Machine learning in trading: theory, models, practice and algo-trading - page 558

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

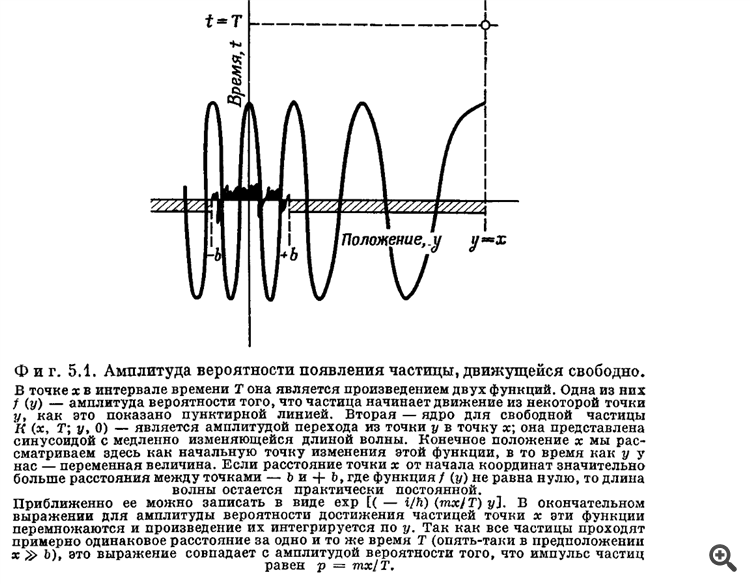

To top it off - figures from R. Feynman's monograph on probability amplitudes of quantum transitions

Something resembles the graphs that SanSanych posted, doesn't it?

Hold me seven - I'm about to start broadcasting a new theory for 3-4 months... ^))))))))

To top it off - figures from R. Feynman's monograph about probability amplitudes of quantum transitions

Somewhat reminiscent of the graphs posted by SanSanych, isn't it?

Hold me seven - I'm about to start broadcasting a new theory for 3-4 months... ^))))))))

The main thing is not to let it all go to eternity :) it seems, but here the probabilities at different amplitudes on an already, say, detrended chart. And if we add the trend component it will be even more complicated

Hold me seven - I'm about to start broadcasting a new theory for 3-4 months... ^))))))))

it turned out that the simple NS beyond the boundaries of the training sample works very poorly, too ....

Not a simple NS, but an NS of a certain configuration. From top to bottom.

Generated from this (1) - this (2), fit this (3) ......)))))

Not a simple NS, but an NS of a certain configuration. From top to bottom.

generated from this(1) - this(2), fit this(3)......)))))

at this point my brain finally snapped :) screw it, I'll just convert BP :)

this non-linear world... listening to Gordon in the background :)

I'm going to convert BP :)

Vizard_'s posts make even my quantum brain break...

In my opinion, under this nickname the closest relative of R. Feynman sprinkles here posts :))))

That's why it's easy to get confused, let's say we were using linear or regression and everything was ok, and then we decided to switch to MLP for the same tasks... and no way :)

That's why everybody prefers classification, though regression is good for forecasting :)

I would even say that linear or regression is more suitable for trends, and MLP for flat

Well, firstly, we need only classification - whether to enter a deal or not. That's all. We don't need anything else - only 1 and 0. MLP does that very well. Why do we need forecasting? - I don't understand it at all.

Secondly, for MLP we need to clearly formulate the task, and cut off everything unnecessary, leaving it to algorithmic methods. And thirdly, when teaching, don't impose your solution on MLP, as it is done in most local articles.

Well, first of all, we only need a classification - to enter or not to enter the deal. That's all. We don't need anything else, just 1 and 0. MLP does that just fine. Why do we need forecasting? - I don't understand it at all.

Secondly, for MLP we need to clearly formulate the task, and cut off everything unnecessary, leaving it to algorithmic methods. And third, when teaching, do not impose your solution on the MLP, as is done in most local articles.

Forecasting is a way to crash, but you can estimate a probability of future instability :) forecasting is needed to adapt the system to new conditions, ns, itself retraining, is fit to market changes periodically

And the classifier just works with the results of the first ns

Classification is also a prediction, but through a combination of bays/sells, i.e. simple optimization, it can be done rather qualitatively with the standard optimizer

yeah in general i don't know, i just do it that way, it's fun

+ i don't have such a neurocell like you have, and in the mql version it's absent

I'll also soon finish it in 2 variants, we'll see... I've forgotten about it during the holidays

Forecasting is a way to crash, but you can estimate probability of future instability :)

Classification is forecasting too, but through combination of bays/cells, i.e. simple optimization, it may be done rather qualitatively by standard optimizer

The classifier may well cope with instability probabilities, at least with the boundaries where a trade may be relevant.

Is an in-house optimizer good enough? - I'm not sure at all, I'm rather sure in the opposite).

+ I don't have such a neural network like yours, and in mql version it's absent.

The classifier is quite able to cope with the probabilities of instability, at least with the boundaries where the transaction may be relevant.In general, the problem of determining the probabilities may not have a solution at all.

Is an in-house optimizer good enough? - I'm not sure at all, I'm rather sure of the opposite).

And here I make a forecasting tool, then on some history I immediately evaluate its quality... if the quality is ok then I teach the second one to trade according to forecasts and it simply defines where it is better to buy/sell.

(at first it just had fuzzy logic, but then I decided to replace it with the Boolean one)

If there are a lot of parameters in the cloud, it will take the same 24 hours to train as in your case... The problem is the same - the optimization of the target f-function