AxelQuant | 系统化交易与风险管理

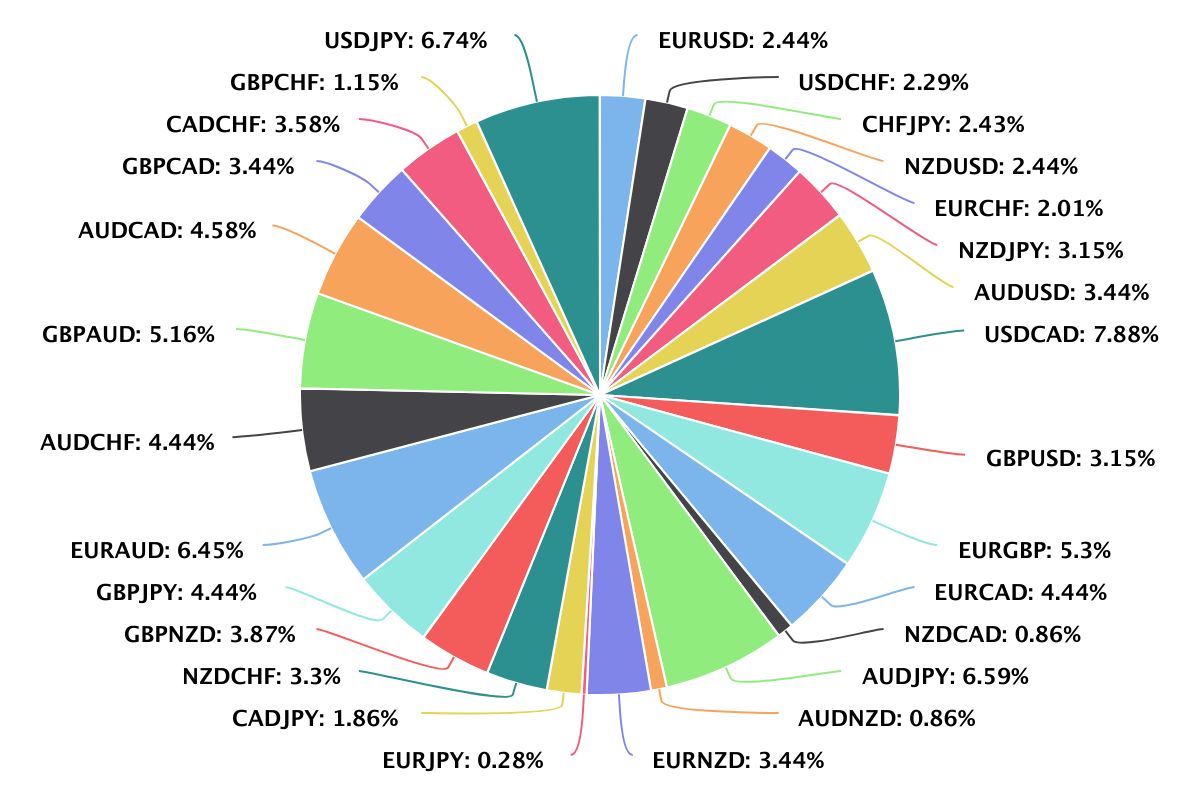

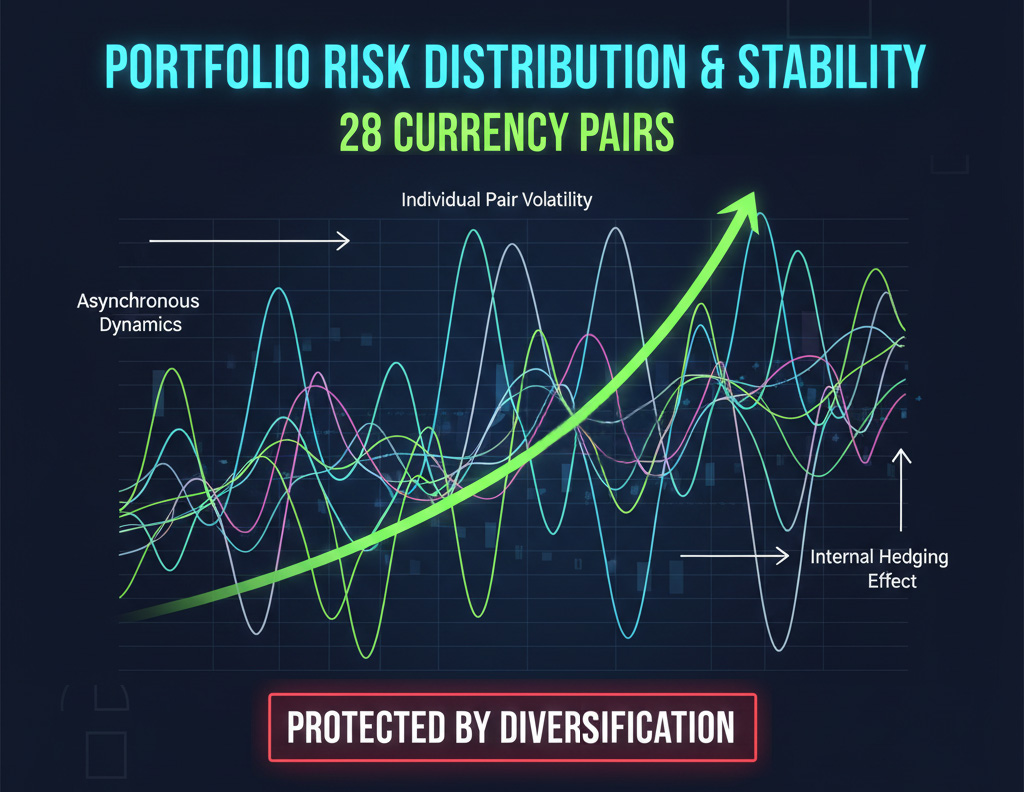

欢迎。我专注于开发旨在实现结构化稳定和资本长期增长的交易策略。我的旗舰策略 Bowstring's Song 是一种混合趋势适应模型,涵盖 28 种货币对的多元化投资组合。

官方链接与审计:

📊 实盘审计: 在 Myfxbook 上查看完整实时统计数据

myfxbook.com/members/AxelQuant/bowstrings-song/11859074

🔵 RoboForex (CopyFX): 基础信号,按盈利分红

roboforex.com/copy-trading/rating/aaai/74170190

🟢 SignalStart: 适用于其他经纪商的备选连接

axelquant.signalstart.com/analysis/bowstrings-song/285067

🛰 Telegram 频道: 策略日志、逻辑分析与动态更新

t.me/BowstringsSong

策略详情:

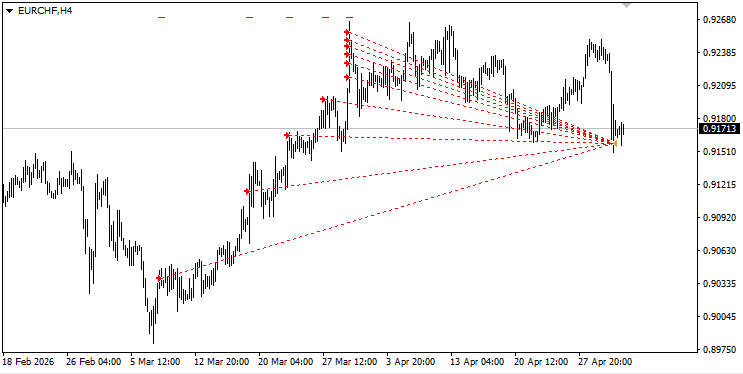

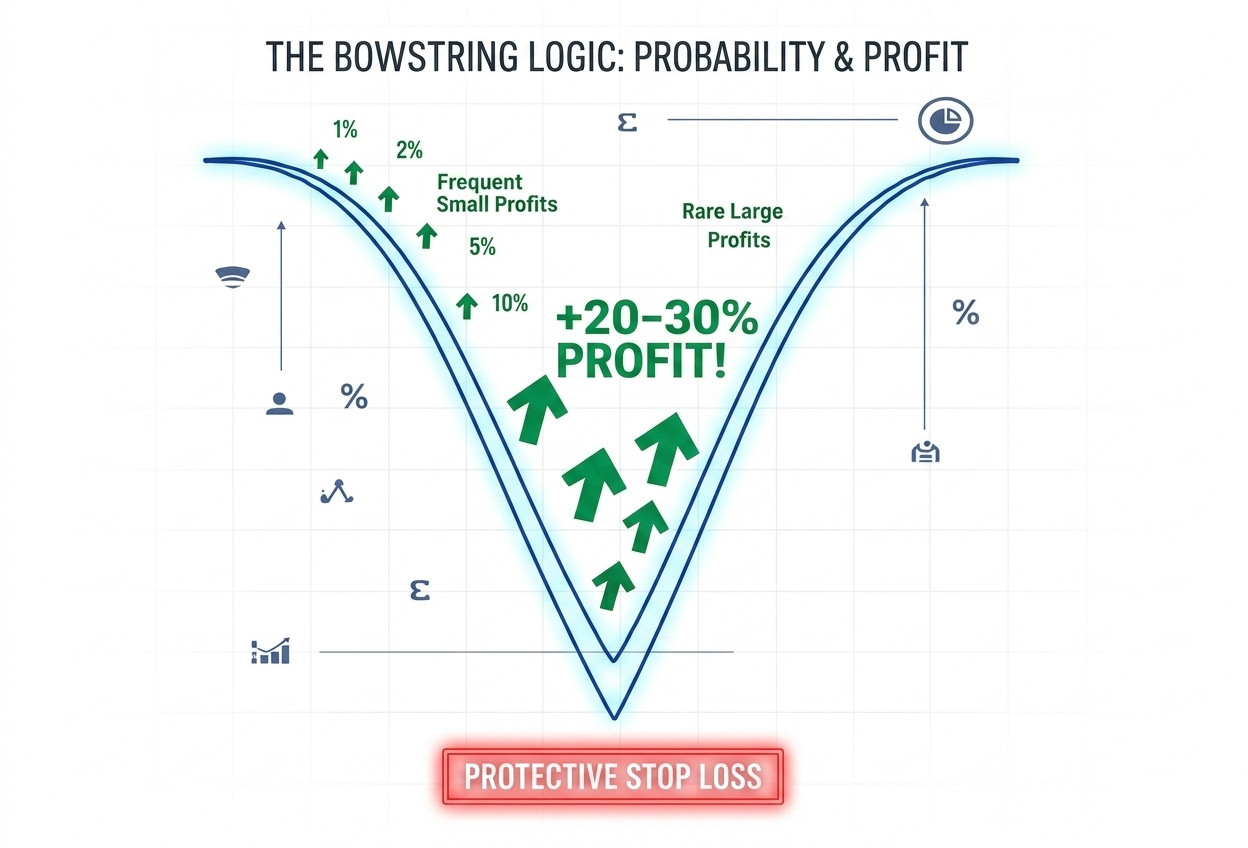

该逻辑基于顺势回调入场,并具备双重退出机制(趋势延续或均值回归)。我坚持透明化原则:每笔交易均设有强制止损 (Hard Stop-Loss),并结合专业的人工监控。

📖 有关逻辑、网格机制和风险管理的完整解析,请阅读下方个人主页动态的前 5 篇文章。

感谢您对我的工作感兴趣。

欢迎。我专注于开发旨在实现结构化稳定和资本长期增长的交易策略。我的旗舰策略 Bowstring's Song 是一种混合趋势适应模型,涵盖 28 种货币对的多元化投资组合。

官方链接与审计:

📊 实盘审计: 在 Myfxbook 上查看完整实时统计数据

myfxbook.com/members/AxelQuant/bowstrings-song/11859074

🔵 RoboForex (CopyFX): 基础信号,按盈利分红

roboforex.com/copy-trading/rating/aaai/74170190

🟢 SignalStart: 适用于其他经纪商的备选连接

axelquant.signalstart.com/analysis/bowstrings-song/285067

🛰 Telegram 频道: 策略日志、逻辑分析与动态更新

t.me/BowstringsSong

策略详情:

该逻辑基于顺势回调入场,并具备双重退出机制(趋势延续或均值回归)。我坚持透明化原则:每笔交易均设有强制止损 (Hard Stop-Loss),并结合专业的人工监控。

📖 有关逻辑、网格机制和风险管理的完整解析,请阅读下方个人主页动态的前 5 篇文章。

感谢您对我的工作感兴趣。