GOLD Technical Analysis 2015, 16.08 - 23.08: bearish ranging within key levels

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.08.17 19:22

5 reasons to believe gold prices could recover to $1,200 at year-end - HSBC (based on cnbc article)

The bank made a forecast for the price of gold at year-end and estimated that it will be increase as much as 10 percent higher than current levels. The bank set out five reasons in a report on Friday for the experts to believe gold prices could recover to $1,200 per ounce at the year-end.

1. Fed tightening is already priced into gold

"With

a shift in the Federal Reserve's policy

having been anticipated in the financial markets since as early as 2013,

some of the declines based on a rate rise have already occurred." Thus,

the reaction of the gold may not be negative one in any case.

2. Actual Fed hikes could see gold prices rise

"This pattern has important ramifications for gold. History shows

that gold prices…generally rise, though sometimes with a lag, after the

first rate hike."

3. There's scope for a short-covering rally

Short positions on the Comex touched the peak on July 7 while long

positions are at their highest since December 2009.

4. Low prices will, ultimately, spur demand

"In important gold consuming nations, such as China, India,

Indonesia, and Vietnam, as well as other EMs, consumers may have fewer

tools at their disposal with which to protect savings and household

wealth against rising prices or low or negative real interest rates."

5. Central bank buying will remain supportive

"The PBoC is an important central bank with

significant influence. The mere fact that they have accumulated gold may

lead other EM central banks to examine purchasing bullion. Also many central banks hold quite low levels of

gold reserves in relation to their forex holdings, leaving room for

further accumulation."

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.08.18 10:21

FOMC Meeting Minutes expectations by Barclays and September Fed hike (based on efxnews article)

Barclays made a forecast for high impacted fundamental news events which will be on Wednesday at 19:00 GMT. The bank is telling that Federal Open Market Committee is already made a decision concerning a September Fed hike. Besides, Barclays is expecting the USD dollar to gain strength because "fears around China and weak commodity prices should keep pushing investors out of risky assets":

- "We do not expect a material change and we anticipate that the document will echo the latest comments from different FOMC members. We think they will want to keep options open and will probably signal the data dependency of their decisions ahead. We believe that the FOMC has already made up their mind about their next move, absent any market disruptive events in the months ahead. Our base case remains a September Fed hike."

- "Furthermore, we argued that the actual path of the normalization process will be more important for FX markets. The pace at which the Fed could tighten monetary conditions should depend heavily on price measures."

-

"We expect the USD to be supported in the next weeks mainly due to external factors.

Fears around China and weak commodity prices should keep pushing

investors out of risky assets, benefiting the USD under different

scenarios."

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.08.18 20:21

BNP Paribas: 2 Things To Look For At FOMC Minutes (based on efxnews article)

-

"The key message will probably be that ‘lift-off’ is approaching and

that we moved a step closer in July. A majority of FOMC participants

probably still expected ‘lift-off’ to be appropriate sometime this year.

As markets are already pricing this in, the minutes should present few

surprises."

-

"Two things to look for: (1) what “some” further labor-market

improvement means and (2) why there was no progress report on being

“reasonably confident” in the inflation outlook."

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.08.19 06:54

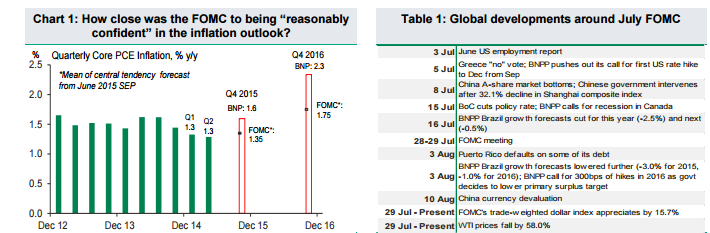

The Royal Bank of Scotland - FOMC Meeting Minutes and Consumer Price Index (CPI) (based on efxnews article)Chair Yellen is not speaking at the Jackson Hole Symposium this year:

-

"While our economist Michelle Girard thinks the Fed may

disappoint on giving a “firm” signal, which would fit with their data

dependent outlook, she sees a risk that the FOMC minutes begin to put a

greater emphasis on the pace of hikes being gradual. A clear discussion

along those lines may be a “soft signal” that an earlier start to rate

hikes, giving more assurance that a gradual pace can be taken, is the

preferred path of the FOMC’s majority."

-

"Because the meeting took place before China’s devaluation, that

discussion should not come up in the FOMC July minutes."

- "It’s also too early for that impact to be seen in the July CPI, which is the key data release tomorrow in the US ahead of the FOMC minutes. Our economists see the risks to the y/y rate as slightly on the upside – a “high” 0.2% m/m edge up in the core CPI index could push the y/y rate up from 1.8% to 1.9% y/y."

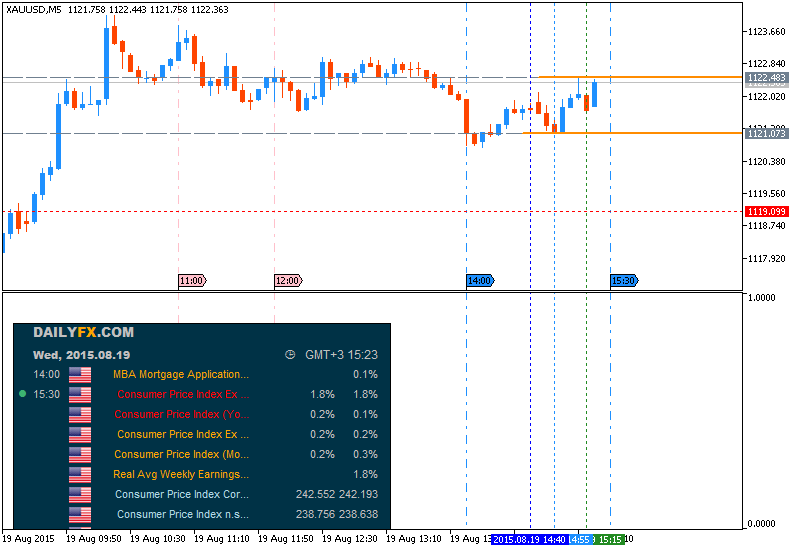

Gold (XAU/USD), M5 timeframe, 6 minutes before USD - CPI news event:

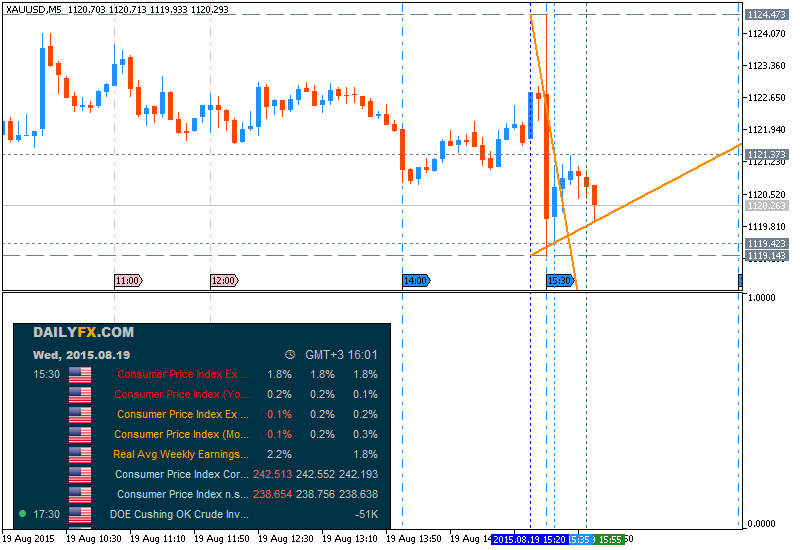

This is half an hour after USD CPI news event:

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.08.20 08:34

Time To Turn Bullish On EUR - Credit Suisse (based on efxnews article)

EUR will be on bullish, and the main reason for CS to decide it is the still-high risk that the ECB may have to re-enter the easing fray down the line:

"For example, as Exhibit 2 shows, European inflation breakevens have also been falling recently. With the ECB's credibility is on the line as it proceeds with its QE program, it is hard to imagine it standing pat for long and allowing sustained EUR strength to provide a fresh reason for these indicators to push still lower."

By the way - EUR/USD was already turned to bullish in intra-day basis:

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.08.21 06:54

Gold Climbs to Six-And-A-Half-Week High (based on wsj article)

"An unexpected rally in gold prices that was sparked by yuan’s

devaluation last week gathered pace, propelling the precious metal to a

six-and-a-half week-high on Friday. Gold breached the near-term

resistance level of $1,150 per troy ounce, showing the price rally has

taken a firmer hold of markets than was being earlier anticipated. Spot

gold rose 1.25% from the opening price to an intra-day high of

$1,168.32/oz, the highest level since July 3. It is currently trading at

$1,164.3/oz."

Forum on trading, automated trading systems and testing trading strategies

Sergey Golubev, 2015.08.22 09:53

Forex Weekly Outlook August 24-28 (based on forexcrunch article)

The US dollar suffered in a week that saw doom and gloom in global markets. Will this continue? German Ifo Business Climate, US CB Consumer Confidence, US Durable Goods Orders and GDP data from the US and the UK are the main highlights in Forex calendar. Join us as we explore the market-movers for this week.

The Federal Reserve released its July meeting minutes, revealing a dispute over the rate hike timing. Despite clear signals from some Fed officials calling for a rate rise in September, many policy makers still believe such a move is premature. In her capacity as the chair and the leader, Janet Yellen will be the driving force behind September’s decision. Will we see a rate hike in September? The chances look more slim with growing worries about China and fresh political uncertainty about Greece. The euro is clearly positioned as a safe haven currency and enjoys the crisis, alongside the yen. Dollar longs are on the other end.

- German Ifo Business Climate: Tuesday, 8:00. Business sentiment improved unexpectedly in July following two monthly declines upon an agreement between Greece and its creditors. The Ifo business climate index edged up to 108.0 from a revised 107.5 in June, beating expectations fora 107.6 reading. The Greek crisis resolution and the nuclear deal with Iran boosted sentiment. The survey showed brighter expectations, as well as better current conditions. Business sentiment is forecasted to reach 107.6 in August.

- US CB Consumer Confidence: Wednesday, 12:30. U.S. consumers were less optimistic in July. The Conference Board’s Consumer Confidence Index declined to 90.9 in July from 99.8 in the prior month, missing forecasts for 100.1. The reading registered its lowest level since September 2014. Current conditions remain positive, but the short-term expectations deteriorated, amid uncertainty concerning the labor market, and volatility in financial markets prompted by the situation in Greece and China. U.S. consumers are expected to be more positive in August. The index is expected to rise to 93.1.

- US Durable Goods Orders: Wednesday, 12:30. Businesses rebounded after a slow start. Orders for long lasting manufactured goods edged up 3.4% in June after a 1.8% fall in May. Economists forecasted a 3.2% gain. Business investments in manufacturing equipment and software also suggests a pickup in manufacturing in the coming months. However, uncertainty remains since the Durable-goods can be volatile. Meanwhile, orders excluding transportation gained 0.8%, the largest increase since August 2014. Overall, new orders in the first half of 2015 remain weak, down 2% from the same period in 2014. Orders for durable goods are expected to decline 0.5%, while core orders are forecast to gain 0.3%.

- Jackson Hole Symposium: Thursday, Friday and Saturday. Quite a few central bankers will be making their way to Jackson Hole Wymong for the annual conference. While Fed Chair Janet Yellen will not be attending, some other important figures will be speaking and rubbing shoulders in the corridors. This includes Vice Chair Stanley Fischer, BOE Governor Mark Carney and others. Remarks about the Chinese slowdown ,the euro-zone recovery and of course a potential US Fed hike from the people that matter most will all stir markets.

- US GDP data: Thursday, 12:30. According to the initial estimate, the US economy grew by 2.6% in Q2, a bounce back from an upwards revised 0.6% in Q1 but certainly not convincing enough. In the second estimate, an upgrade to 3.2% is on the cards. Will a significant upwards revision improve the mood? Ir it the gloom of Q3 here to stay?

- US Unemployment claims: Thursday, 12:30. The number of Americans filing initial claims for unemployment aid increased mildly last week, reaching 277,000. The 4,000 climb is still consistent with a solid job market. The four-week average increased 5,500 to 271,500. The average number of claims remain near a 15-year low, indicating the US labor market continues to strengthen. However, wage growth has yet to improve. Average hourly pay increased a mere 2.1% from 12 months earlier, far less the 3.5% to 4% gains viewed in healthy economies. The number of jobless claims are expected to reach 275,000 this week.

- UK GDP data: Friday, 8:30. The UK economy returned to stronger growth in Q2: 0.7% according to the initial read. This was as expected and stronger than +0.3% seen in Q1. A confirmation of this number is on the cards for the first revision.

- US Goods Trade Balance: Friday, 12:30. This new report from the U.S. Commerce Department was released in July. The event is issued four to seven days prior to the existing report on International Trade in Goods and Services, excluding services or trade in goods on a balance of payments basis. This data is included in the GDP report aimed to improve the accuracy of the first estimate. The Goods Trade Balance for June showed a trade deficit at $62.26 billion.

- Mark Carney speaks: Saturday, 2:25. BOE Governor Mark Carney is scheduled to speak about inflation Dynamics and Monetary Policy at Jackson Hole Symposium. He may talk about the low inflation trend in the UK and his concerns that inflation might fall below zero again postponing any rate hike initiatives this year.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Daily price is located below Ichimoku cloud for the primary bearish market condition with secondary ranging between the following s/r lines:

Chinkou Span line is below the price for the ranging condition to be continuing.

D1 price - ranging bearish:

W1 price is on bearish market condition with 1077.19 support level for descending triangle pattern to be crossed for the bearish trend to be continuing.

MN price is on bearish with 1077.19 as the nearest support level for this timeframe.

If D1 price will break 1077.19 support level on close D1 bar so we may see good bearish breakdown of the price movement.

If D1 price will break 1126.67 resistance level so the price will be on local uptrend as the secondary market rally up to 1164.81 as the next level in this case.

If D1 price will break 1164.81 resistance level so the price will be reversed to the primary bullish market condition.

If not so the price will be on ranging between the levels.

SUMMARY : bearish

TREND : ranging