Press review - page 293

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

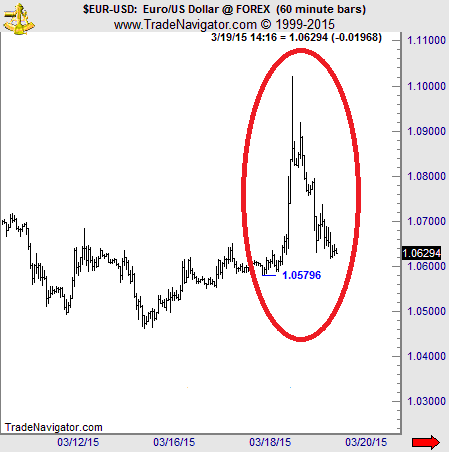

EURUSD surges after the FOMC decision

EURUSD flew approximately 400 pips higher after the Fed, despite dropping “patient”, lowered its interest rate trajectory and downgraded its view on economic growth and inflation. EURUSD moved above the near-term downtrend line taken from back the peak of the 26th of February to hit resistance at 1.1045 (R2), close to the 61.8% retracement level of the 26th of February – 13th of March decline. Subsequently the pair retreated to trade below 1.08000. Although an astonishing rally, it is far from a trend reversal signal.

if actual > forecast (or previous data) = good for currency (for CHF in our case)

[USD - Philly Fed Manufacturing Index] = Level of a diffusion index based on surveyed manufacturers in Philadelphia. It's a leading indicator of economic health - businesses react quickly to market conditions, and changes in their sentiment can be an early signal of future economic activity such as spending, hiring, and investment.

==========

Philly Fed Index Unexpectedly Shows Modest Drop In March

Manufacturing activity in the Philadelphia region has increased at a modest pace in the month of March, according to a report released by the Federal Reserve Bank of Philadelphia on Thursday, although the index of regional manufacturing activity unexpectedly showed a slight decrease.

The Philly Fed said its diffusion index of current activity edged down to 5.0 in March from 5.2 in February. While a positive reading indicates continued growth in manufacturing activity, economists had expected the index to climb to 7.0.

AUDIO - Goodbye "Patience" with Tillie Allison

Wednesday started off looking like a typical down day, nice gap down, nice trend down.. then the 5’3” sorceress of the markets, Janet Yellen decided to remove the word “Patience” from her comments and the markets went NUTS! Tillie and Merlin take a look at how this impacts the markets going forward, including bonds, equity markets, currencies and more.

Euro Correction Already Over? intraday volatility continues (based on dailyfx article)

The question on everybody’s mind after yesterday’s Fed inspired squeeze on USD long positons is whether that was it and the dollar can now resume higher or does the correction have more room to run? Judging by the action this morning it seems the market is scared of missing out on the next leg higher in the Greenbck as several pairs have already returned to pre-FOMC levels. Only time will tell whether this is the case, though it would be unusual to not see at least a period of minor consolidation first after such extreme volatility. In the euro, the 1.0550 area looks key with traction under this zone needed to confirm that a downside resumption is indeed underway. A move back over 1.0920 would warn that the correction has more room to run.

EURUSD: A Crazy 900-Pip "Roundtrip" (based on elliottwave article)

This week, we saw exactly what Jim had warned about: the craziest volatility in euro-dollar (EURUSD) we've seen in years. To be exact, last time EURUSD jumped 400-500 pips in one day was back in 2008. But the latest price action topped that: Not only did the euro rally almost 500 pips on Wednesday, but on Thursday it gave up almost all of those gains -- for an almost 900-pip "roundtrip":

In other words, bulls and bears got their clocks cleaned. All that's left now is confusion -- in both camps. While it may seem that the market "is out to get you" on days like these, the market doesn't have vendettas with anyone. It's simply doing what it should: taking money from the weak hands and handing it over to the strong. As Jim puts it, "The markets are doing what they are supposed to be doing: inflicting the most pain on the most number of people. The majority always gets caught on the wrong side at big reversals. Always.""At some point, everyone is in the same trade, like they are now in the euro short. Then it reaches the point of exhaustion: There is nobody left to sell the euro. Then somebody will start covering -- and before you know it, it's like Black Friday at your local Wal-Mart: Everyone is trying to squeeze through the same door at the same time. The coming EURUSD rally will be like that."

Jim Martens, Editor of Currency Pro Service

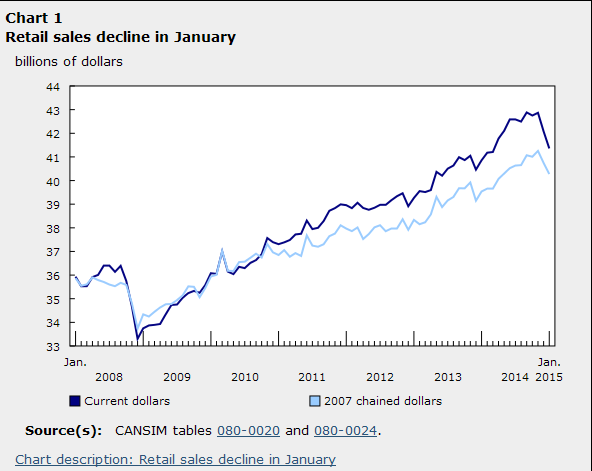

if actual > forecast (or previous data) = good for currency (for CAD in our case)

[CAD - Retail Sales] = Change in the total value of sales at the retail level. It's the primary gauge of consumer spending, which accounts for the majority of overall economic activity.

==========

Canada Retail Sales Decline 1.7% in JanuaryCanadian retail sales dropped at a steeper-than-anticipated pace in January, reaching the lowest level in 10 months, on a decline in receipts from gasonline stations.

Retail sales decreased 1.7% to a seasonally adjusted 41.36 billion Canadian dollars ($32.50 billion) in January, Statistics Canada said Friday, whereas market expectations were for a 0.8% decline, according to economists at Royal Bank of Canada.

Inflation data in the UK and the US, housing data from the US, German Ifo Business Climate, US Core Durable Goods Orders, Us Unemployment Claims and Stephen Poloz’ speech. These are the highlights of this week. Follow along as we explore the Forex market movers.

Last week, The Federal Reserve removed the word “patient” from its policy statement, increasing the odds for a rate hike in the coming months. However, the Fed also downgraded its economic growth and inflation projections. The Policy makers’ rate hike decision depends on mixed economic data, on one-hand strong job gains and robust consumer demand, while on the other hand, falling oil prices and a strong dollar, reducing exports and lowering inflation. Will the Fed raise rates on its June meeting?

The euro is going bananas (based on businessinsider article)

The euro is climbing against the dollar again on Friday, rising more than 1.7% to as high as $1.085 as of around 12:40 pm ET.

The euro spiked against the dollar when the Fed's latest decisions came out, as the US central bank looked less likely to hike rates in June (which would typically strengthen the dollar).

As it stands so far, the euro's depreciation bottomed out five days ago, below $1.05. A lot of people are still expecting parity by the end of 2015.

US Dollar Fundamentals (based on dailyfx article)

Fundamental Forecast for Dollar: Neutral

The Federal Open Market Committee (FOMC) meeting this past week certainly set off fireworks in the financial market. Yet, the outcome didn’t follow the simple path rate watchers would have expected. Now, with volatility further magnified; we find the Dollar wavering on its record-breaking, eight-month bull trend. Did the market overshoot on its speculative forecast for the Greenback before the central bank clarified its position – either pricing in a faster pace than was reasonable or perhaps pushing more premium than just the monetary policy differential would confer? Have the speculative ‘weak hands’ already been flushed from the system? And, will risk trends start to contribute to the curerncy’s fundamental picture in the near future?

Looking back at the Fed meet this past week, there weren’t many ‘surprises’. The headlines were focusing in particularly on whether the group would include or strike the term ‘patient’ in reference to their timing for normalizing monetary policy. It was popularly understood that the word was equivalent to a more than three-month time frame before the central bank would consider a rate hike. Having been removed, the ‘mid-2015’ (some say June) first rate hike is more probable.

Another meaningful change was the downgrade in growth, inflation and interest rate forecasts. In their updated forecasts, the Committee lowered a the 2015 GDP view to 2.3 – 2.7 percent (from 2.6 – 3.0), the 2015 inflation range to 0.6 – 0.8 percent (from 1.0 to 1.6) and December’s expected benchmark rate level to 0.625 percent (from 1.125). These are significant changes that could lower the ‘curve’ (or projected pace of tightening), but there was limited speculation of a swift pace to begin with. Furthermore, the moderation in this data does little to offset the communication effort by the Fed to acclimatize the market to an approaching hike. And yet, timing of the first hike assessed by Fed Funds futures was pushed even further back, to November.

The Dollar’s waffle after the policy update is likely a flush of an excessive market exposure. We’ve seen the currency far outpace other markets that are theoretically connected to rate forecasts (Treasury yields, Fed Fund futures, monetary markets). Having established such a remarkable and obvious trend, it is likely speculative interests that fell outside of the fundamental rational were drawn in. With the policy update, those focused on short-term momentum were easily shaken. The question is whether the excess has been worked from the market. Wednesday’s tumble was severe in both price and volume, but it didn’t even break the USDollar’s 8-month trend.

There is likely a large pocket of tactical traders who would quickly abandon the Dollar long view should it slip further or even stall for an extended period. Yet, despite the risk of a short-term long squeeze, the fundamental backdrop would still support the medium-term bullish lean for the currency. Whether the Fed realizes a hike in June or October, its hawkish view – much less its timing – is far more incisive than its counterparts.

What is perhaps even more remarkable from this past week, was the swell in risk appetite following the Fed decision. Even a delay to the start of a tightening regime still clarifies the central bank’s ability and intention to raise rates. That reverses a course of years of increasing accommodation to draw risk out of the market and encourage investing. Yet, to a market with an increasingly shorter time frame for positioning, it offers a quick opportunity. The trouble is, what will the mentality be after that speculative swing is over? For milestones to gauge policy and risk trends moving forward; watch event risk such as the CPI data, the laundry list of Fed Speeches (including Yellen’s address on Friday) as well as international topics – like Greece’s financial problems.

USDJPY Fundamentals (based on dailyfx article)

Fundamental Forecast for Japanese Yen: Neutral

In light of the market reaction to the Federal Open Market Committee’s (FOMC) March 18 meeting, the fundamental developments coming out of the world’s largest economy may continue to dictate the near-term price action for USD/JPY as Janet Yellen and Co. shows a greater willingness to retain the zero-interest rate policy (ZIRP) beyond mid-2015.

With that said, a slowdown in Japan’s Consumer Price Index (CPI) may have a limited impact on the dollar-yen especially as the Bank of Japan (BoJ) largely endorses a wait-and-see approach, while the U.S. data prints may foster increased volatility in the exchange rate as market participants continue to speculate on the Fed’s first rate hike. An uptick in the core U.S. CPI paired with an upward revision in the 4Q Gross Domestic Product (GDP) report may heighten the appeal of the greenback, but the disinflationary environment may become a growing concern for the central bank as the core Personal Consumption Expenditure (PCE), the Fed’s preferred gauge for price growth, is expected to slow to 1.1% from 1.4% in the three-months through September.

The fresh forecasts coming out of the central bank suggests that FOMC will further delay its normalization cycle as the committee pushes out its interest rate dot-plot, and the Fed may sound more dovish heading into the second-half of the year amid the uncertainties surrounding the global economy. In turn, the dollar remains at risk of facing additional headwinds over the coming months, and the near-term pullback may ultimately turn into a larger correction should the U.S. data prints fail to meet market expectations.

As a result, the near-term topping process around the 122.00 handle may pave the way for a further decline in USD/JPY, and the pair may continue to give back the advance from earlier this year as the Relative Strength Index (RSI) fails to retain the bullish trend carried over from back in January. The downside break in the oscillator favors the approach to ‘sell bounces’ in the dollar-yen, but the pair may face choppy price action going into the key event risks as market participants continue to digest the latest developments coming out of the U.S.