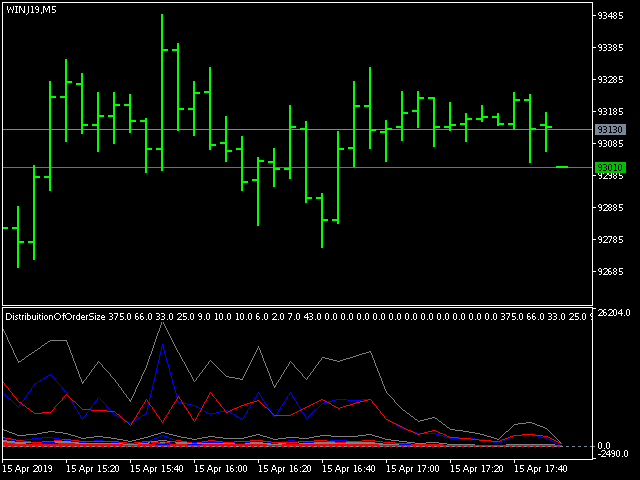

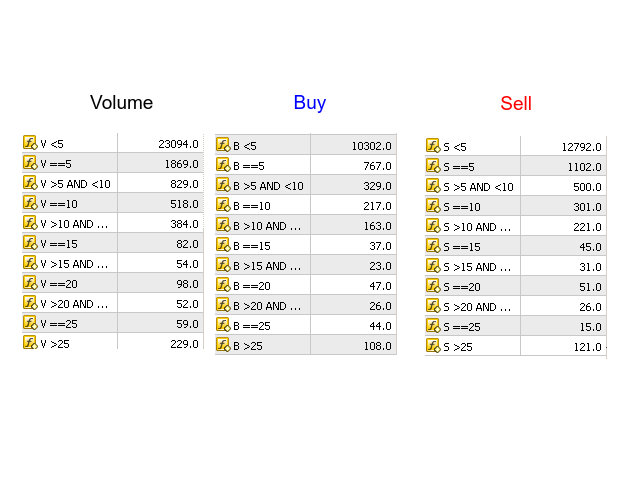

Distribuition of Orders Volume

- Индикаторы

- Roberto Spadim

- Версия: 1.1

- Обновлено: 16 апреля 2019

- Активации: 5

Easley et al. study the frequency of trades per trade size, and find that

trades with round sizes are abnormally frequent. For example, the frequency rates

quickly decay as a function of trade size, with the exception of round trade sizes

{5, 10, 20, 25, 50, 100, 200,…}.

These authors attribute this phenomenon to socalled “mouse” or “GUI” traders, that is, human traders who send orders by clicking buttons on a GUI (Graphical User Interface).

In the case of the E-mini S&P 500, for example, size 10 is 2.9 times more frequent than size 9; size 50 is 10.9 times more likely than size 49; size 100 is 16.8 times more frequent than size 99; size 200 is 27.2 times more likely than size 199; size 250 is 32.5 times more frequent than size 249; size 500 is 57.1 times more frequent than size 499.

Such patterns are not typical of “silicon traders,” who usually are programmed to randomize trades to disguise their footprint in markets.

---

These authors attribute this phenomenon to socalled “mouse” or “GUI” traders, that is, human traders who send orders by clicking buttons on a GUI (Graphical User Interface).

In the case of the E-mini S&P 500, for example, size 10 is 2.9 times more frequent than size 9; size 50 is 10.9 times more likely than size 49; size 100 is 16.8 times more frequent than size 99; size 200 is 27.2 times more likely than size 199; size 250 is 32.5 times more frequent than size 249; size 500 is 57.1 times more frequent than size 499.

Such patterns are not typical of “silicon traders,” who usually are programmed to randomize trades to disguise their footprint in markets.

---

This indicator is based on Advances in Financial Machine Learning 2018 - Marcos Lopez de Prado book, Page 293.