Calculate Stochastic for custom timeframes

double iStochMain() { double sumLow=0.0,sumHigh=0.0; for(int u=0;u<slowing;u++) { sumLow+=(iClose(Symbol(),5,u+1)-iLow(Symbol(),5,iLowest(Symbol(),5,MODE_LOW,perck,u+1))); sumHigh+=(iHigh(Symbol(),5,iHighest(Symbol(),5,MODE_HIGH,perck,u+1))-iLow(Symbol(),5,iLowest(Symbol(),5,MODE_LOW,perck,u+1))); } return(sumLow/sumHigh*100); }

Thank you so much! Appreciate the help of a fellow Saffer!

Ok so now I have the correct values for the %K line:

double SK1(int tf) { int starts=iTime(Symbol(),PERIOD_H4,0); int barstart=iBarShift(Symbol(),1,iTime(Symbol(),PERIOD_H4,0)); double rem=barstart%tf; int theshift=tf-rem-1; double sumLow=0.0,sumHigh=0.0; ArrayResize(K1,percd+1); int t; for(int i=0;i<(percd+1)*tf;i+=tf) { for(int u=0;u<slowing*tf;u+=tf) { sumLow+=(iClose(Symbol(),1,(u+tf-theshift)+i))-iLow(Symbol(),1,iLowest(Symbol(),1,MODE_LOW,perck*tf,(u+tf-theshift)+i)); sumHigh+=(iHigh(Symbol(),1,iHighest(Symbol(),1,MODE_HIGH,perck*tf,(u+tf-theshift)+i))-iLow(Symbol(),1,iLowest(Symbol(),1,MODE_LOW,perck*tf,(u+tf-theshift)+i))); } K1[t]=sumLow/sumHigh*100; sumLow=0.0; sumHigh=0.0; t++; } return(K1[0]); }

Adjust for a custom time frame value

How I want to go about calculating th %D - using an EMA.

From what I understand, the iMAOnArray() will only work for indicator buffers, for which this is not.

An SMA for %D would be simply:

double theema; theema=(K1[0]+K1[1]+K1[2]+K1[3]+K1[4])/5;

How would I go about calculating %D using EMA?

Regards

Richard

iMAOnArray() should work or you can use the function from MovingAverages.mqh header file.

MMm Thanks Ernst, but does not seem to be producing the correct value?

{kind=link}

MMm Thanks Ernst, but does not seem to be producing the correct value

These array sizes get the correct values.

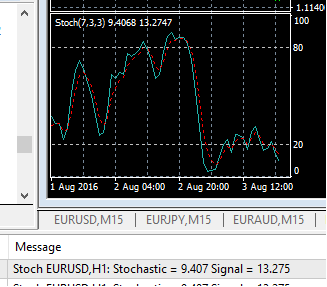

#include <MovingAverages.mqh> double Stoch[2]; //+------------------------------------------------------------------+ //| Custom indicator iteration function | //+------------------------------------------------------------------+ void OnTick() { //--- iStochastic(_Symbol,_Period,7,3,3,Stoch); printf("Stochastic = %.3f Signal = %.3f",Stoch[0],Stoch[1]); //--- return value of prev_calculated for next call return; } //+------------------------------------------------------------------+ int iStochastic(string symbol,int timeframe,int k_period,int d_period,int slowing,double &stoch[]) { double Kbuffer[],Dbuffer[]; ArrayResize(Kbuffer,k_period*3); ArrayResize(Dbuffer,k_period*3); //--- for(int i=0;i<k_period*3;i++) { double sumLow=0.0,sumHigh=0.0; for(int u=i;u<i+slowing;u++) { sumLow+=(iClose(symbol,timeframe,u)-iLow(symbol,timeframe,iLowest(Symbol(),timeframe,MODE_LOW,k_period,u))); sumHigh+=(iHigh(symbol,timeframe,iHighest(symbol,timeframe,MODE_HIGH,k_period,u))-iLow(symbol,timeframe,iLowest(symbol,timeframe,MODE_LOW,k_period,u))); } Kbuffer[i]=sumLow/sumHigh*100; } //--- for(int i=k_period*3-2;i>=0;i--) Dbuffer[i]=ExponentialMA(i,d_period,Dbuffer[i+1],Kbuffer); //--- stoch[0]=Kbuffer[0]; stoch[1]=Dbuffer[0]; //--- return(0); } //+------------------------------------------------------------------+

These array sizes get the correct values.

Awesome thanks Ernst! Will give it a try.

Thanks for the help man!

These array sizes get the correct values.

You rock Ernst! Works like a charm.

Thanks Buddy!

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Hi there,

I am trying to code an indicator to show Stochastic %K and %D for custom timeframes ( 2, 17, 26 etc).

For the first step, I am just trying to recode the normal stochastic, to give me the %K for the most recent closed bar. for this example I am using the M5 timeframe. My code is as follows:

Where "slowing" is the slowing period for the stochastic, and perck is the %K period.

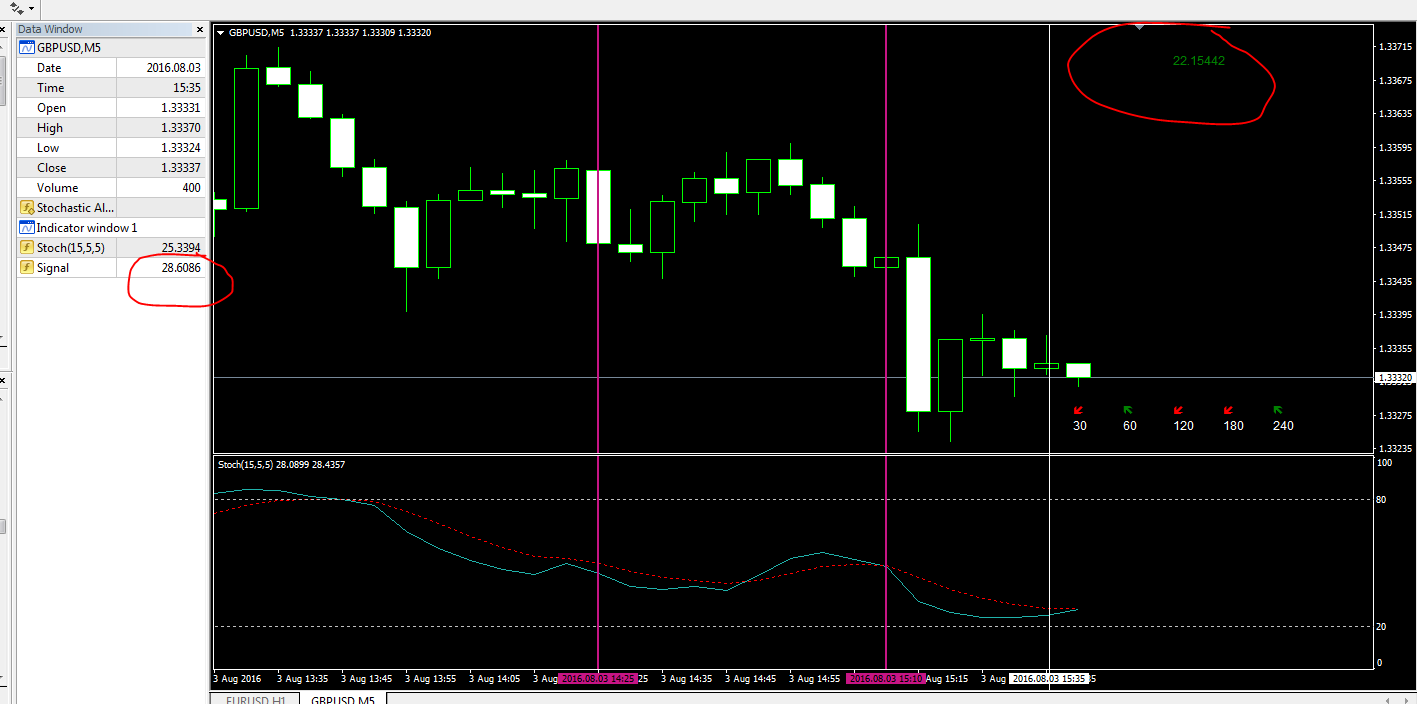

The value is close to the standard MT4 stochastic indi, but out but a couple of decimal places.

Any idea where I am going wrong?

Thanks

Richard