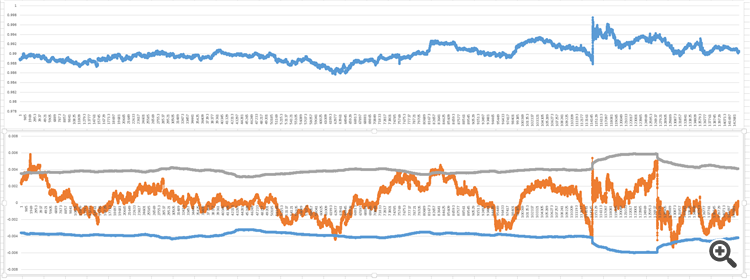

And here, for example, is this week's AUDCAD data:

Cool, isn't it?

Note the bounce yesterday, following the release of the Canadian interest rate decision.

And here, for example, is this week's AUDCAD data:

Pretty cool, isn't it?

Note the bounce yesterday, following the release of the Canadian interest rate decision.

Actually very cool, seriously!

There is, as always, only one question: "How do we make money on this?"

It's actually very cool, seriously!

There is, as always, only one question: "How can we make money from this?

It's actually very cool, seriously!

There is, as always, only one question: "How do you make money on this?"

You're telling the truth, Denis! Have you got the program set up, I hope? Or is there anything else you don't understand?

Not yet. Sick. Slowly getting back to work rhythm... Any questions, I'll ask them.