NZDUSD Technical Analysis 2015, November: ranging bearish with symmetric triangle pattern to be formed for direction

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.11.07 07:29

Forex Weekly Outlook Nov. 9-13 (based on forexcrunch article)

The US dollar surged across the board as a December rate hike looks very real. Employment data from the UK and Australia, speeches from Mark Carney and Mario Draghi, German GDP data , US Retail sales stand out. These are the main events on forex calendar.

The US Non-Farm Payrolls report for October showed strong growth with a 271,000 payrolls increase following two straight months of lukewarm gains. The unemployment rate declined to a 7-1/2-year low of 5.0%, demonstrating domestic strength. This robust reading may signal the well-awaited rate hike announcement in the Fed’s next meeting in December which was also evident in recent Fed talk. Another encouraging piece of news is the wage gains and robust consumer spending, showing an upbeat picture of the economy on the verge of the fourth quarter.

- UK Employment data: Wednesday, 9:30. The U.K. labor market continued to improve in the third quarter, posting the lowest unemployment rate since the second quarter in 2008. The unemployment rate stood at 5.4% compared to 5.5% in the three months to July. Wages including bonuses grew 3% indicating a growth trend in the UK economy. However, the number of jobless claims increased 4,600 in September, missing forecasts for a 2,300 contraction. The number pf jobless claims is expected to rise by1,600 this time.

- Mark Carney speaks: Wednesday, 10:30. BOE Governor Mark Carney will speak in London about theInflation Report released last week. Following the statement Carney suggested interest rates would stay lower for a longer period, hinted they would rise in about two years. He said global growth has weakened since the previous inflation report which could weigh on UK growth. As to inflation forecast, the bank downgraded its growth outlook slightly, to around 2.7% for 2015 from 2.8% in the last report. Mr Carney stated that if rates did not rise until the first half of 2017, inflation is predicted to overshoot its 2% target.

- Mario Draghi speaks: Wednesday, 13:15. ECB President Mario Draghi is due to speak in London. He may provide further information regarding his recent declaration that the ECB is prepared to cut interest rates and step up quantitative easing prevent a renewed economic slump in the Eurozone. Draghi stated that the ECB policymakers would not be in “wait and see” mode, but rather “wait and assess” mode, between now and their policy meeting on 3 December.

- Australian Employment data: Thursday, 0:30. Australia’s employment market contracted 5,100 jobs in September missing forecasts for a 5,000 rise. 13,900 full-time workers were dismissed, while 8,900 part-time jobs were added. The participation rate, fell to 64.9% from 65.0% in August. However, the jobless rate remained steady at 6.2%. Economists expect jobs growth may slow due to soft economic conditions and the jobs growth from the labor services sector will weaken amid less support from housing activity and lower currency. Australia’s labor market is expected add 15,200 jobs while the unemployment rate is predicted to remain at 6.2%.

- US Unemployment Claims: Thursday, 13:30. US jobless claims were weaker than expected last week, reaching 276,000 after posting 260,000 in the prior week. Analysts expected the number of claims would come to 263,000. However, the number of claims remain low from historical perspective showing solid labor market conditions with previous and continuing unemployment claims, which are around decade’s lows.

- German GDP: Friday, 7:00. Germany’s economy expanded 0.4% in the second quarter according to August estimates. Exports climbed 2.2% in the three months through June. Private consumption advanced 0.2%, while capital investment contracted 0.4%. Germany faces downturn risks in exports due to the weakness in China, Germany’s third-biggest trading partner. Nevertheless, German manufacturing sector continued to grow and consumer spending remained strong amid record-low unemployment and borrowing costs. Economists expect GDP to grow by 0.3% in the third quarter.

- US Retail sales: Friday, 13:30. U.S. retail sales registered weak performance in September, rising 0.1%, while expected to gain 0.2%. Excluding autos, core retail sales declined 0.3%. Sales of motor vehicles and auto parts edged up by 1.7%. Gasoline sales, meanwhile, declined 3.2%. Consumer spending is the largest contributor to the U.S. gross domestic product. Weaker consumption means a hit to GDP growth. Retail sales are expected to gain 0.3% in October and Core sales are expected to rise by 0.4%.

- US PPI: Friday, 13:30. U.S. producer prices plunged in September to their lowest level in eight months amid a decline in prices of energy products. Producer price index fell 0.5%, after being unchanged in August. In the 12 months through September, the PPI dropped 1.1% after declining 0.8% in August. Weak inflation one of the key reasons for the Fed’s reluctance to raise interest rates. Producer prices are expected to grow by 0.1% this time.

- US UoM Consumer Sentiment: Friday, 15:00. U.S. consumer sentiment rebounded sharply in October, indicating that the economic recovery remained positive despite headwinds from a strong dollar and weak global demand weighing on the industrial and the manufacturing sectors. The University of Michigan consumer sentiment index edged up to 92.1 from 87.2 in September. Analysts expected a lower reading of 88.8. It is a hopeful sign on the outlook for consumer spending. U.S. consumer moral is expected to reach 91.2 in November.

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.11.13 17:33

Forex Weekly Outlook November 16-20 (based on the article)

The US dollar had a mixed week after the NFP. Japan GDP data, Inflation data from the UK, the US and Canada and a rate decision in Japan stand out. These are the main events on forex calendar. Here is an outlook on the market-movers for this week.

A long list of Fed speakers basically left expectations for a Fed hike unchanged, thus leaning towards a move in December. Yellen remained silent. In the euro-zone. Data was mixed, with a disappointment in retail sales but upbeat consumer confidence also a positive JOLTs report, Draghi reiterated his desire to act in December: provide more easing. In Australia, the jobs report was excellent and falling oil prices weighed on the Canadian dollar.

- Japan GDP data: Sunday 23:50. Japan’s economy contracted 0.4% in the second quarter, when Gross domestic product declined by an annualized 1.6% between April to June. The contraction was less than expected, but consumer spending and investments weakened. Many economists believe inflation will not reach the 2% target by summer 2016 expecting further monetary easing in the coming months. GDP is expected to remain negative at -0.1%.

- Mario Draghi speaks: Monday. 10:15 and Friday, 8:00. ECB President Mario Draghi will give speeches in Madrid and in Frankfurt. During his talk before the European Parliament last week, Draghi dropped another hint that the ECB is preparing further monetary easing measures to boost the Eurozone’s recovery. The ECB president admitted that the 2% inflation target will take longer to achieve and that the central bank will re-examine a QE program in early December. Market volatility is expected.

- UK inflation data: Tuesday, 9:30. UK Consumer Prices fell to -0.1% in September hovering close to zero for most of this year. Food prices declined by 2.5% in the year amid ongoing supermarket price wars. According to the low CPI release, the Bank is in no hurry to raise rates anytime soon. Furthermore, core CPI also remained weak at 1.0% suggesting no underlying inflationary pressures despite continuing strength in wage growth. Consumer prices are expected to remain at -0.1%.

- German ZEW Economic Sentiment: Tuesday, 10:00 German analysts and investors sentimentplunged in October to 1.9 points, following 12.1 in September amid the scandal at Volkswagen and the weakness in emerging markets. Analysts expected a reading of 6.8. Current conditions declined to 55.2 points from 67.5 points in September, below expectations for a drop to 64.7. German economic sentiment is expected to reach 6.7% this time.

- US inflation data: Tuesday, 13:30. Consumer prices in the U.S. declined 0.2% in September while Core CPI excluding the volatile food and energy sectors gained 0.2%. Analysts expected CPI to drop 0.2% and Core CPI was predicted to rise by 0.1%. Despite the fall in headline inflation, core prices edged up 1.9% in the past 12-months, from 1.8% the prior month getting closer to a December rate hike call. The energy index plunged 4.7% in September. A continued decline in the gasoline index, this time by 9%, was the main cause in the decline for overall CPI. Both CPI and Core CPI are forecasted to rise 0.2% in October.

- US Building Permits: Wednesday, 13:30. Building permits declined 5% to a 1.1 million pace in September the lowest number since March. Meanwhile, applications for single-family projects declined 0.3% to a 697,000 unit pace; indicating this component will come to a standstill in the coming months. However, housing starts were encouraging consistent with the builders increasing confidence in the outlook for their industry. The number of permits is expected to reach a unit pace of 1.15 million in October

- US FOMC Meeting Minutes: Wednesday, 19:00. In the Fed’s October decision, the tone was relatively hawkish regarding inflation and employment, not expressing real worries. In addition, they provided a hint about action in December. The minutes may reveal how hawkish the members really are and how close a December hike is real. Note that the excellent NFP was released in the meantime, and that the Fed edits the minutes until the last minute before the publication. Markets always move by any wording nuances.

- Japan rate decision: Thursday. The Bank of Japan maintained its monetary policy, refraining from adding further stimulus at its policy meeting in October. However, the members reiterated their promise to increase the monetary base at an annual rate of 80 trillion yen ($660 billion). At the Press conference, following the meeting, BOJ Governor Haruhiko Kuroda said there were no proposals to ease monetary policy during the meeting, and blamed the low energy prices for the failure to achieve the BOJ’s inflation target.

- US Unemployment Claims: Thursday, 13:30. New U.S. applications for unemployment benefits remained unchanged last week, indicating strong labor market conditions. The data was worse than the 270,000 forecasted but still supports the Federal Reserve call to raise interest rates next month. The four-week moving average of claims rose 5,000 to 267,750 last week, still close to a 42-year low. The number of people continuing to receive benefits after an initial week of aid increased 5,000 to 2.17 million last week. Jobless claims for this week are expected to reach 272,000.

- US Philly Fed Manufacturing Index: Thursday, 15:00. The Philadelphia manufacturing index remained in negative territory for the second month in a row reaching -4.5 in October after posting -6 in the prior month. The negative figures show sharp slowing in the manufacturing sector. The strength of the US dollar has been weighing on US industry since last fall, making products less competitive in the global market. Philadelphia manufacturing index is expected to rise to 0.1 in November.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

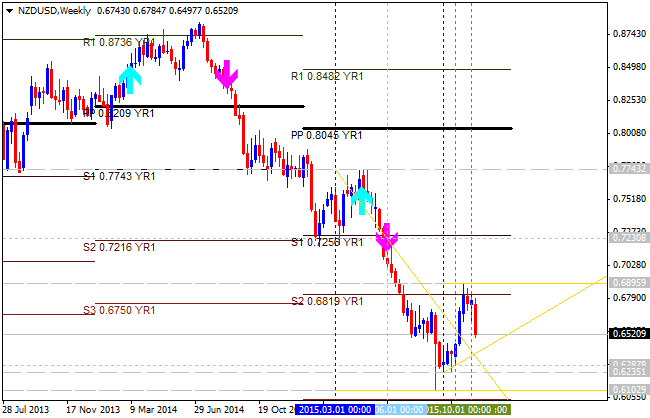

The price is on bearish market condition with the secondary ranging within the following key support/resistance levels:

Intermediate support levels for this pairs are the following: 0.6287 and 0.6235.

W1 price is on ranging bearish market condition:

MN price is on bearish breakdown for 0.6102 as the real bearish target.

If W1 price will break 0.6895 resistance level so the reversal from the primary bearish to the primary bullish market condition will be started.

If W1 price will break 0.6235 support level so the primary bearish trend will be continuing up to 0.6102 level as the next bearish target.

If W1 price will break 0.6102 support level so we may see good breakdown possibility.

If not so the price will be ranging within the levels.

SUMMARY : bearishTREND : ranging