Best Arbitrage

MB Trading

MB Trading

Arbitrage trading, as described above, would work best if it could be executed in a single account.

This way you could avoid the problem that one trade side may produce big losses which have to be covered by enough margin capital till you can close both trades and pay back the losses of one side with the profit of the other.

Trading both sides in a single account the broker could charge the losses against the profit and no surplus money would be necessary to avoid a margin call.

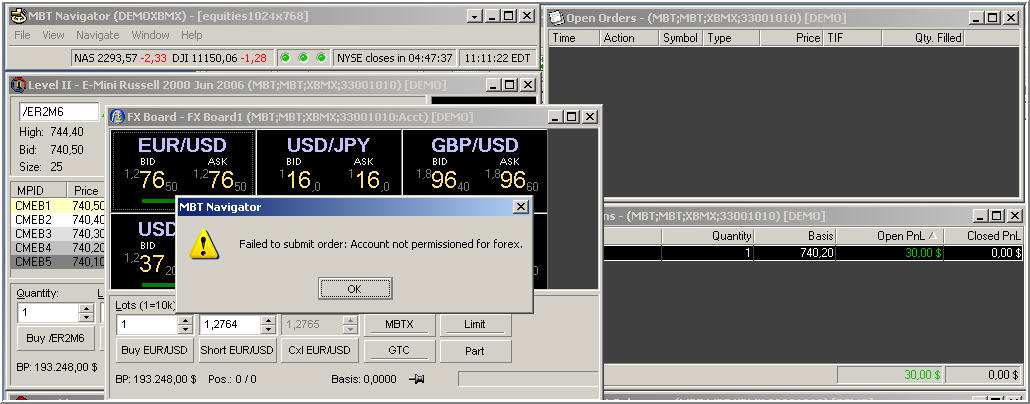

Technically the broker MB Trading (recommended by scott TTM) would be in a position to offer this service since his Tradestation offers both Future Trading and Spot Trading.

But testing the demo version of his tradestation named 'MBT Navigator' it seems that you cant trade both sides in the same account.

The Futures-Version of this trade station produces the errormessage ''Account not permissioned for forex'. See below.

Nevertheless doing both sides with the same broker even if you need different accounts should have the advantage that it doesn't take weeks but 1-2 days only to get the accounts balanced if necessary.

Perhaps you, scott, or somebody else has got practical experience whats possible with MB Trading or other brokers

Regards Martin

----

{kind=link}

any suggestions

You will need two accounts, thats the answer I got from MB Trading.

So catching the safe 12 pip profitdescribed above, where you could buy GBP for 1.9040 at the Spot market and sell it at the same time for 1.9052 in a Futures trade wont be easy.Any suggestion of yourshow to exploit this situation without runnig the risk that the loosing side triggers a margin call?

regards Martin

How arbitrage could work

Thanks pip-gandalf for your PM that you can program an automatic system no matter if a broker offers quote links and automatic trading or not and thanks for your offer to program my arbitrage idea.

So here are the details of the arbitrage system you asked for:

------------------------------------------------------------

A. Input Parameter

Instrument <- Default="GBPUSD"

WaitingTime <- Default=10 minutes

WaitMode <- Default=0

(0= Wait for Futures coming inside)

(1= Wait for narrow Forex Spread )

MoveRisk <- Default=500 pips

(Could be set to 0, if we find a broker where you can trade Futures and Forex within the same account)

B. Data Collection

Get CME Futures equivalents either from

http://equivalentsrdc.cme.com:443/index.html?

or calculate it yourself by subtracting the appropriate

(today -9.95 for bid and -10.05 for ask) forward points

from the realtime bid/ask of your MB Trading Futures account.

Calculate trade size that there is enough margin that one account can stand the above MoveRisk whereas the other account creates the same amount as profit.

C. First Trade

Compare Forex quote with Futures quote equivalent

1a. Buy Forex and Sell Futures

if Forex Ask + 10 pips < Futures Bid equivalent

2a. Buy Futures and Sell Forex

if Futures Ask equivalent + 10 pips < Forex Bid

same amount in both accounts (trade size see above)

D. Following Trade

(if situation inverses)

1b. if long in Forex

Sell Forex and Buy Futures

if ForexBid > 10 pips + Futures Ask equivalent

2n. if short in Forex

Buy Forex and Sell Futures

if Forex Ask + 10 pips < Futures Bid equivalent

same amount in both accounts (trade size see above)

After Waiting time start searching for closing opportunity:

E1. Closing Trade in WaitMode=0

1c. if long in your Forex account

Close both trades

if Forex Bid < Futures Bid equivalent

2c if short in your Forex account

Close both trades

if Forex Ask > Futures Ask equivalent

E2. Closing Trade in WaitMode=1

Close both trades

if Forex Spread < 3 pips

------------------------------------------------------------

I am very curious about your result, pip-gandalf,

kind regards Martin

hi Martin,

Well, I don't clear futures through MB - only Spot. So that's a correction to your first post here.

With MB, you would need to open a seperate account for FX than on Futures - theirs is not like Interactive Brokers that you can do all asset classes under one central account. I've never used IB, so i can't comment on them specifically.

With arb-trading between futures and spot - you need to recognize that the futures prices also reflect a premium over the spot - so if the quotes on Spot and futures are numerically the same, then they are way off in terms of real-life valuation. What this means is, they shouldn't ever trade at the same quote. The futures will always be higher because they have a premium, which I'm not sure how is calculated. But they will move tick for tick in line with each other.

This type of arb trading is best suited to an algorithm, as it can not only execute much faster than we can therefore reducing risk, but it can also identify opportunities like this on a daily basis that we can't see because they happen so quickly.

You're on the right path by programming it with pip-gandalf, so my suggestion would be to continue on that road. FYI, I don't do any arb trading so take my advice for what it's worth.

Hope this helps.

CME Equivalents

Thanks Scott for your answer,

You are right the futures quote differs from the Spot quote.

When a Spot Forex Broker offers a GBPUSD Ask = 1.9000 for example on CME the Globex price of the September 2006 GBP 5BU6 contract would be Ask = 1.9010.

The difference is the premium you mentioned.

But in the short time of an arbitrage trade this premium doesn't change so that you get it back when closing the trade.

To make comparison between Forex quotes and CME Futures quotes easier, CME offers its CurrencyEquivalent service. See attached screenshot.

Its available with the following link:

http://www.cme.com/trading/dta/real/eqivalents4042.html

and its free - you only have to register with email.

Using these equivalents you can immediately see if futures price has left your brokers spread creating an arbitrage opportunity, as under normal market condition futures equivalent price is nearly always within your brokers spread.

Last Thursday Oandas Ask was 12 pips below Futures Bid equivalent for a time span of 6 seconds see

https://www.forex-tsd.com/forum/commercial-talks/3241-best-news-broker#comment_78548

and the link to my quote video there.

So in principle such arbitrage trades are possible even if there remain some questions to be answered as: Will MB quotes offer the same arbitrage opportunities? Will orders be filled before the arbitrage possibility disappers? How to balance lot size of the Forex trade with contract size of the Futures trade and so on.

But I think it's worthwhile to search for an answer and to put the whole idea into a program.

So I wish you, pip-gandalf, best success programming it.

Regards Martin

{kind=link}

Hi all,

Your idea seems interesting.

For your information: We've build a new trading platform which integrates different broker interfaces together (including MBT, Interactive Brokers, all PATS-Platform brokers and FIX-Engines) where you can trade with different brokers from one application.

In case this idea works, we can develop an EA which would work with an MT-Broker together with an other broker. Of course would all this be free of charge. Please PM in case of interest.

Good trades!

Mr. Krebs

Broker Arbitrage

I had already heard about the concept of arbitrage in forex, triangular arbitrage and so on, but what about a full auto routine that compares different quotes from different brokers and when there is a discrepancy the software opens a trade and closes it when the price is aligned to the price of the other brokers (or whenever you like)?

For example 3 brokers quotes eur/usd 1.3500 and 1 broker 1.3490. Open buy 1.3490 and close 1.3500

Full auto

Would it be something doable in real market?

I was thinking about it because it would be risk free...

Anybody wants to try it?

I can link you to the owner.

pm me or email me

Anybody wants to try it?

I can link you to the owner.

pm me or email meHello Fx_Pro_Trader!

I want to try it if it is connected to arbitrage. But what is it exactly?

Hi all,

Your idea seems interesting.

For your information: We've build a new trading platform which integrates different broker interfaces together (including MBT, Interactive Brokers, all PATS-Platform brokers and FIX-Engines) where you can trade with different brokers from one application.

In case this idea works, we can develop an EA which would work with an MT-Broker together with an other broker. Of course would all this be free of charge. Please PM in case of interest.

Good trades!

Mr. KrebsHello Mr. Krebs,

What about this new trading platform? Have you finished it? Where can I see it? Could you give me a link?

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Yesterday I took a Quote-Video during US Trade Balance news time.

See thread: https://www.forex-tsd.com/forum/commercial-talks/3241-best-news-broker#comment_78548

and http://home.arcor.de/cam06/vids/

Analysis of this video made me think about a possible arbitrage profit, supposed you have got an account with Oanda (https://fxtrade.oanda.com/) and a Broker (InteractiveBrokers or MB Trading for example) where you can trade CME (http://equivalentsrdc.cme.com:443/index.html?) Globex Futures.

As shown in attached screenshots at 14:30:02cet = 08:30:02est you could buy GBP for 1.9040 at Oanda and sell equivalent Futures for 1.9052 at CME.

A 12 points gain!

This situation didn't change till 14.30.08, so that you got 6 seconds to execute the appropriate trades.

Since you can take it for sure, that the equivalent futures after some time will be back insice Onada's spread this trade seems to create a kind of safe profit of 12 points difference - 7 points spread - 2 points comission = 3 points safe arbitrage profit.

If you can stand a possible move and wait till Oanda's spread is reduced to 2.5 points the arbitrage profit would even grow to about 8 points.

So far my consideration.

If anybody has got pracitcal experience with such trades a detailed explanation would be nice.

Regards Martin

-----