Put in a good word about the occasional wanderer... - page 2

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

Если параметры распределений Б и С различны, то формулы для вычисления МО и дисперсии будут сложнее, но все равно будет такое же распредление

This is if C and B have a stable distribution. In that case, yes, the sum of the stable distributions equals a stable distribution. Otherwise, no, the sum or difference of C and B with different distributions will have a hell of a distribution.

Если оба процесса независимые, то оба они просто шум. Если ты складываешь или вычитаешь два шума, то получаешь просто третий шум. Т.е. результирующий процесс будет

y(i) = y(i-1) + e(i), где e(i) = b(i)+s(i) или e(i) = b(i)-s(i); + или - это не имеет значения.

Случайное блуждание чистой воды. Мелкие модификации, типа типа обрезания паникёров, серьёзно ничего не изменят. Только если твои процессы будут не независимые, то могут начаться чудеса.

Thank you for your reply.

Can I introduce one more amendment to the algorithm?

If the hero has had his "increment" - his powers and doubts are doubled.

How then would this random praxiological process look?

Knowing what you have modelled similarly - can you look at the bell/pipe?This is if C and B have a stable distribution. In that case, yes, the sum of the stable distributions equals a stable distribution. Otherwise, no, the sum or difference of C and B with different distributions will have a hell of a distribution.

We are talking about modelling random walks, which is usually done with stationary distributions - normal or discrete. We can probably work around it and model it as non-stationary. The sum or difference of non-stationary distributions will also be non-stationary as a rule, although there are exceptions that underlie cointegration e.g.

Спасибо за ответ.

можно ввести еще одну поправку к алгоритму?

Если герой получил свое "приращение" - его силы и сомнения удваиваются.

Как тогда этот случайно праксиологический процесс будет смотреться?

Зная, что вы похожее моделировали - можно колокол/трубу глянуть?I don't really get it. Like y(i) = y(i-1) + e(i) * i, where e(i) = b(i)+s(i)?

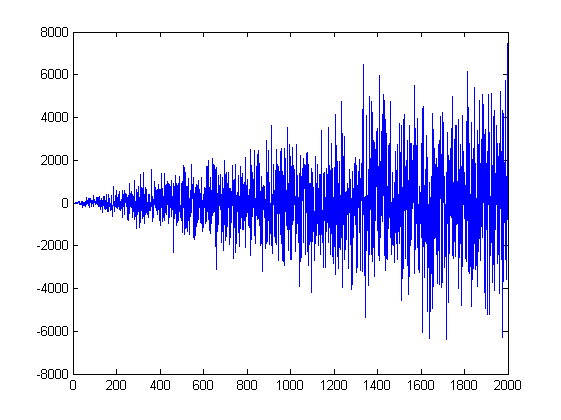

Not doubling, but increasing. The doubling will grow too fast. Even a simple multiplication by i gives this growth of increments

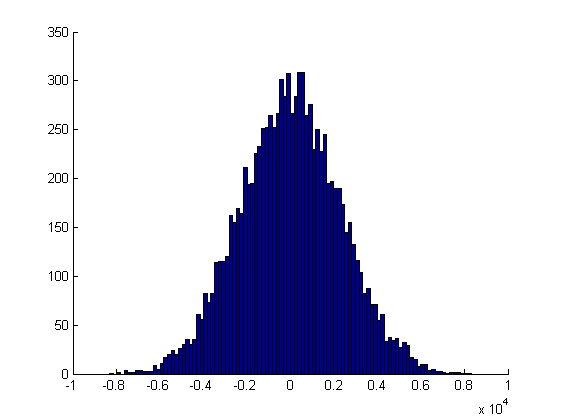

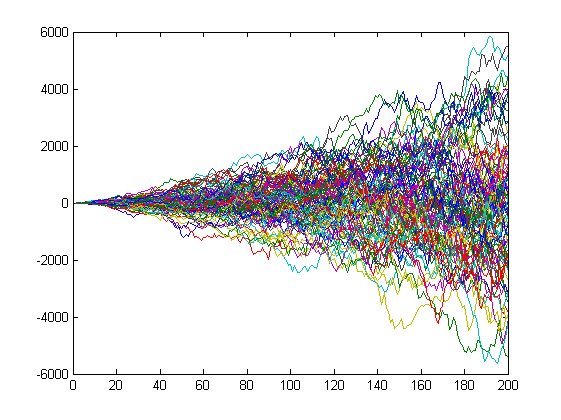

However, the resulting process y(i) remains normal, which is what we would expect from a random walk.

Although it may not seem so at first sight, this is only due to the change in scale

Не очень понял. Типа y(i) = y(i-1) + e(i) * i, где e(i) = b(i)+s(i)?

Не удваивается, но возрастает. Удваивание слишком быстро вырастет. Даже простое умножение на i даёт вот такой рост приращений

Однако, результирующий процесс y(i) остаётся нормальным, чего мы и ожидаем от случайного блуждания.

Хотя оно так может и не кажется на первый взгляд, но это только из-за изменения масштаба

About doubling is the following "practical" observation.

If in the previous step the hero got the desired increment (i.e. |y(i)-y(i-1)|>= hero's strength in the i-th step, then his generated strength (including minus - doubt) in the i+1 step should be doubled.

Here the arcsine should amplify, but I'm not sure. The sign-variance gets in the way ;)

---

A cheeky request - increase the length of the implementation to 500. fire

На форуме часто в пылу дискуссии утверждается, что блуждание цены абсолютно случайно.

Пускай не всегда. Но случайность и не... сложно якобы отличить.

Теоремы арксинуса и двойного логарифма периодически обсуждаются или цитируются напрямую, либо только выводы.

Мутно как то...

У меня вопрос к теоретикам и практикам.

Изучал ли кто "блуждание после соударения"?

Постановка задачи следующая - есть два условных героя "БАЙ" и "СЕЛ".

Пускай генерится некое приращение для каждого из них.

В зависимости от героя назовём их "наступательным приращением" и "оборонительной силой".

...

There should be a footnote here: if the increment is offensive, it must by convention take precedence over defensive increments in mobility,

Either a constant should be added to the RPM after generation or a shifted range of RPM should be set.

Then we will have one offensive and one defensive, otherwise how do we know who is on the defensive?

About doubling is the following "practical" observation.

If in the previous step the hero got the desired increment (i.e. |y(i)-y(i-1)|>= hero's strength in step i, then his generated strength (including minus - doubts) in step i+1 should be doubled.

Here the arcsine should amplify, but I'm not sure. The sign-variance gets in the way ;)

Are you hoping to determine (or rather, to fit) the market distribution by such a coffee-leaved guessing?

супер!

О удваивании следующее "прак...ое" наблюдение.

Если на предыдущем шаге герой получил желаемое приращение (т.е |y(i)-y(i-1)|>= сила героя на i-том шаге, то его сгенерированную силу ( в том числе с минусом - сомнения) на i+1 шаге следует удвоить.

There is no point. Such manipulation will change the distribution of the increments, it will grow large tails, even if B and C were normally distributed, but it will not change the nature of the resulting process - it will still be a random walk and will be normally distributed. A random walk does not care about the distribution of the increments as long as the third moment is zero, i.e. it is symmetric.

речь о моделировании случайных блужданий, что делается как правило стационарными распределниями - нормальным или дискретным. Можно наверное изголиться и смоделировать нестационарным. Сумма или разность нестационарных распределений будет так же нестационарна как правило, хотя есть исключения, которые лежат в основе коинтеграциии например

Don't confuse warm and soft, i.e. stationarity with distribution. They are not related in any way. A random walk has a normal distribution, but it is not stationary. A uniform distribution is stationary, but the sum of two uniform distributions will not be a uniform distribution. This is a property (to retain the type/shape of the distribution under any linear manipulation) only of stable distributions.

Don't confuse warm and soft, i.e. stationarity with distribution. They are not related in any way. A random walk has a normal distribution, but it is not stationary. A uniform distribution is stationary, but the sum of two uniform distributions will not be a uniform distribution. This is a property (to retain the type/shape of the distribution under any linear manipulation) only of stable distributions.

How is it not related? The normal distribution is stationary and the SB increments distributed by NR are stationary, and I was originally talking about the increments.

Regarding SB itself (as cumulative sum of increments): there will be no "heavy tails" as you described in the previous post. Because SB itself at time t is also normally distributed, but with variance t times larger than for one increment (at time t from the origin). Yes, the variance of the SB distribution increases as time increases. Heavy tails over 3 sigmas for example, but for SB if you calculate the variance at a particular time (and you can do it analytically) it will be as for normal.

I agree that the SB process itself is not stationary, it is an inegraded process with unit root I(1), i.e. the first difference (increments) are distributed stationary https://www.mql5.com/go?link=http://window.edu.ru/catalog/pdf2txt/141/28141/11363?p_page=55 But a non-stationary distribution does not necessarily have heavy tails and in this case there will be none

Do you think HP is non-stationary? Or can't you say for every continuous distribution whether it is stationary or not? :)