WalkForwardOptimizer MT5

- Libraries

-

Stanislav Korotky

Trading is just my hobby. I'm working in IT industry. So developement of experts, indicators, and script is not a problem at all to me. Wide range of technologies are used: MQL4, MQL5, system and applied programming, web-services, neural networks and more.

Trading is just my hobby. I'm working in IT industry. So developement of experts, indicators, and script is not a problem at all to me. Wide range of technologies are used: MQL4, MQL5, system and applied programming, web-services, neural networks and more.

New: - Version: 1.17

- Updated: 9 April 2025

- Activations: 5

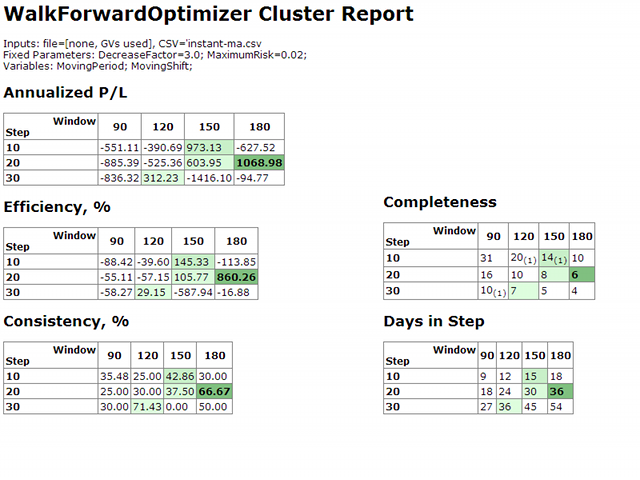

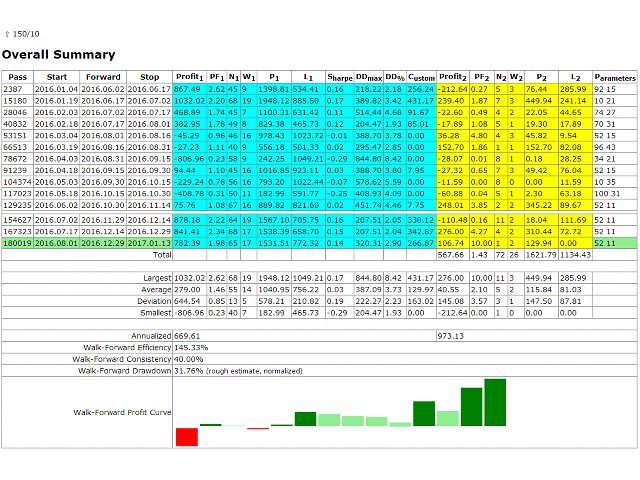

WalkForwardOptimizer library allows you to perform rolling and cluster walk-forward optimization of expert advisers (EA) in MetaTrader 5.

To use the library include its header file WalkForwardOptimizer.mqh into your EA source code, add call provided functions as appropriate.

Once the library is embedded into EA, you may start optimization according to the procedure described in the User guide. When it's finished, intermediate results are saved into a CSV file and some special global variables. Also a comprehensible report is generated as HTML page.

This is a library. It requires a user to have some developer skills. If you do not have source codes of your EA (if it's a 3-rd party commercial EA) or do not understand the sources codes (if it's made for you by custom developer), please, contact the author/developer of the EA (source codes) to solve all problems. If he thinks there is a bug in the library, then let the author/developer contact me directly. I need technical details (which are hard to receive from non-developers) to provide proper support.

The text is shortened due to size limit - download full file from Comments.

WalkForwardOptimizer.mqh Header File

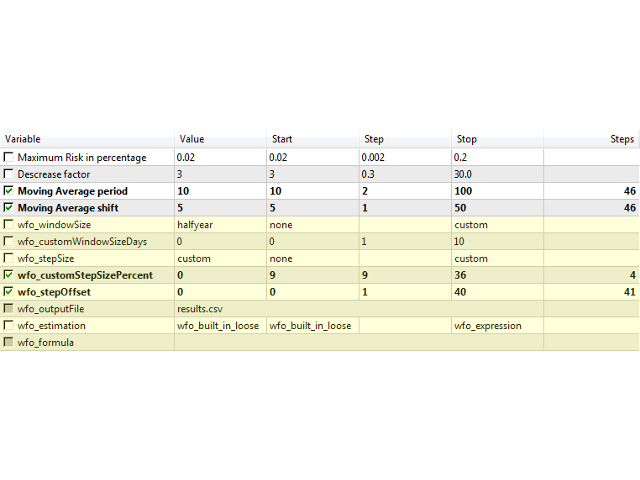

#define DAYS_PER_WEEK 7 #define DAYS_PER_MONTH 30 #define DAYS_PER_QUARTER (DAYS_PER_MONTH*3) #define DAYS_PER_HALF (DAYS_PER_MONTH*6) #define DAYS_PER_YEAR (DAYS_PER_MONTH*12) #define SEC_PER_DAY (60*60*24) #define SEC_PER_WEEK (SEC_PER_DAY*DAYS_PER_WEEK) #define SEC_PER_MONTH (SEC_PER_DAY*DAYS_PER_MONTH) #define SEC_PER_QUARTER (SEC_PER_MONTH*3) #define SEC_PER_HALF (SEC_PER_MONTH*6) #define SEC_PER_YEAR (SEC_PER_MONTH*12) #define CUSTOM_DAYS -1 enum WFO_TIME_PERIOD {none = 0, year = DAYS_PER_YEAR, halfyear = DAYS_PER_HALF, quarter = DAYS_PER_QUARTER, month = DAYS_PER_MONTH, week = DAYS_PER_WEEK, day = 1, custom = CUSTOM_DAYS}; enum WFO_ESTIMATION_METHOD {wfo_built_in_loose, wfo_built_in_strict, wfo_profit, wfo_sharpe, wfo_pf, wfo_drawdown, wfo_profit_by_drawdown, wfo_profit_trades_by_drawdown, wfo_average, wfo_expression}; #import "WalkForwardOptimizer MT5.ex5" // !after install must be copied into MQL5/Libraries void wfo_setEstimationMethod(WFO_ESTIMATION_METHOD estimation, string formula); void wfo_setPFmax(double max); void wfo_setCloseTradesOnSeparationLine(bool b); void wfo_OnTesterPass(); int wfo_OnInit(WFO_TIME_PERIOD optimizeOn, WFO_TIME_PERIOD optimizeStep, int optimizeStepOffset, int optimizeCustomW, int optimizeCustomS); int wfo_OnTick(); double wfo_OnTester(); void wfo_OnTesterInit(string optimizeLog); void wfo_OnTesterDeinit(); #import input WFO_TIME_PERIOD wfo_windowSize = year; input int wfo_customWindowSizeDays = 0; input WFO_TIME_PERIOD wfo_stepSize = quarter; input int wfo_customStepSizePercent = 0; input int wfo_stepOffset = 0; input string wfo_outputFile = ""; input WFO_ESTIMATION_METHOD wfo_estimation = wfo_built_in_loose; input string wfo_formula = "";

Example of Usage

#include <WalkForwardOptimizer.mqh> ... int OnInit(void) { // your actual code goes here ... wfo_setEstimationMethod(wfo_estimation, wfo_formula); // wfo_built_in_loose by default wfo_setPFmax(100); // DBL_MAX by default // wfo_setCloseTradesOnSeparationLine(true); // false by default // this is the only required call in OnInit, all parameters come from the header int r = wfo_OnInit(wfo_windowSize, wfo_stepSize, wfo_stepOffset, wfo_customWindowSizeDays, wfo_customStepSizePercent); return(r); } void OnTesterInit() { wfo_OnTesterInit(wfo_outputFile); // required } void OnTesterDeinit() { wfo_OnTesterDeinit(); // required } void OnTesterPass() { wfo_OnTesterPass(); // required } double OnTester() { return wfo_OnTester(); // required } void OnTick(void) { int wfo = wfo_OnTick(); if(wfo == -1) { // can do some non-trading stuff, such as gathering bar or ticks statistics return; } else if(wfo == +1) { // can do some non-trading stuff return; } // your actual code goes here ... }

Excellent library! its very simple to setup and not too complex, just make sure to locate the ex5 library correctly (hidden in the market directory, this left me confused for a bit lmao) all in all. 5/5 would use it constantly