AUDUSD Technical Analysis 2014 20.04 - 27.04: Correction To Be Started

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.04.18 22:34

Forex Fundamentals - Weekly Outlook Apr. 21-25The pound and the dollar emerged as winners in a week that saw the euro and the yen retreat. US housing data, the rate decision in New Zealand, German business sentiment, US Durable Goods Orders and Unemployment Claims are the main highlights on Forex calendar. Here is an outlook on the market-movers for this week.

The US economy emerged from the cold winter registering gains in retail sales and manufacturing activity as well as continuous improvement in the labor market. . The Philly Fed Index exceeded expectations in April, providing more evidence of a spring bounce. Overall, the US economy is steadily advancing. In the euro’zone, Mario Draghi managed to send the euro down in a Sunday gap, and the common currency never recovered. GBP enjoyed a sharp drop in the UK unemployment rate to reach new multi year highs. The kiwi stayed behind after weak inflation figures and the loonie took the other direction on positive ones

- US Existing Home Sales: Tuesday, 14:00. U.S. existing home sales declined slightly in February to a 19 month-low reaching an annual rate of 4.60 million units, following 4.62 million in January. A combination of cold weather and dwindling inventory of homes for sake, discouraged potential buyers. Economists expected a higher figure of 4.65 million. However, as the cold winter is over, analysts believe the pace of sales will accelerate this time. U.S. home sales are expected to rise to 4.57 million.

- Chinese HSBC Flash Manufacturing PMI: Wednesday, 1:45. The independent purchasing managers’ index is considered one of the most reliable gauges for the Chinese economy, the world’s no. 2 economy. After a disappointing drop to 48 points, a small rise to 48.4 is expected. Note that this is below the 50 point mark separating growth and contraction.

- US New Home Sales: Wednesday, 14:00. The number of transactions for buying new U.S. homes in February declined to 440,000 (annualized) due to the unusually cold winter. Sales of new homes declined 3.3% from a revised rate of 455,000 in January. Nevertheless, economists forecast a pick-up in sales this spring. A further improvement in the US job market and a better consumer confidence will help boost numbers in March. New home sales are expected to reach 455,000.

- NZ rate decision: Wednesday, 21:00. The Reserve Bank of New Zealand raised its official cash rate by 25 basis points to 2.75%, in line with market forecast. RBNZ Governor Graeme Wheeler said in a statement that inflation pressures have increased and expected to continue doing so over the next two years. Raising rates was important to keep inflation under control. Wheeler left the door open for further rate hikes within the next two years. The Reserve Bank of New Zealand is expected to raise its benchmark rate to 3%. Recent weak inflation data suggests that the RBNZ may become somewhat more dovish.

- German Ifo Business Climate: Thursday, 8:00. German business sentiment declined for the first time in five months in March reaching 110.7 from 111.3 in February, amid the Russian- Ukraine conflict. Businesses are worried that this ongoing crisis might affect Germany’s economic recovery since Germany receives more than a third of its gas and oil from Russia. In case of conflict escalation, many German firms are at danger. German business sentiment is expected to edge down to110.5.

- Mario Draghi speaks: Thursday, 9:00. ECB President Mario Draghi will speak at a conference in Amsterdam. He may comment on the low inflation in the Eurozone. Market volatility is expected. We have seen his heavy hand on the euro and we might see this happen again.

- US Core Durable Goods Orders: Thursday, 12:30. Orders for long-lasting U.S. manufactured goods regained strength in February with a 2.2% increase following a 1.3% decline in the previous month. Meantime, Core durable goods orders increased by 0.2% after posting a 0.9% rise in January, falling below expectations of a 0.3% rise. Economic growth in the first quarter is expected to be weaker than the fourth quarter’s annualized 2.4% rise, due to the cold weather. Orders for transportation equipment increased 6.9% while transportation orders had declined 6.2% in January. Durable goods orders are expected to climb 2.1%, while Core durable goods orders are expected to edge up 0.6%.

- US Unemployment Claims: Thursday, 12:30. The number of new jobless claims registered last week remained low at 304,000, near their pre-recession levels, following 302,000 posted in the previous week. Manufacturing activity has accelerated in April, indicating growth momentum after the cold winter. Economists forecasted jobless claims to reach 315,000. The four-week moving average for new claims, dropped to its lowest level since October 2007 with a 312,000 claims. Jobless claims are expected to increase by 5,000 to 309,000.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.04.21 06:52

Finalizing FTA Deal will See Trade Volumes between Aussie Dollar and Yuan Go up

Australia Prime Minister Tony Abbott is expected to sign the final terms to a trade agreement between China and Australia that will see transactions volumes between yuan and Australian dollar soar and lower the cost of business between the two countries.

Presently, the Aussie is one of the four currencies that can be fully converted into the Chinese yuan. The Chinese government is currently considering turning the renminbi into an international currency, reported the Australian.

The deal to convert the two currencies was signed a year ago though the trading volumes between the yuan and the Aussie dollar have started to stabilize after initially surging. Currency flows are estimated to be worth $US2.5 billion per month, up from around US$300 million before former prime minister Julia Gillard signed the convertibility deal in Beijing.

Analysts had expected the turnover to increase every month as more Australian firms scaled up their Chinese exports. Currently, China is Australia’s No. 1 trading partner, with volumes valued at more than US$130 billion per year.

Other currencies that convert directly to the yuan include the New Zealand dollar, the Japanese yen and the US dollar. The deal between Australia and China ensures Australian export firms can receive payments in the Aussie dollar. The full convertibility lowers the transaction costs involved in using other currencies to settle the payments. Certain exporters say that the agreement cut the transaction costs by 10 percent.

“The trading between the dollar and the renminbi has flatlined over the past couple of months but it will take off again, the next obvious step is to see Sydney become a renminbi hub,” said Andrew Whitford, the head of Westpac in China. “I’m a very strong advocate for Sydney to become that hub. There is certainly a need for that to happen.”

Currently, commodity agreements from Australia to China are paid in US dollars, though the trend points towards increasing use of the yuan to settle them.Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.04.19 12:12

AUDUSD Fundamentals (based on dailyfx article)

Fundamental Forecast for Australian Dollar: Neutral- Australian Dollar Looking to Upbeat CPI Data to Rekindle Up Move

- Firming US News-Flow May Hurt AUD/USD on Narrowing Policy Gap

The Australian Dollar’s month-long winning streak ran into resistance

last week as the build-up in RBA policy expectations stumbled. A Credit

Suisse measure of investors’ priced-in policy bets over the coming 12

months declined for the first time in three weeks. A potentially

conflicting set of fundamental event risk in the week ahead promises to

keep driving policy outlook speculation and keep volatility elevated.

On the domestic news-flow front, the spotlight will be on first-quarter CPIdata.

Expectations suggest the headline year-on-year inflation rate will

rise to 3.2 percent from 2.7 percent recorded in the three months

through December 2013, marking the highest level in over two years.

Data from Citigroup shows Australian economic news-flow has

increasingly outperformed relative to consensus forecasts since

mid-February, suggesting economists are underestimating Australia’s

place in the business cycle.

That opens the door for an upside surprise. Such a result may go a

long way toward rebuilding support on from the RBA policy outlook and

driving the Aussie higher.

Externally, a busy docket of US activity data will help inform bets on

the continuity of the Fed’s effort to “taper” QE asset purchases. Home Sales, Durable Goods Orders and Consumer Confidence

figures are in the spotlight. Economic data outcomes from the world’s

largest economy showed a notable improvement relative to expectations

over the past two weeks. If that trend continues, ebbing doubt about the

continued withdrawal of Fed stimulus. That may highlight the immediacy

of the Fed’s move to narrow the policy gap compared with the RBA’s

apparent preference for inaction in the near term, weighing on AUD/USD.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.04.22 17:00

2014-04-22 14:00 GMT (or 16:00 MQ MT5 time) | [USD - Existing Home Sale]

- past data is 4.60M

- forecast data is 4.57M

- actual data is 4.59M according to the latest press release

if actual > forecast = good for currency (for USD in our case)

==========

U.S. Existing Home Sales Drop To Lowest Level Since July 2012

Existing home sales in the U.S. showed a modest decrease in the month of March, according to a report released by the National Association of Realtors on Tuesday, although the annual rate of sales still came in above economist estimates.

The report said existing home sales edged down 0.2 percent to a seasonally adjusted annual rate of 4.59 million in March from 4.60 million in February. Economists had been expecting existing home sales to drop to an annual rate of 4.56 million.

With the modest decrease, existing home sales fell for the seventh time in eight months and hit their lowest level since July of 2012.

NAR also said the rate of existing home sales is now 7.5 percent below the 4.96 million-unit pace in March of 2013.

The modest monthly decrease came as increases in existing home sales in the Northeast and Midwest were offset by declines in sales in the West and South.

Lawrence Yun, NAR chief economist, noted that current existing home sales activity is underperforming by historical standards.

"There really should be stronger levels of home sales given our population growth," Yun said. "In contrast, price growth is rising faster than historical norms because of inventory shortages."

The report showed that the median existing home price was $198,500 in March, up 5.4 percent from $188,300 in February and up 7.9 percent from $184,000 in the same month a year ago.

NAR noted that distressed homes accounted for 14 percent of March sales, down from 16 percent in February and 21 percent in March of 2013.

"With rising home equity, we expect distressed homes to decline to a single-digit market share later this year," Yun said.

The report also showed that there were 1.99 million existing homes available for sale at the end of March compared to the 1.90 million available for sale at the end of February.

The March housing inventory represents 5.2 month of supply at the current sales pace, up from 5.0 months in February.

Wednesday morning, the Commerce Department is scheduled to release a separate report on new home sales in the month of March.

Economists expect new home sales to climb to an annual rate of 455,000 in March after dropping to a rate of 440,000 in February.

MetaTrader Trading Platform Screenshots

MetaQuotes Software Corp., MetaTrader 5, Demo

AUDUSD M5 :12 pips price movement by USD - Existing Home Sale news event

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.04.20 17:35

Forex - Weekly outlook: April 21 - 25The dollar ended the week higher against the yen on Friday as market sentiment was boosted by easing tensions over Ukraine, while upbeat U.S. economic reports also supported the dollar.

USD/JPY touched highs of 102.57 on Friday, before ending the session at 102.40, rising 0.49% for the week. Trade volumes remained thin on Friday, with most markets closed for the Easter weekend, although markets in Tokyo were open.

Concerns over the crisis in eastern Ukraine eased on Thursday after Russia, Ukraine, the U.S. and the European Union said an agreement on steps to "de-escalate" the crisis had been reached.

The dollar also received a boost after upbeat U.S. data on manufacturing and employment on Thursday pointed to underlying strength in the economy.

The Labor Department reported the number of people filing for unemployment benefits edged up to 304,000, below analysts’ forecasts and not far from the six-and-a-half year low of 300,000 touched the previous week.

GBP/USD edged up 0.06% to 1.6798 at Friday’s close, and ended the week 0.45% higher. The pair rose to highs of 1.6840 on Thursday, the strongest since November 18 2009. Sterling strengthened broadly after data earlier in the week showed that the U.K. unemployment rate fell to a five year low of 6.9% in the three months to February.

The upbeat data bolstered expectations that the Bank of England could raise interest rates as soon as the first quarter of 2015.

The euro was little changed against the dollar on Friday, with EUR/USD settling at 1.3810.

The euro’s gains were held in check after recent comments by European Central Bank officials flagged concerns over the impact of the strong currency on the inflation outlook.

On Thursday, ECB Executive Board member Yves Mersch said that if foreign exchange developments with an impact on inflation continue it would trigger a reaction by the central bank.

Elsewhere, the New Zealand dollar posted its largest weekly decline against the greenback since January, with NZD/USD ending the week down 1.24% to 0.8576, ahead of the Reserve Bank’s rate review on Thursday.

In the week ahead, market watchers will be focusing on U.S. data on housing and manufacturing activity, while manufacturing data from China will also be closely watched. The euro zone is to release data on private sector activity, while the U.K. is to produce a report on retail sales.

Ahead of the coming week, Investing.com has compiled a list of these and other significant events likely to affect the markets.

Monday, April 21

- Markets in Australia, New Zealand, the U.K. and the euro zone are to remain closed for Easter Monday. Meanwhile, Japan is to release data on the trade balance.

- Australia is to publish an index of leading economic indicators.

- Canada is to produce data on wholesale sales.

- The U.S. is to release private sector data on existing home sales.

- Australia is to publish data on consumer price inflation, which accounts for the majority of overall inflation.

- China is to release the preliminary estimate of the HSBC manufacturing index, a leading indicator of economic health.

- The euro zone is to release preliminary data on manufacturing and service sector activity, a leading indicator of economic health. Germany and France are also to release individual reports.

- The U.K. is to release data on public sector borrowing, while the BoE is to publish the minutes of its April meeting. The nation is also to publish private sector data on industrial order expectations.

- Canada is to produce official data on retail sales, the government measure of consumer spending, which accounts for the majority of overall economic activity.

- The U.S. is to publish reports on new home sales and manufacturing activity.

- The Reserve Bank of New Zealand is to announce its benchmark interest rate and publish its rate statement, which outlines economic conditions and the factors affecting the monetary policy decision.

- In the euro zone, Germany is to release the Ifo report on business climate.

- ECB President Mario Draghi is to speak at an event in Amsterdam; his comments will be closely watched.

- The U.S. is to publish data on durable goods orders and the weekly report on initial jobless claims.

- Markets in Australia and New Zealand will be closed for the Anzac Day holiday.

- Japan is to release data on consumer inflation.

- The U.K. is to produce data on retail sales.

- The U.S. is to round up the week with revised data on consumer sentiment.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.04.23 06:09

2014-04-23 01:30 GMT (or 03:30 MQ MT5 time) | [AUD - CPI]

- past data is 0.8%

- forecast data is 0.8%

- actual data is 0.6% according to the latest press release

if actual > forecast = good for currency (for AUD in our case)

==========

Australia CPI Rises 0.6% On Quarter In Q1

Consumer prices in Australia collected 0.6 percent on quarter in the first quarter of 2014, the Australian Bureau of Statistics said on Wednesday.

That was weaker than forecasts for 0.8 percent, which would have been unchanged from the previous three months.

The most significant price rises this quarter were for tobacco (+6.7 percent), automotive fuel (+4.1 percent), secondary education (+6.0 percent), tertiary education (+4.3 percent), medical and hospital services (+1.9 percent) and pharmaceutical products (+6.1 percent).

These rises were partially offset by falls in prices for furniture (-4.3 percent), maintenance and repair of motor vehicles (-3.3 percent), international holiday travel and accommodation (-2.4 percent) and domestic holiday travel and accommodation (-2.4 percent).

The tobacco price increase was caused by the federal excise tax rise that went into effect December 1.

Education prices have risen with the commencement of the new school year, the bureau said.

Rises for medical and hospital services and pharmaceutical products were a result of the cyclical reduction in the proportion of patients who qualify for subsidies under the Medicare Benefits Scheme and Pharmaceutical Benefits Scheme at the start of each calendar year.

On a yearly basis, consumer prices gained 2.9 percent - also below expectations for 3.2 percent after showing 2.6 percent in the three months prior.

MetaTrader Trading Platform Screenshots

MetaQuotes Software Corp., MetaTrader 5, Demo

AUDUSD M5 : 26 pips price movement by AUD - CPI news event

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

D1 correction within primary bullish was started on open bar together with triangle pattern: price is trying to break 0.9320 and 0.9261 support levels for the correction to be continuing.

H4 price is on reversal from bullish to bearish trying to go away from ranging zone (the cloud of Ichimoku indicator) having 2 strong support levels on the way.

W1 - market rally within primary bearish is going on.

If D1 price will break 0.9461 resistance level on close bar so the primary bullish will be continuing.If D1 price will break 0.9261 support level from above to below so the correction will be continuing with good possibility of price reversal.

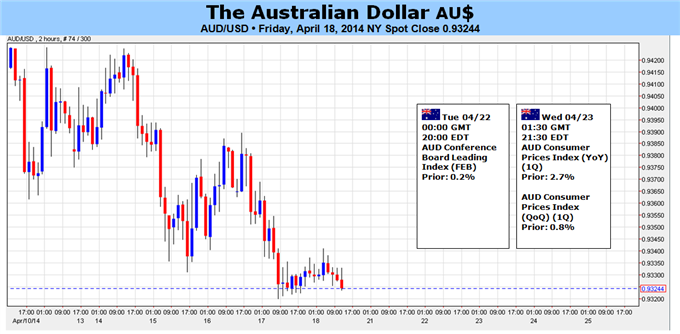

UPCOMING EVENTS (high/medium impacted news events which may be affected on AUDUSD price movement for this coming week)

2014-04-22 00:00 GMT (or 02:00 MQ MT5 time) | [AUD - CB Leading Index]

2014-04-22 14:00 GMT (or 16:00 MQ MT5 time) | [USD - Existing Home Sale]

2014-04-23 01:30 GMT (or 03:30 MQ MT5 time) | [AUD - CPI]

2014-04-23 01:45 GMT (or 03:45 MQ MT5 time) | [CNY - HSBC Manufacturing PMI]

2014-04-23 14:00 GMT (or 16:00 MQ MT5 time) | [USD - New Home Sales]

2014-04-24 12:30 GMT (or 14:30 MQ MT5 time) | [USD - Durable Goods Orders]

2014-04-25 13:55 GMT (or 15:55 MQ MT5 time) | [USD - UoM Consumer Sentiment]

Please note : some US (and CNY) high/medium impacted news events (incl speeches) are also affected on AUDUSD price movementSUMMARY : bullish

TREND : correction

Intraday Chart