NZDUSD Technical Analysis 2014, 18.05 - 25.05: Correction to Breakdown

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.05.19 05:35

2014-05-18 22:45 GMT (or 00:45 MQ MT5 time) | [NZD - PPI Input]

- past data is -0.7%

- forecast data is 0.4%

- actual data is 1.0% according to the latest press release

if actual > forecast = good for currency (for NZD in our case)

NZD PPI Input = Change in the price of goods and raw materials purchased by manufacturers

==========

New Zealand Q1 PPI Outputs Add 0.9%, Inputs Up 1.0%Output producer prices in New Zealand climbed 0.9 percent on quarter in the first quarter of 2014, Statistics New Zealand said on Monday.

The output PPI - prices received by New Zealand producers - topped forecasts for an increase of 0.7 percent following the 0.4 percent contraction in the fourth quarter.

Input prices - prices of goods and services used by New Zealand producers - climbed 1.0 percent on quarter, topping expectations for 0.4 percent after shedding 0.7 percent in the three months prior.

"The higher prices for electricity generation contributed to both the higher input and output PPIs in the latest quarter," prices manager Chris Pike said. "This often happens in March quarters, due to spot-market conditions and low lake levels."

The output electricity and gas supply price index rose 14 percent, which contributed more than half of the rise in the output PPI. The input electricity and gas supply price index (up 20 percent) contributed nearly three-quarters of the rise in the input PPI.

Higher prices for raw milk resulted in an increase in prices received by dairy cattle farmers (up 4.0 percent), and an increase in input prices paid by dairy product manufacturers (up 3.1 percent) in the latest quarter.

On a yearly basis, producer rice outputs climbed 4.0 percent after gaining 3.8 percent in Q1, while inputs added 3.1 percent after rising 2.8 percent in the previous three months.

On a yearly basis, the output electricity and gas supply price index rose 2.8 percent, while inputs rose 0.7 percent.

The prices received by the dairy cattle farming industry surged 47 percent, and the prices paid by the dairy product manufacturing industry spiked 39 percent.

Also on Monday, the bureau said that capital goods prices in New Zealand were up 0.6 percent on quarter in Q1.

The major upward contributions to the capital goods price index came from the residential buildings price index (up 1.1 percent), and the non-residential buildings price index (up 0.8 percent).

The gains were offset by a decrease in the price index for transport equipment (down 0.4 percent). The appreciating New Zealand dollar against most key currencies also influenced this price change.

On a yearly basis, the CGPI rose 2.1 percent. The increases for residential buildings (up 4.6 percent) and non-residential buildings (up 3.5 percent) were the highest since 2008, the bureau noted.

Finally, the Performance of Services Index came in with a score of 58.9 in April, up from the upwardly revised 58.5 in March (originally 58.3) - and accelerating above the line of 50 that separates expansion from contraction.

MetaTrader Trading Platform Screenshots

MetaQuotes Software Corp., MetaTrader 5, Demo

NZDUSD M5 : ~ 0 pips price movement by NZD - PPI news event

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.05.17 11:16

Forex Fundamentals - Weekly Outlook May 19-23Rate decision in Japan, inflation data in the UK and Canada, FOMC Meeting Minutes, Unemployment Claims, German Ifo Business Climate and US housing data are the main events on our list. Here is an outlook on the main market-movers for this week.

Last week, major US figures came out above expectations; Annual inflation reached 2%, as expected and the monthly CPI edged up to 0.3%. Meanwhile, the annual core inflation beat forecasts with a 1.8% reading. Furthermore, the sharp drop in the number of unemployment claims reaching a 7-year low of 297,000, reaffirms the strength of the US labor market. These positive signs support the Fed’s tapering plan, indicating the US economy is getting stronger and does no longer need QE. Will the US housing data also change for the better this week.

- UK inflation data: Tuesday, 8:30. UK inflation remained below the BOE’s 2.0% inflation target in March, reaching 1.6%, the lowest reading since October 2009. This reading was preceded by 1.7% in February. This was the sixth consecutive month of low inflation narrowing the gap between wage growth and the rise in prices contributing to business stability. UK inflation is expected to increase to 1.7%.

- Japan rate decision: Wednesday. Governor Haruhiko Kuroda maintained the BOJ’s monetary policy in April expressing confidence that the economy is advancing according to plan. However, many analysts believe the BOJ will have to ease policy in the near future to prevent a deflation trend. Kuroda told Prime Minister Shinzo Abe that he will adjust policy without hesitation in case the 2.0% inflation target may be jeopardized. No change is expected this time.

- US FOMC Meeting Minutes: Wednesday, 18:00. FOMC minutes released in April indicate the Fed’s intention of maintaining loose monetary policy for years to come. The FOMC welcomed the pickup in GDP growth registered after the weak first quarter affected by the cold weather. The members supported a low fed funds rate for as lonf as inflation remains below the 2% target. Tapering should continue and changes to guidance are possible. The FOMC expects that the economy will improve.

- UK GDP data: Thursday, 8:30. According to the NIESR estimates GDP edged up 1.0% in the second quarter after posting a 0.8% expansion rate in the first three months of 2014. The growth levels nearly equal the pre-financial crisis peak. NIERS forecasts a 2.9% growth rate in 2014. However, despite the pick-up, income per capita will need another three years to catch up with GDP expansion. GDP growth in the second quarter is expected to reach 0.8%.

- US Unemployment Claims: Thursday, 12:30.Initial claims for U.S. unemployment benefits hit a seven-year low of 297,000 claims last week, confirming the strong recovery in the US economy. Claims fell 24,000 from the preceding week, indicating stronger economic growth in the second quarter. Stronger labor market and rising inflation pressures give green light to the Fed’s ongoing tapering move. Jobless claims are expected to increase to 312,000.

- US Existing Home Sales: Thursday, 12:30. Second hand homes sales declined to their lowest level in more than 1-1/2 years in March, reaching an annual rate of 4.59 million units. However, sales were stronger than the 4.57 million forecasted by analysts, indicating that the negative trend in the housing market may be over. Supply increased as well as the number of first time buyers. Existing Home Sales are expected to rise to 4.71 million.

- German Ifo Business Climate: Friday, 8:00. German business climate index rose to 111.2 in March, following a revised 110.7 in February. The reading was stronger than the 110.5 points forecasted by analysts. The Ukraine crisis took less attention in the survey despite Barack Obama’s warnings of additional sanctions against Russia in case it fails to reach an agreement with Ukraine. German business climate is predicted to reach 111.

- US New Home Sales: Friday, 14:00. Sales of new U.S. homes plunged to their lowest level in eight months reaching a seasonally adjusted annual rate of 384,000 units in March. It was the second consecutive monthly drop indicating a slowdown in sales. Economists expected sales to increase to 455,000 saying the unexpected drop may be related to cold weather conditions. However, the weak demand increased the months’ supply of houses on the market to 6.0, the highest level since October 2011, from 5.0 months in February. New home sales are expected to reach 426,000.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.05.17 18:11

NZD/USD forecast for the week of May 19, 2014, Technical AnalysisThe NZD/USD pair tried to rally during the course of the week, but as you can see pulled back to form a shooting star for the second week in a row. It appears that we are in the middle of consolidation, so it’s difficult to imagine that were going to break down significantly from here, but the fact is that we will more than likely test the 0.85 level in the short term. We believe that a supportive candle in that area is a nice longer-term buying opportunity as the market should head to the 0.90.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.05.18 15:29

NZD/USD Fundamentals - weekly outlook: May 19 - 23The New Zealand dollar fell from the previous session’s one-week high against its U.S. counterpart on Friday, amid indications that the U.S. economy is shaking off the effect of a weather-related slowdown over the winter.

NZD/USD hit 0.8694 on Thursday, the pair’s highest since May 7, before subsequently consolidating at 0.8634 by close of trade, down 0.12% for the day but still 0.25% higher for the week.

The pair is likely to find support at 0.8607, the low from May 13 and resistance at 0.8694, the high from May 15.

The Commerce Department reported Friday that U.S. housing starts rose 13.2% last month, the largest increase in five months and following a 2.0% increase in March.

The upbeat housing data came one day after a report from the U.S. Department of Labor showed that the number of people who filed for unemployment assistance in the U.S. last week fell to a six-year low of 297,000.

The robust data underlined the view that the U.S. economy was regaining traction after being slowed by unusually cold temperatures during the winter months.

Meanwhile, in its annual budget release published Thursday, New Zealand's Treasury said the operating surplus will be NZ$372 million in the year through June 2015, up from a previously forecast NZ$86 million.

The Treasury also forecast the nation's jobless rate will decline to 4.4% in 2018 from a projected 5.4% next fiscal year.

The report came after Reserve Bank of New Zealand Chairman Graeme Wheeler said last week that the speed and extent of further interest rate increases will depend on economic performance and how much the nation’s strong currency weighs on inflation.

The central bank has already raised its benchmark interest rate twice this year to 3%, after keeping at a record low 2.5% to support the economy.

Data from the Commodities Futures Trading Commission released Friday showed that speculators decreased their bullish bets on the New Zealand dollar in the week ending May 13.

Net longs totaled 19,340 contracts as of last week, compared to net longs of 20,693 contracts in the previous week.

In the week ahead, investors will be looking to the minutes from the Federal Reserve's latest monetary policy meeting, due for release on Wednesday, for insight on the central bank's view of the economy.

Ahead of the coming week, Investing.com has compiled a list of these and other significant events likely to affect the markets.

Monday, May 19

- New Zealand is to publish data on producer price inflation.

- Federal Reserve Bank of Philadelphia Charles Plosser and Federal Reserve Bank of New York President William Dudley are to speak.

- Fed Chair Janet Yellen is to speak at an event in New York. Later Wednesday, the Fed is to publish the minutes of its May meeting.

- New Zealand is to produce data on inflation expectations.

- China is to publish the preliminary reading of the HSCB manufacturing index. The Asian nation is the New Zealand’s second-largest trade partner.

- The U.S. is to release its weekly report on initial jobless claims and private sector data on existing home sales.

- The U.S. is to round up the week with data on new homes sales.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.05.22 10:08

2014-05-22 01:45 GMT (or 03:45 MQ MT5 time) | [CNY - HSBC Manufacturing PMI]

- past data is 48.1

- forecast data is 48.1

- actual data is 49.7 according to the latest press release

if actual > forecast = good for currency (for CNY in our case)

CNY - HSBC Manufacturing PMI = Level of a diffusion index based on surveyed purchasing managers in the manufacturing industry

==========

China Manufacturing PMI Jumps To 49.7 - HSBC

An index monitoring manufacturing activity in China came in with a score of 49.7 in May, the latest flash estimate from HSBC and Markit Economics revealed on Thursday.

That topped forecasts for a score of 48.3 and was up sharply from 48.1 in April - and while it does remain below the line of 50 that separates expansion from contraction, the May reading represents a five-month high.

"The improvement was broad-based with both new orders and new export orders back in expansionary territory. Disinflationary pressures also eased over the month and output prices increased for the first time since November 2013," said HSBC Chief Economist, China & Co- Head of Asian Economic Research Hongbin Qu.

Among the individual components of the survey, the index for manufacturing output came in at 50.3 - up from 47.9 in April to a four-month high.

The index for new orders swung to expansion from contraction a month earlier - as did new export orders, output prices, stocks of purchases and quantity of purchases.

Backlogs of work continued to contract, but at a slower pace - as did input prices. The employment index declined at a faster pace, while stocks of finished goods turned to contraction after expanding last month.

Suppliers' delivery times lengthened in May after showing no change in the previous month.

"The employment index fell further to 47.3, which implies that this month's uptick in sentiment has not yet filtered through to the labor market. Some tentative signs of stabilization are emerging, partly as a result of the recent mini-stimulus measures and lower borrowing costs. But downside risks to growth remain, particularly as the property market continues to cool. We think more policy easing is needed to put a floor under growth in the coming months," Hongbin said.

MetaTrader Trading Platform Screenshots

MetaQuotes Software Corp., MetaTrader 5, Demo

NZDUSD M5 : 30 pips price movement by CNY - HSBC Manufacturing PMI news event

Forum on trading, automated trading systems and testing trading strategies

Something Interesting in Financial Video May 2014

newdigital, 2014.05.22 20:15

The AB=CD Pattern - Harmonic Ratios and Explanation

Alternative AB=CD Pattern

Forum on trading, automated trading systems and testing trading strategies

Something Interesting in Financial Video May 2014

newdigital, 2014.05.23 18:35

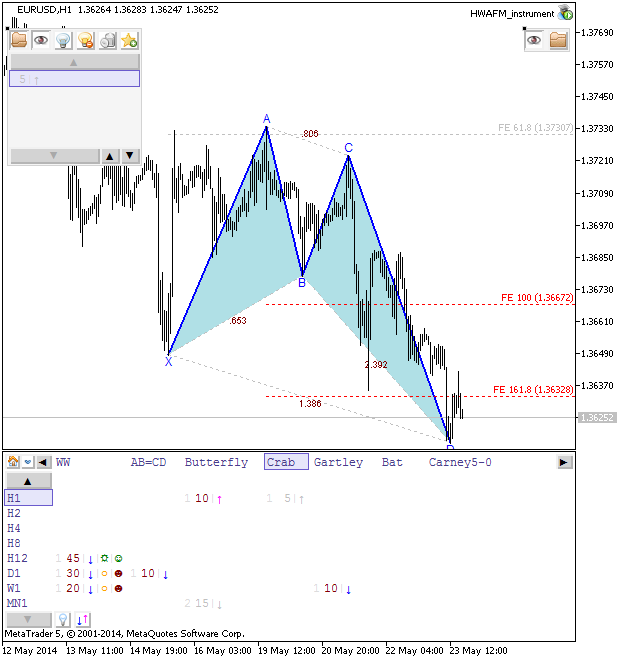

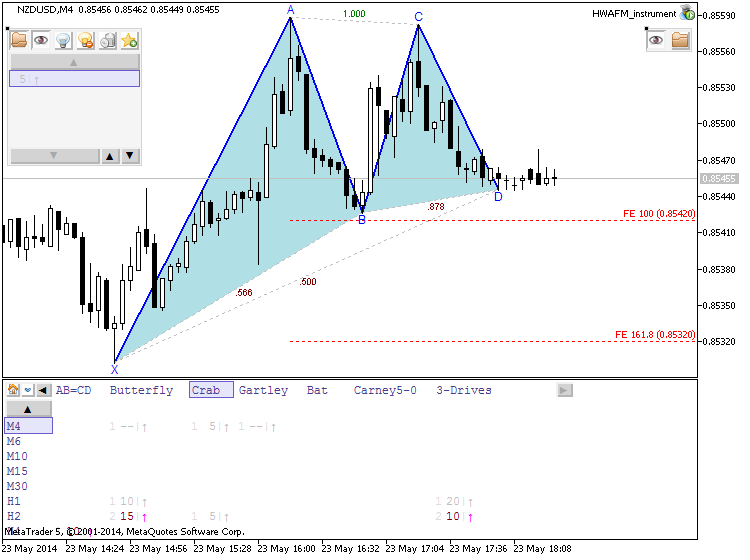

The Crab Pattern - Harmonic Ratios and Explanation :

The Deep Crab Pattern - Harmonic Ratios and Explanation :

The charts were made by using free HWAFM tool for Metatrader 5

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

D1 price: Chinkou Span line of Ichimoku indicator crossed historical price from above to below on open D1 bar for possible breakdown of the price movement in the near future. If this breakdown will be continuing and price will break 0.8603 support level on close D1 bar so we may see good price movement together with secondary ranging market condition: D1 price will be inside Ichimoku cloud/kumo.

H4 price: Chinkou Span line of Ichimoku indicator crossed historical price from above to below on open H4 bar for possible breakdown within primary bearish market condition for H4. This Ichimoku signal (Chinkou Span breakdown together with the price below kumo) is very strong signal for possible downtrend, and this situation may be validated if H4 bar will close with same signals on previous close H4 bar.

W1 price: flat within primary bullish.

If D1 price will break 0.8603 support so correction will be continuing with good possibility to reversal to bearish market condition.

If not so we may see the ranging market condition within primary bullish.

UPCOMING EVENTS (high/medium impacted news events which may be affected on NZDUSD price movement for this coming week)

2014-05-18 22:45 GMT (or 00:45 MQ MT5 time) | [NZD - PPI]

2014-05-20 22:45 GMT (or 00:45 MQ MT5 time) | [NZD - Visitor Arrivals]

2014-05-21 15:30 GMT (or 17:30 MQ MT5 time) | [USD - Fed Chair Yellen Speech]

2014-05-21 18:00 GMT (or 20:00 MQ MT5 time) | [USD - FOMC Meeting Minutes]

2014-05-22 01:45 GMT (or 03:45 MQ MT5 time) | [CNY - HSBC Manufacturing PMI]

2014-05-22 03:00 GMT (or 05:00 MQ MT5 time) | [NZD - Inflation Expectations]

2014-05-22 14:00 GMT (or 16:00 MQ MT5 time) | [USD - Existing Home Sales]

2014-05-23 14:00 GMT (or 16:00 MQ MT5 time) | [USD - New Home Sales]

Please note : some US (and CNY) high/medium impacted news events (incl speeches) are also affected on NZDUSD price movement

SUMMARY : bullish

TREND : correction

Intraday Chart