LET'S SAY THAT ... - page 5

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

Если приращения случайны, то цена - это random walk, она имеет нормальное распределения, и заработать на ней гарантированно нельзя.

Однако надо оговорить природу приращения, сказать просто "случайная" - не сказать ничего. В жизни всё случайно. У автобуса есть расписание, но время его прибытия величина случайная. Случайные приращения цены могут быть коррелированы с фазами луны, например, это не делает их неслучайными.

Чтобы получить random walk приращения должны быть iid независимыми и одинаково распределёнными.

That's the thing: the price increment is not normally distributed. Otherwise it would be guaranteed to make money on it.

В том то и дело, что приращение цены не нормально распределено. Иначе заработать на нем было бы гарантированно можно.

relative to what are the abnormal increments?

В том то и дело, что приращение цены не нормально распределено. Иначе заработать на нем было бы гарантированно можно.

The price increment can be assumed to be normally distributed, which is close enough to reality, but it does nothing if it is iid . The price increment can be considered as t-distributed with degrees of freedom 4 or 5. This is much closer to reality than assuming that the increments are normal.

The resulting process will be a random walk. It is guaranteed to be normally distributed regardless of the distribution of the increments, but normality does not help - you cannot make money on a random walk. Price increments can be considered stationary, but they cannot be traded. You can trade the price, and it is a random walk, a non-stationary process. At least in the context of this topic.

Приращение цены можно считать нормально распределённым - это достаточно близко к реальности, однако это ничего не даст, если оно iid . Можно считать приращение цены t-распределённым со степенью свободы 4 или 5. Это гораздо ближе к реальности, чем допущение о нормальности приращений.

Результирующий процесс будет random walk. Вот он-то вообще гарантированно нормально распределённый, независимо от распределения приращений, но от той нормальности никакого прока - нельзя заработать на случайном блуждании. Приращение цены можно считать стационарными, но их нельзя торговать. Торговать можно цену, а она random walk, процесс нестационарный. По крайней мере в контексте данного топика.

Can I argue a little to keep the discussion going? I'm not very sure what I want to say right now. Especially now it is very late. But still... If the increments of some quantity are normally distributed, it means that this quantity is bounded. (Am I wrong?).

Unless the previous statement is wrong, there is a maximum and a minimum value in the set of values of a quantity. Also, the closer the value of a value is to the maximum or minimum, the more likely it is to change towards the mean. This is the law that can be used.

p.s. Don't think I'm attacking. Just want to have a conversation with an intelligent person.

Можно я для поддержания дискуссии немножко поспорю? Я сейчас сам не очень уверен в том, что хочу сказать. Тем более уже очень поздно. Но все-таки... Если приращения какой-то величины нормально распределены, то это значит, что эта величина ограничена. (Ошибаюсь?)

Если не ошибся в предыдущем утверждении, то во множестве значений величины есть максимумальное и минимальное. Кроме того, чем ближе значение величины к максимальному или минимальному, тем больше вероятность его изменения в сторону среднего. Вот это и есть закон, который можно использовать.

п.с. Не подумайте, что я нападаю. Просто хочу поговорить с умным человеком.

Have you not heard about the arcsine theorem and player error?

I didn't ask about the relativity of deflection for nothing.

If it returns - one song.

MA(x period) is a different tune...

If you use TrueDMA instead of MA - a completely different cacaphony will befall you.

;)

Where did you get abnormality?

Don't ask anyone, they don't say a word.

There's a topic - it shows the opposite.

Yo my...

:)

Можно я для поддержания дискуссии немножко поспорю? Я сейчас сам не очень уверен в том, что хочу сказать. Тем более уже очень поздно. Но все-таки... Если приращения какой-то величины нормально распределены, то это значит, что эта величина ограничена. (Ошибаюсь?)

Если не ошибся в предыдущем утверждении, то во множестве значений величины есть максимумальное и минимальное. Кроме того, чем ближе значение величины к максимальному или минимальному, тем больше вероятность его изменения в сторону среднего. Вот это и есть закон, который можно использовать.

п.с. Не подумайте, что я нападаю. Просто хочу поговорить с умным человеком.

You are definitely wrong. The nature of the distribution says nothing about the limitation of the value. There are probably some exceptions, but in general this is the case. Limitations are imposed by the parameters of the distribution. For example: the normally distributed prevalence is ~N(0,1). It's a stationary process, it has magnitude limits, it will almost never reach 4 or -4.

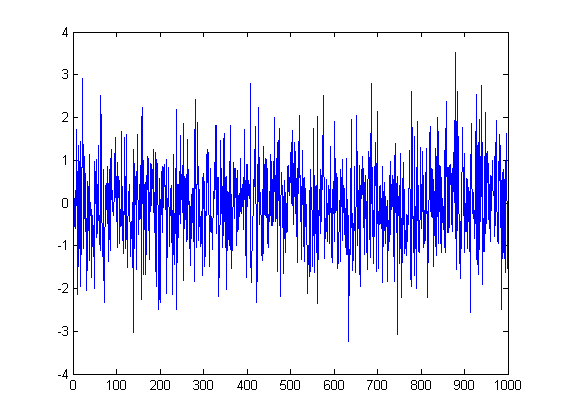

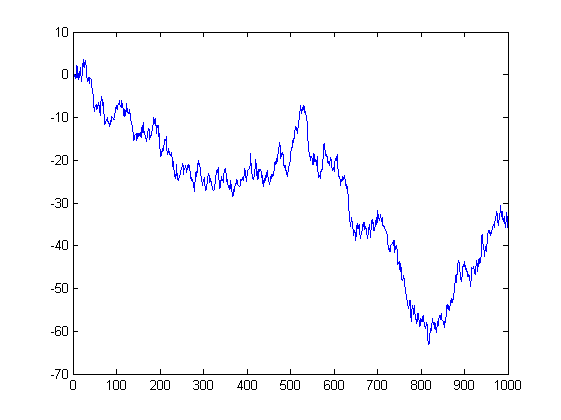

And here's the price that comes out of those increments. It's a random walk. It too has a normal distribution ~N(0,sigma^2), but its variance parameter is not a constant, but increases with time, i.e. the number of increments. Naturally, this process has no magnitude limit and will visit all points with equal probability. This is the basis of the gambler's bankruptcy problem - if you play long enough in a perfectly fair game (50:50), you will still lose, because sooner or later this curve will lead you lower than you have money.

And here's 1,000 random wanderings, you can obviously see the bell of the normal distribution.

But what you say about returning to the mean is a different story, it's a mean-reverting process - autoregressive (AR)

x(i) = a * x(i-1) + e(i). The e(i) transformation is ~N(0,1), a < 1.

If you've found a tradable mean-reverting process, then there's only time to haul away baskets of cabbage. Naturally, it depends on the parameters - the rate of return to the mean (a) - but either way it's cool.

А вот 1000 случайных блужданий, очевидно виден колокол нормального распределения.

you have to light up the frequencies of the hits.

--

the expanding double King(log) Bell.

;)

не всякий увидит.

You have a histogram and a probability plot for the 1000th sample.

Although, since the increments were normal, the sum of normal distributions is a normal distribution. You don't even need to check anything.

На тебе гистограмму и пробабилити плот для 1000-го отсчёта.

Хотя исходя из того, что приращения были нормальные, сумма нормальных распределений есть нормальное распределение. Тут ничего даже и проверять-то не надо.

Sens!

Good (or rather - and visually useful;) work.