|

12+ 년도

경험

|

6

제품

|

292

데몬 버전

|

|

3

작업

|

0

거래 신호

|

0

구독자

|

Quant Researcher

에

.

Trading is my full-time job. I've been in the market since 2008, researching the forex, stock, commodity, and cryptocurrency markets. I study patterns and the reasons why they emerge and disappear. I'm developing my own pricing theory that describes and predicts the emergence of certain patterns. I develop unique indicators based on my research, build complex trading algorithms, and use them in my work.

Maxim Romanov

8

ron33

2021.06.18

I read all your self-adaptation articles are great but in chapter three I did not find the 50% V3 robot, I found the block indicators but in EA code it is not anywhere in the compressible . Although this is an excellent guide on how it works. Does the robot code exist?

Maxim Romanov

2021.06.18

The code exists, but it is not distributed free of charge. If there is a strong desire, then I consider proposals

Maxim Romanov

· 3

Maxim Romanov

2018.11.16

Aleksey Vyazmikin не оптимизируется вообще ничего. В роботе есть параметры, отвечающие за работу самого алгоритма, их очень много, чуть больше 2000. Но устанавливаются они вручную без оптимизации. Да и оптимизация просто невозможна с такой скорость работы (2 месяц теста проходят за сутки). Дальше на каждом инструменте, автоматически определяется тайм фрейм для торговли и период для анализа тоже автоматически, эти параметры корректируются по мере движения цены. Если открыта позиция, то определяется точка профита и лосса автоматически и корректируется от текущего состояния рынка. У торговой стратегии нет как таковых настроек, у нее есть закономерность, которую она должна отрабатывать, а все параметры торговли корректируются под эту закономерность в реальном времени.

Maxim Romanov

· 8

전체 댓글 표시 (9)

Maxim Romanov

2020.08.02

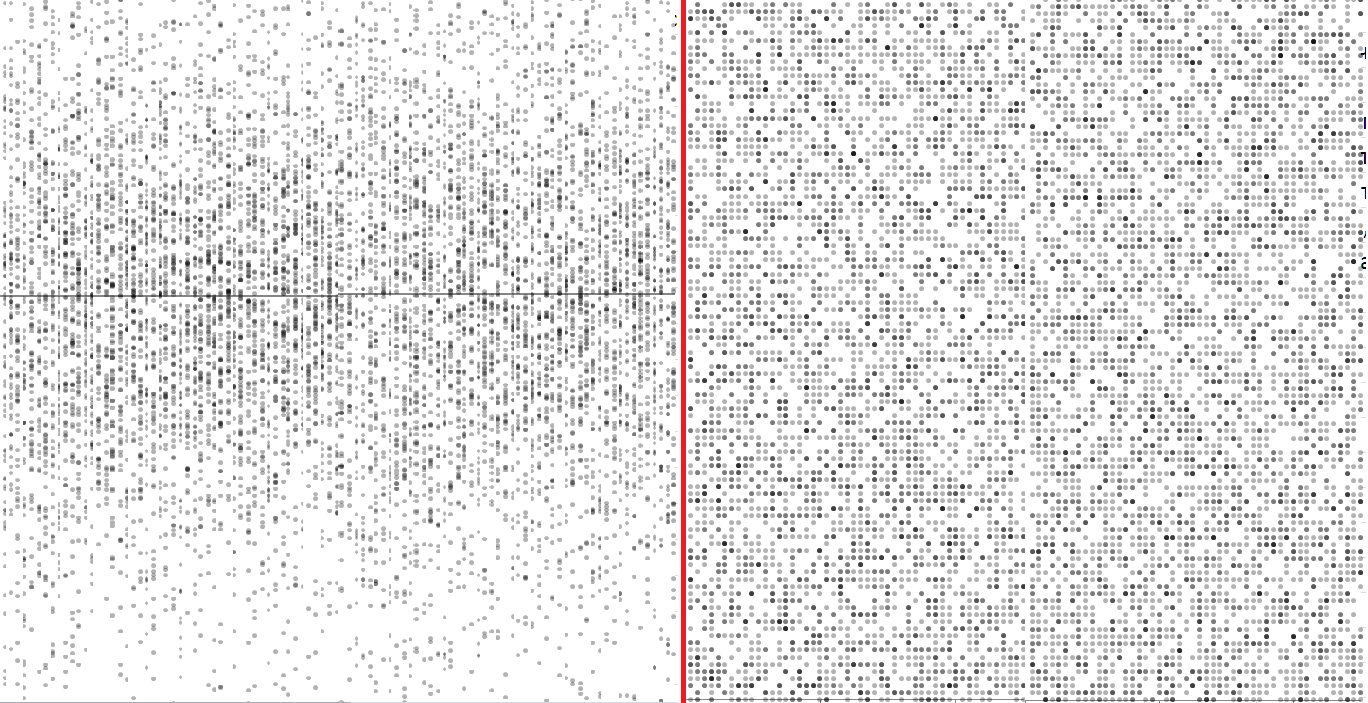

Это был размер свечей. По оси Y размер свечей в пунктах от -n до n. Одна точка это одна свеча. График состоит из столбцов, набранных по К точек. Например в одном столбце делаем 1000 измерений размера свечей и ставим полупрозрачные точки. Как только 1000 измерений сделано, переходим к следующему столбцу. и так заполняем все пространство. Тут есть одна особенность. Я делал это достаточно давно и не учел один нюанс: Справа рисунок построен для равномерного распределения, а слева для рынка. Но рынок ближе к нормальному распределению, из-за особенностей формирования цен! Поэтому правильнее было бы сравнивать рыночные данные с ГСЧ, формирующим нормальное распределение.

Enrique Enguix

2020.11.20

I think you are a genius, although many times I don't understand what you're talking about. Every time I read something of yours, I have to think about your words for hours. You are a humility cure for many of the people who are in this market

Arch

2021.12.16

Потому,что на графике образуются "контрольные точки" вероятность их закрытия 95% (но по логике 99)и только время определяет , когда эти точки будут закрыты.Скопление точек ближе к середине это и есть точки с наименьшем временем, ближе к краям те самые 5%.Я больше,чем уверен,если каждый пипс пронумеровать и сделать следующий тест вперёд-то При сравнении те самые 5% окажутся ближе к середине,а по краям будут только новые пипсы с другими цифрами.