|

6+ years

experience

|

0

products

|

0

demo versions

|

|

0

jobs

|

0

signals

|

0

subscribers

|

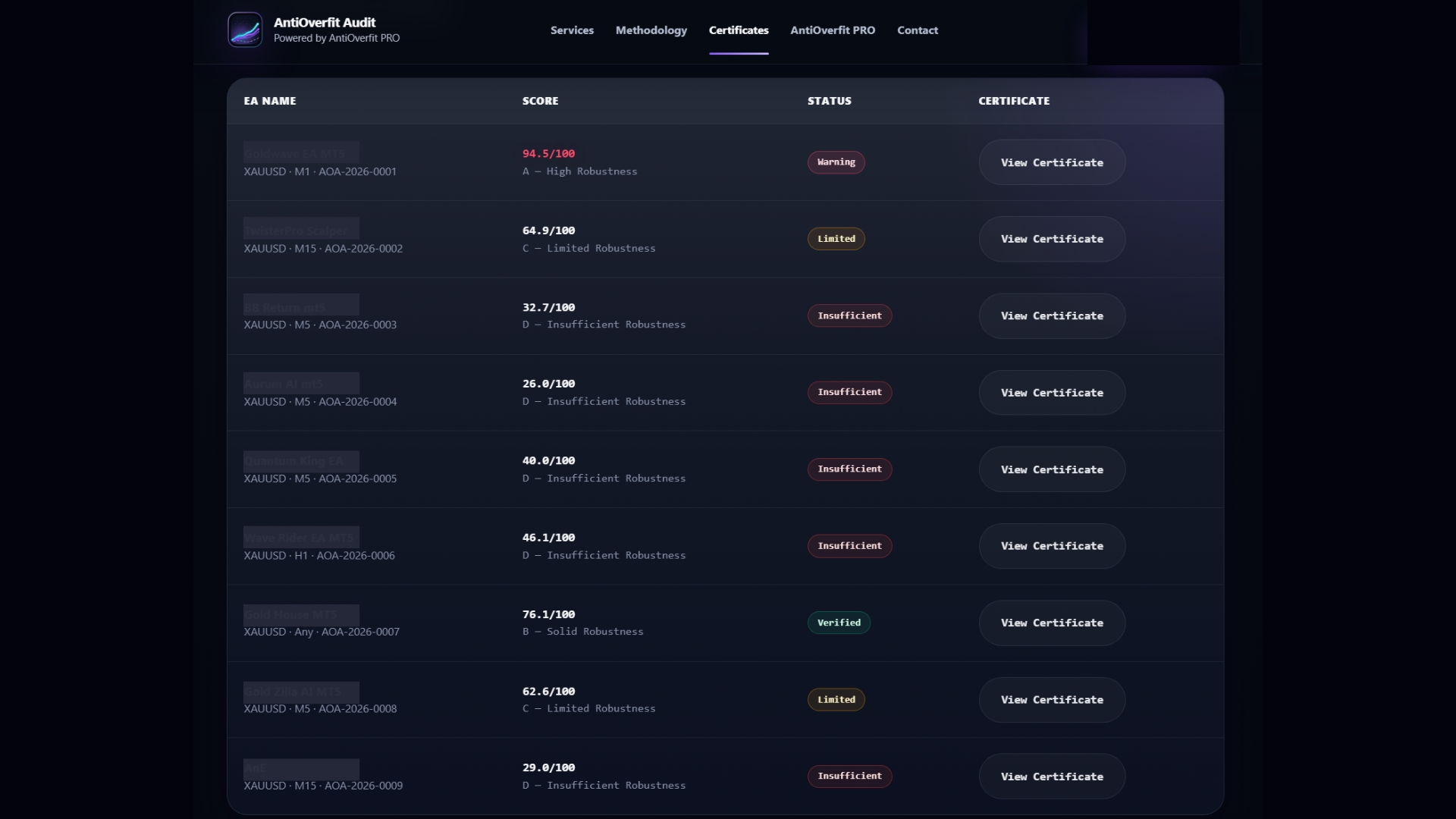

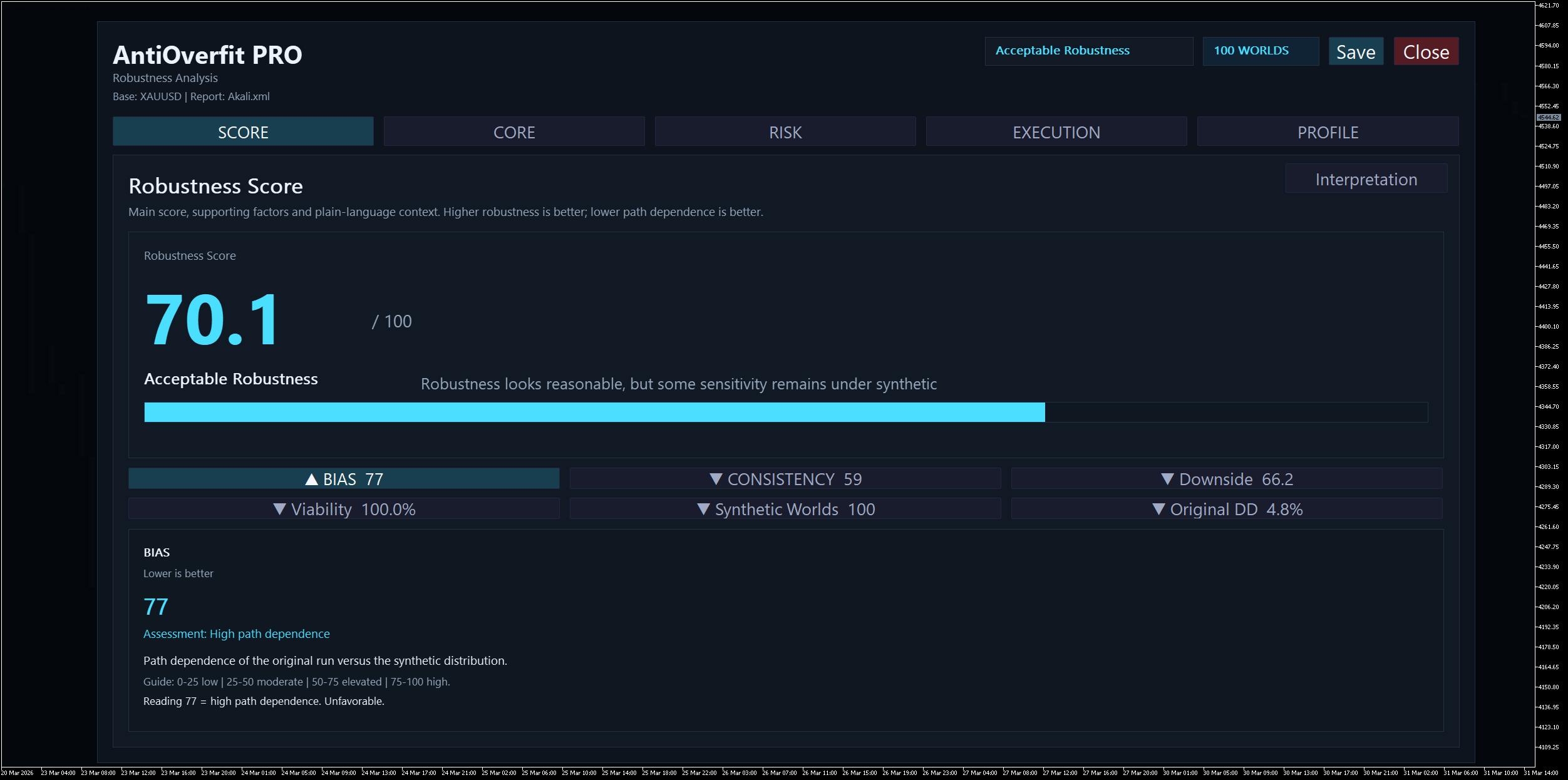

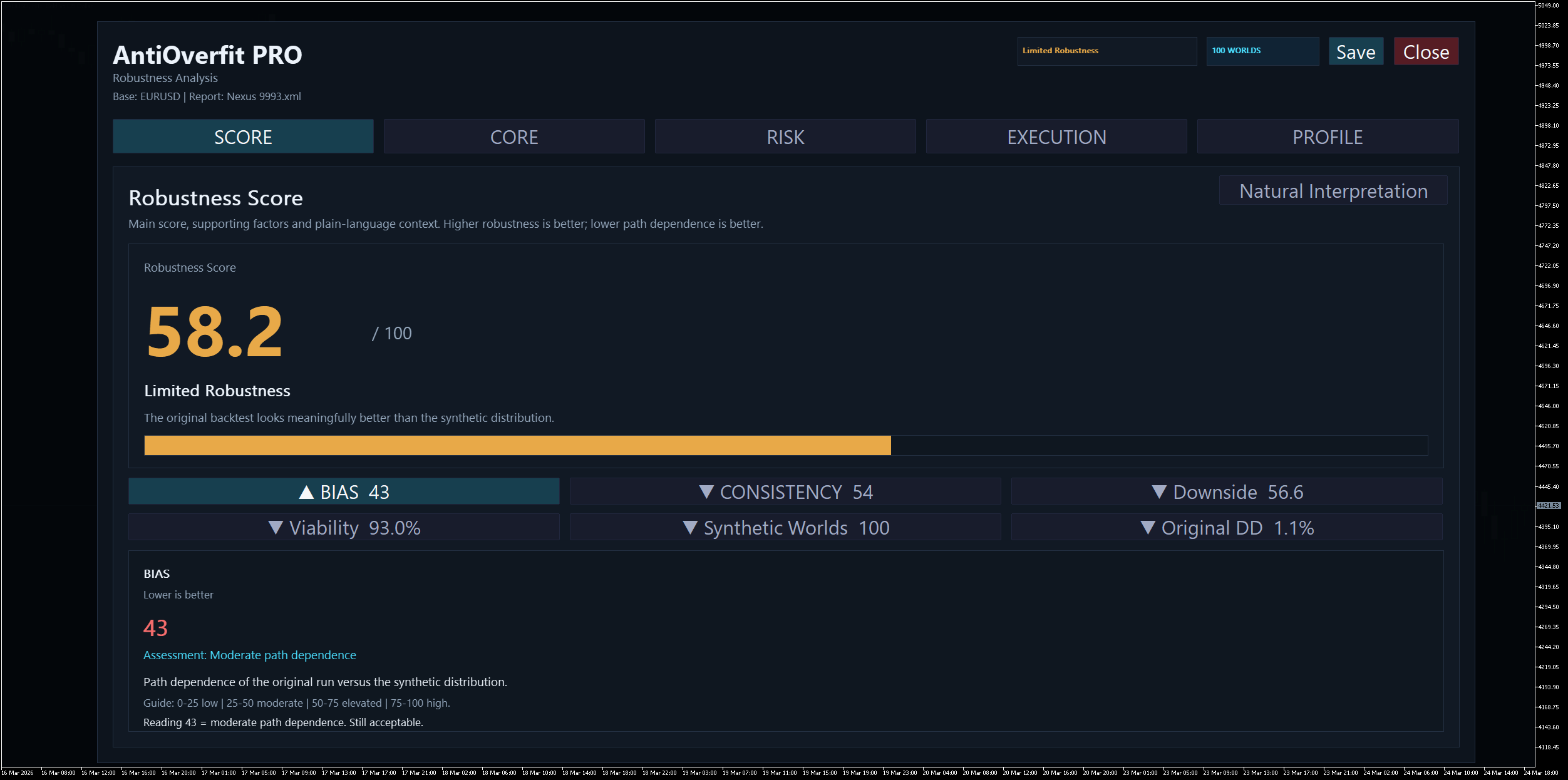

AntiOverfit PRO guide: https://www.mql5.com/en/blogs/post/768007