AxelQuant | Sistematik Trade ve Risk Yönetimi

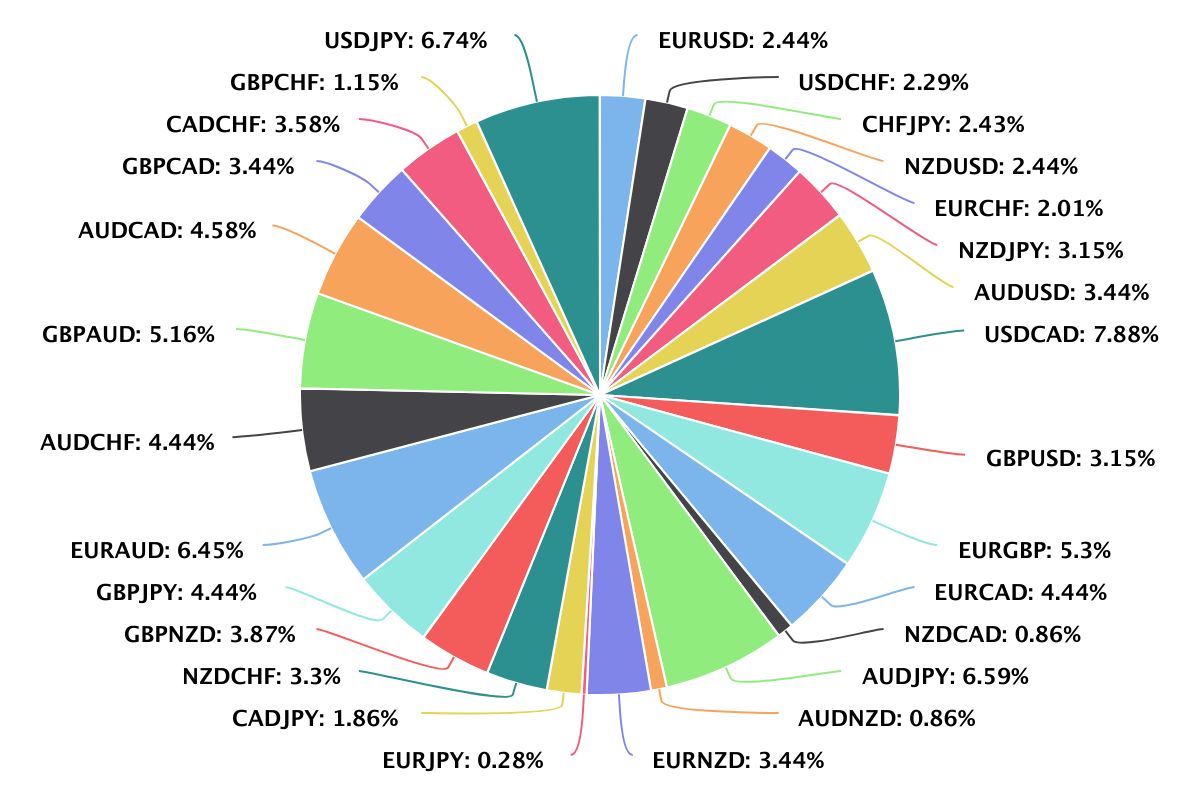

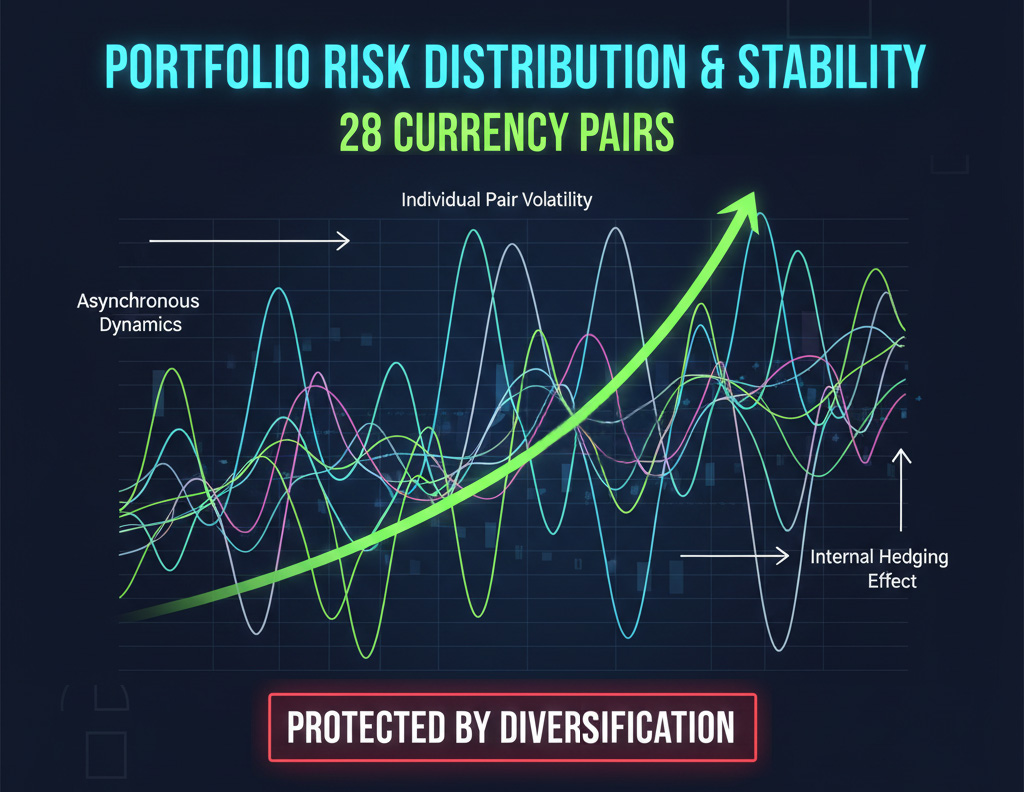

Hoş geldiniz. Yapısal istikrar ve uzun vadeli sermaye büyümesine odaklanan işlem stratejileri geliştirme konusunda uzmanım. Ana stratejim olan Bowstring's Song, 28 döviz çiftinden oluşan çeşitlendirilmiş bir portföyde işlem yapan hibrit, trende uyumlu bir modeldir.

Resmi Bağlantılar ve Doğrulama:

📊 Doğrulanmış Denetim: Myfxbook üzerinden gerçek zamanlı tam istatistikler

myfxbook.com/members/AxelQuant/bowstrings-song/11859074

🔵 RoboForex (CopyFX): Kâr payı bazlı ana sinyal

roboforex.com/copy-trading/rating/aaai/74170190

🟢 SignalStart: Diğer aracı kurumlar için alternatif bağlantı

axelquant.signalstart.com/analysis/bowstrings-song/285067

🛰 Telegram Kanalı: Strateji günlüğü, mantık analizleri ve güncellemeler

t.me/BowstringsSong

Strateji Detayları:

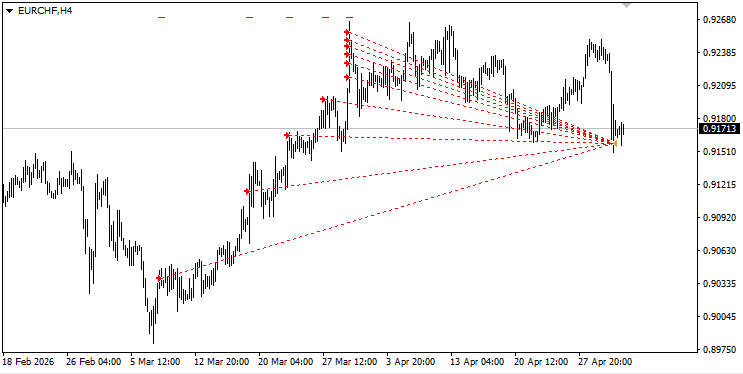

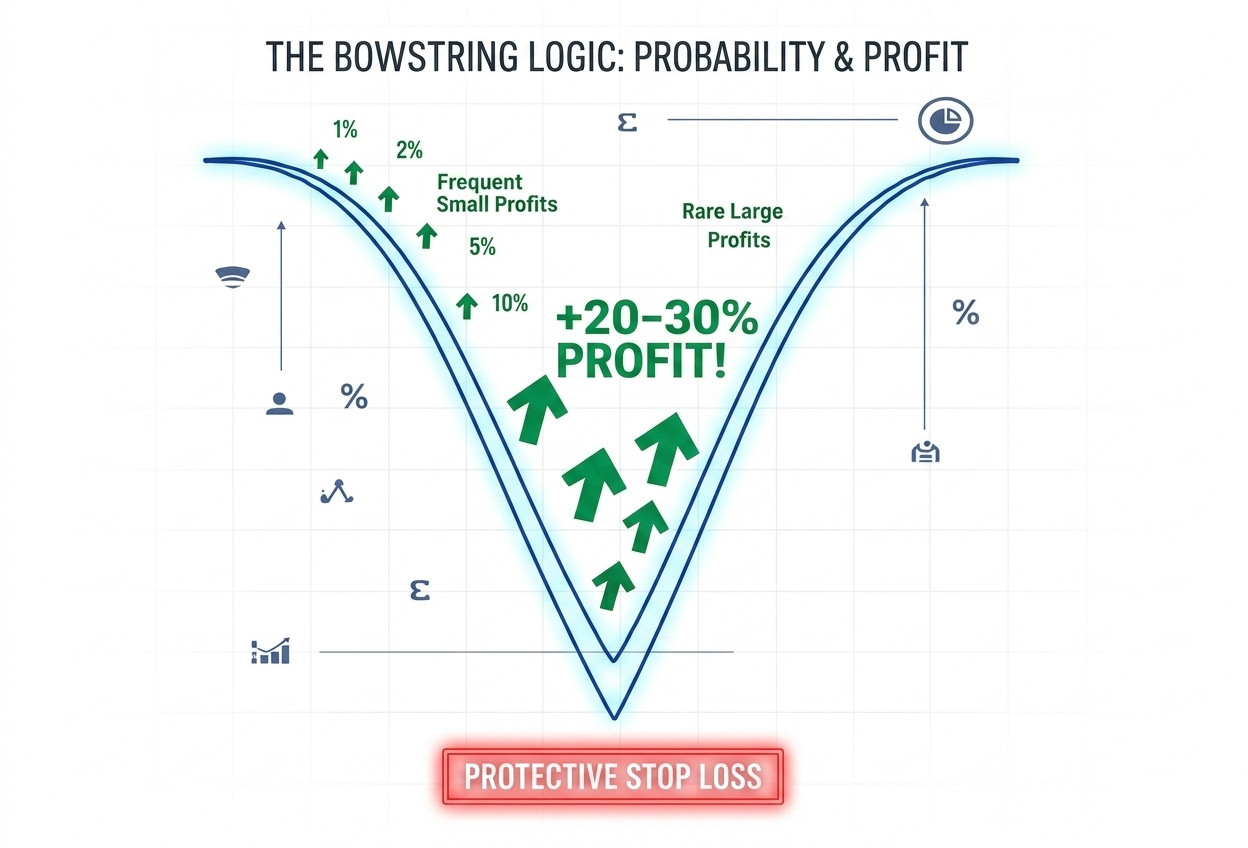

Mantık, hakim trend içindeki geri çekilmelerde (pullback) işleme girmeye ve çift çıkış mekanizmasına (trendin devamı veya ortalamaya dönüş) dayanmaktadır. Tam şeffaflık ilkesini benimsiyorum: Her pozisyon için zorunlu Hard Stop-Loss ve profesyonel denetim sağlıyorum.

📖 Mantık, grid (ızgara) mekanizması ve risk yönetimi hakkındaki detaylı analiz için lütfen profil akışımdaki ilk 5 gönderiyi okuyun.

Çalışmalarıma gösterdiğiniz ilgi için teşekkür ederim.

Hoş geldiniz. Yapısal istikrar ve uzun vadeli sermaye büyümesine odaklanan işlem stratejileri geliştirme konusunda uzmanım. Ana stratejim olan Bowstring's Song, 28 döviz çiftinden oluşan çeşitlendirilmiş bir portföyde işlem yapan hibrit, trende uyumlu bir modeldir.

Resmi Bağlantılar ve Doğrulama:

📊 Doğrulanmış Denetim: Myfxbook üzerinden gerçek zamanlı tam istatistikler

myfxbook.com/members/AxelQuant/bowstrings-song/11859074

🔵 RoboForex (CopyFX): Kâr payı bazlı ana sinyal

roboforex.com/copy-trading/rating/aaai/74170190

🟢 SignalStart: Diğer aracı kurumlar için alternatif bağlantı

axelquant.signalstart.com/analysis/bowstrings-song/285067

🛰 Telegram Kanalı: Strateji günlüğü, mantık analizleri ve güncellemeler

t.me/BowstringsSong

Strateji Detayları:

Mantık, hakim trend içindeki geri çekilmelerde (pullback) işleme girmeye ve çift çıkış mekanizmasına (trendin devamı veya ortalamaya dönüş) dayanmaktadır. Tam şeffaflık ilkesini benimsiyorum: Her pozisyon için zorunlu Hard Stop-Loss ve profesyonel denetim sağlıyorum.

📖 Mantık, grid (ızgara) mekanizması ve risk yönetimi hakkındaki detaylı analiz için lütfen profil akışımdaki ilk 5 gönderiyi okuyun.

Çalışmalarıma gösterdiğiniz ilgi için teşekkür ederim.