Discussion of article "The Optimal Method for Calculation of Total Position Volume by Specified Magic Number"

There is one question: what will happen if one EA loads the whole history and starts counting from 1000 position to 0, and the other previously launched at this time will request loading from the place it knows (for example, from 1000 to 900), the history will be cut and the first will stumble at 900 position and will not go further.

Therefore, I advise you to reconsider the algorithm in the direction of full history loading (or somehow to provide synchronisation that until one has not finished its calculations the second does not request history).

There is one question: what will happen if one EA loads the whole history and starts counting from 1000 position to 0, and the other previously launched at this time will request loading from the place it knows (for example, from 1000 to 900), the history will be cut and the first will stumble at 900 position and will not go further.

Therefore, I advise you to reconsider the algorithm in the direction of full history loading (or somehow to provide synchronisation that until one has not finished its calculations the second does not request history).

Everything will be fine! And if not, everything will be very bad. © "The Last Armoured Train".

Do you think tasks are parallelised line by line?

I tried to run a long loop on one symbol in two Expert Advisors now, no wedging occurs.

Everything's gonna be okay! And if not, everything will be very bad. © "The Last Armoured Train".

Do you think tasks are parallelised line by line?

I tried to run a long loop on one symbol in two Expert Advisors now, no wedging occurs.

Lottery, that's why I gave up the approach of partial history loading when a similar problem started to appear.

ZY in general, pay attention to the problem is there, to test it, make an Expert Advisor that on each tick will load history to a random depth, open the history tab with the running Expert Advisor and see what happens.

Lottery, that's why I gave up the approach of partial history loading when a similar problem started to appear.

ZY in general, pay attention to the problem is there, to test it, make an Expert Advisor that on each tick will load history to a random depth, open the history tab with the running Expert Advisor and see what happens.

Let anything happen there, the main thing is that other EAs do not interfere with the work of the cycle.

Let anything happen there, the main thing is that there should be no interference of other Expert Advisors in the work of the cycle.

There can only be a guarantee if all EAs work in the same thread,

but this is not the case and each EA works in its own, so it's only a matter of time before problems arise.

There can only be a guarantee if all advisors work in the same thread,

but that's not the case and each EA is running in its own, so it's only a matter of time before problems arise.

You can fantasise endlessly about how a computer works.

You can fantasise endlessly about how a computer works.

I don't understand your position, do you want me to give you a code where this problem will be explicitly expressed? (so I won't waste my time on it).

I've shown you the weak point where I was wrong myself (and spent more than one day on catching the error), and it's your right to react or not.

I don't understand your position, you want me to give you a code where this problem will be explicitly expressed? (so I won't waste my time on it).

I showed you the weak point where I was wrong myself in my time (and spent more than one day to catch the error), and it's your right to react or not.

Exactly. If you claim something, you have to prove it.

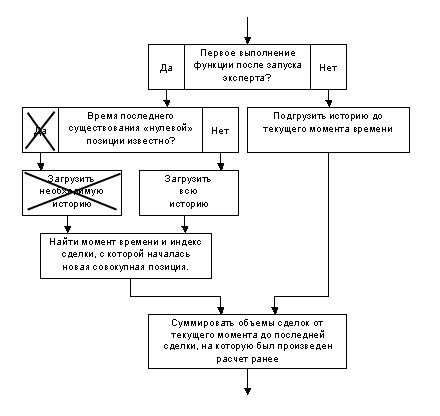

When several Expert Advisors work on one symbol, the unsolvable in general case problem "Counting the fixed profit by each Expert Advisor separately" arises. In a special case (when a pair contains a deposit currency) the problem is solved.

The problem is not very serious, but, as they say, the residue remains....

- www.mql5.com

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

New article The Optimal Method for Calculation of Total Position Volume by Specified Magic Number is published:

Author: Дмитрий