*Daily Forex market overviews by MasterForex.com* - page 42

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

Overview of the main economical events of the current day - 04/06/2013

Manufacturing PMI in the USA turned out the lowest for almost four years

The dollar slumped on Monday after the release of weak manufacturing PMI data. ISM Manufacturing PMI fell to 49 points since April’s 50.7 points – having dropped for the first time this year lower than the level of 50 which separates the activity growth from its fall. The index in May turned out the lowest since August, 2009. The output and new orders subindex dropped most of all.

Construction expenses turned out also lower than expected having risen by 0.4% against the forecasted growth by 1.0%. The dollar fell lower than 88 yen – for the first time since May, 9. It may turn out too early to expect scaling back of QE-3 incentive program with such statistics.

At the same time the euro-zone PMI is a little better than expected although it is still lower 50 points which separate recession from recovery. Final manufacturing PMI reached 48.3 in comparison with 46.7 in April having reached the 15-month high. The index movement justifies the ECB forecasts about the euro-zone economic recovery in the second half of the year, which significantly reduces the probability of rate reduction at the ECB meeting this Thursday.

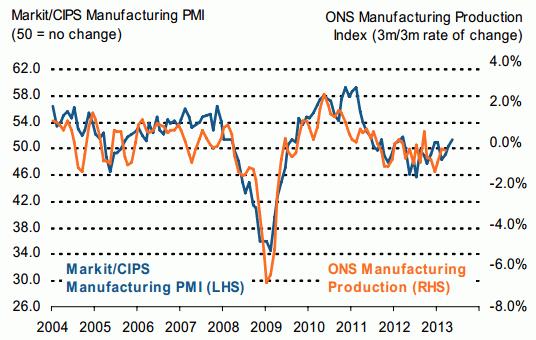

The pound grew on Monday also after the release of the same PMI statistics data which rose to 14-month high in May. Manufacturing PMI reached 51.3 level while the growth up to 50.3 was expected. The reading of March was also revised upwards up to 50.2 from 49.8. It reduces the probability of extra easing of the monetary policy at the nearest meetings of the Bank of England.

Source: markiteconomics.comThe Australian and New Zealand dollar grew on Monday amid rising commodity prices. The official manufacturing PMI of China released by the National Bureau of Statistics of China on Saturday rose up to 50.8 points in May from 50.6 in April. The Australian dollar fell by 7.7% in May, which has become the most significant drop among all major currencies. Although no change of rate is expected in June, interest rate swap market forecasts its fall in September with a probability of 57%.

Meanwhile San Francisco Fed president John Williams announced on Monday in Stockholm that the Fed was likely to start reducing the volume of bond redemption this summer and finish the quantitative easing program at the end of the year. But Williams is not a voting member of the FOMC this year.

By MasterForex Company

Overview of the main economical events of the current day - 05/06/2013

Calm before the storm

The dollar almost didn’t change against the euro and the pound on Tuesday and rose against the yen and commodity currencies after a considerable drop on Monday. The euro and the pound traded in rather narrow ranges and trading is likely to be so till Friday waiting for a key report on the USA labor market which can make clear possible future actions of the Fed towards an earlier exit from incentive programs.

There were almost no important data on the USA except the trade balance which turned out a little better than expected. Trade balance deficit rose up to $40.3 bln in April while a growth up to $41 bln was expected. However the deficit rose significantly in April by 8.5% in comparison with prior month due to a higher growth of import. IBD/TIPP Economic Optimism Index grew up to 49 in June vs 45.1in May but didn’t reach the forecasted level of 50.

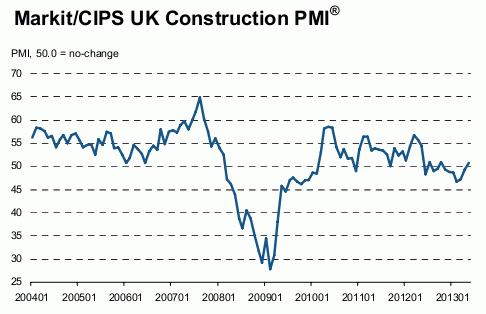

The pound had almost no reaction towards the release of construction PMI which is again better than forecasted and shows a growth along with the PMI of other economic sectors. After six months of decline when the index was lower 50, British construction PMI rose up to 50.8 against 49.4 earlier. A rise up to 49.6 was expected. There is a chance that on Wednesday service PMI will be also better than forecasted.

Source: markiteconomics.comSpanish unemployment change decreased significantly by 98.3 thousand people while it was expected to fall only by 50 thousand. However producer prices of the euro-zone fell in April for the second month in a row and its decline rate was the fastest for almost four years. Producer price index dropped by 0.6% m/m with a forecast of decline by 0.2%. Weak inflation data can give Mario Draghi more opportunities in future to ease monetary policy.

The Australian dollar fell significantly on Tuesday after the Reserve Bank of Australia had kept the key interest rate at the same lowest level 2.75% but had marked that the Australian dollar was still high. It also didn’t rule out the possibility of further rate decline according to a favorable forecast on inflation.

Meanwhile the negative balance of the Australian current account has considerably decreased for the first quarter, having fallen by 42% for the first quarter and having reached the forecasts. Australia Net Exports of GDP amounted to 1.0%, which turned out higher than the experts’ estimate 0.8%.

The dollar rose against the yen and again exceeded 100 yens per dollar amid the rise of the Nikkei 225 which rocketed by 2.1% on Tuesday. The experts of the Morgan Stanley Bank believe that USDJPY correction can last all summer. The decline in stock markets and the increased bond market volatility shake faith of market participant in success of «abenomics» and in the ability of the Bank of Japan to manage the deflation.

By MasterForex Company

Overview of the main economical events of the current day - 06/06/2013

ADP labor market data are again worse than forecasted

Statistics data from the USA on Wednesday again didn’t please the bulls of the US currency. Preliminary ADP labor market data turned out worse than expected and haven’t been reaching forecasted reading for the third month in a row. Besides, factory orders also turned out worse than expected. Revised unit labor costs also slumped for the past quarter.

Service PMI in May was a little better than forecasted – which almost didn’t support the dollar. As a result, the dollar significantly weakened against the pound and the yen, it almost didn’t change against the euro and CAD and continued growing only against the AUD and NZD.

Automatic Data Processing (ADP) survey released on Wednesday showed that nonfarm private payroll employment rose by 135 thousand against forecasted 170 thousand. Prior month data were also lowered from 119 thousand to 113 thousand. ADP survey is often considered preliminary before a key labor market report which is released two days later on Friday.

Factory orders rose by only 1% in April in comparison with the prior month while a more significant growth was expected – by 1.4%. March data also became worse to -4.7% while before it was reported to decline only by 4%. Revised unit labor costs dropped by 4.3% for the first quarter having shown the sharpest decrease since 1947. Earlier the reading was reported to rise by 0.5% and no changes were expected.

ISM Non-Manufacturing PMI grew up to 53.7 in May in comparison with 53.1 in April and a little beat the forecast of 53.5. PMI growth rate increased but the employment subindex fell.

The same service PMI of Great Britain was much better than forecasted, which allowed the pound to show a steady growth against all currencies. Service PMI rose up to 54.9 in May from 52.9 in April – it is the highest reading since March, 2012. Service sector is about ¾ of the UK economy.

The euro continued to trade flat - a little lower 1.31. It didn’t manage to maintain above this level due to weak data. The final services PMI of the euro-zone decreased to 47.2 from 47.5 in May. Meanwhile in Spain the PMI rose, in Italy it fell, in France it remained unchanged and in Germany slightly decreased. Realized sales in euro-zone fell more than expected in April by 0.5% and they have been decreasing for the third month in a row as in Germany.

The yen rose on Wednesday amid a sharp Nikkey decline which fell by 3.8% after the prime minister of Japan had introduced a new plan of reflation – so-called «third arrow» of economic policy. He promised to raise the per capita GDP by 3% and more every year during next 10 years, to create special economic zones and so on. But investors were not inspired by such plan and they greeted it by selling securities.

The Australian dollar continued the prior day’s fall on Wednesday, which was supported by the GDP data. The Australian GDP rose only by 0.6% for the first quarter while a growth by 0.8% was expected. Year-on-year the growth was 2.5% while 2.7% growth was expected.

By MasterForex Company

Overview of the main economical events of the current day - 07/06/2013

Dollar dropped ahead of the key US employment data report issue

On Thursday, the dollar's rate fell dramatically against all majors, though no external force contributed to it. Probably, market players reacted to Friday’s adverse employment data in advance by correcting their positions ahead of this primary event. And dramatic drop of dollar along with stock markets disruption started just after the beginning of ECB head Mario Draghi's press-conference concerning ECB's meeting results.

ECB decided to leave the rate unchanged. Strain of Mario Draghi’s comments remained unchanged as well. Once again he pointed at economic problems and risks, but, therewith expressed his hope that business activity will recover within one year. Inflationary expectations still remain low, and stimulatory measures will be utilized as long as necessary.

This year’s Euro Zone GDP forecasts got worse due to remaining downward risks. But Mario Draghi let everyone know that the key interest rate decrease is not something to wait for as of now. EURUSD pair reacted to the statement by growing significantly.

Bank of England also decided to leave the rate and the assets acquisition program unchanged. The Pound was also supported by the Britain’s housing prices that were growing this May faster than ever within the 2.5 years period. The Halifax housing prices index increased by 0.4% in May though it was expected to grow just by +0.2%, which confirms housing market’s recovery.

Thursday’s Euro Zone data was mostly negative. Quarterly unemployment rate in France increased from 10.5% to 10.8% at once, thus, reaching its maximum since 1997. Order volume in Germany’s production industry decreased in April by 2.3% against the background of expected -1.0%.

At the same time the US data was not so bad. Quantity of initial applications for unemployment compensation in US decreased last week by 11 thousand: to 346 thousand against the expected decrease to 345 thousand.

The average 4-week initial applications quantity is 352.5 thousand in May, which exceeds the April's value by about 10 thousand. And Non-Farm Payrolls (NFP) to be issued on Friday is expected to be almost the same as in the last month (165-168 thousand). It’s most likely that NFP will turn out to be less by 20-30 thousand: about 140-150 thousand. But mostly, this reduction was already reacted to on Thursday. But in case the data will be in accordance to the forecasts, dollar stands a good chance for upwards correction after the recent sales.

By MasterForex Company

Overview of the main economical events of the current day - 10/06/2013

The main events of this week

Last week the dollar showed the largest decline over the year and fell by 2% in the dollar index which shows its relation towards the basket of six major currencies. During the week the dollar leveled the entire May increase. The largest decrease was on Wednesday and Thursday after the ADP report when bad labor market data which must have been released on Friday were worked out.

The data of the USA Department of Labor turned out rather contradictory. On the one hand Non-Farm Employment Change rose by 175 thousand which is the largest increase since February. The data turned out a little higher than the forecast of 163-168 thousand and almost coincided with the growth of employment change for the last 12 months which is 172 thousand per month.

On the other hand unemployment rate increased by 0.1% up to 7.6% from 7.5% in April. Although, unemployment rate growth can be explained by the fact that the population has started to return to the labor market. It is indirectly proved by the growth of participation rate from 63.3% to 63.4% and by the decrease of population not in labor force by 231 thousand. Underemployment rate (U6), which includes discouraged workers and part time workers, has fallen from 13.9% to 13.8% for the past month.

In general the USA labor market data turned out a little better than expected. The dollar was decreasing in anticipation of bad data and now its corrective bounce can go on this week facing 2-day meeting of the Fed which will be held next week June 18,19.

On weekend there was a release of a large Chinese data block. Inflation continued to fall and new loans also dropped. Industrial production and trade balance were as forecasted. However, imports and exports decreased significantly. The released data are negative for the Australian dollar as the currency of the main trade partner of China.

This week there will not be a lot of important macrostatistics data. Market participants will think over the key data of the US labor market released on Friday. There will be two meetings of Japanese and New Zealand central banks.

As usually, on the second week of the month industrial production and inflation data will be released. There will be a release of the UK and Australian labor market data. On Wednesday the German Federal Constitutional Court is due to announce a ruling regarding the constitutionality of the ECB's Outright Monetary Transactions policy (OMT). The hearings will be held two days – on Tuesday and Wednesday.

The USA realized sales will be released on Thursday; and producer prices and Prelim U. of Michigan Consumer Sentiment - on Friday. Traditionally, on the second week of the month long-term US bonds will be sold from Tuesday to Thursday. In theory, it may lead to the dollar increase and reduce of risky assets.

10-Jun (UTC+4)

13:00 Germany to Sell EUR4 bln 182-day Bills

17:00 France to Sell Bills

11-Jun

12:00 the Netherlands to Sell Up to EUR3.5 bln 2016 Bonds

13:00 Greece to Sell EUR1.25 bln 182-day Bills

21:00 the USA to Sell $32 bln 3-year Notes

12-Jun

13:00 Italy to Sell 3- and 12-month Bills

13:30 Germany to Sell EUR5 bln 2015 Bonds

21:00 the USA to Sell $21 bln 10-year Notes

13-Jun

13:00 Italy to Sell 3-year Bonds (BTP)

21:00 the USA to Sell $13 bln 30-year Bonds

14-Jun

07:45 Japan to Sell 5-year Bonds

14:00 Belgium to Sell Bonds

By MasterForex Company

Overview of the main economical events of the current day - 11/06/2013

Standard & Poor's rating agency raised the outlook for the USA credit rating

By the end of Monday the dollar almost had not changed in the dollar index, it had risen to the yen and Australian dollar but had fallen to the euro a little. There were no any significant data on the USA on Monday, besides the markets of China and Australia were closed. The dollar tried to rise against the euro at the beginning of the day but during the second half of the day it lost all growth. Fed representative Bullard supporting asset purchases said on Monday that low inflation indicated that the Fed could still continue buying bonds. Inflation is still low due to low commodity prices, a slowdown in Chinese economy and weakness in Europe.

The dollar rose against the yen on the back of the start of 2-day meeting of the Japanese central bank and amid the release of Japanese GDP data for the first quarter revised upwards. It allowed Japanese stock index Nikkei to rise by 4.9% and to show the largest per cent rise since March, 16, 2011.

In the first quarter of 2013 the GDP of Japan was revised upwards (+4.1% year-on-year, earlier it was reported about 3.5% growth) and it proves the effectiveness of Abe Sondzo’s economic policy. In the fourth quarter of 2012 the GDP of Japan rose only by 1.2% year-on-year. Also in Japan a current account surplus was recorded in April at the level of 750 bln yens, which turned out twice more than expected.

The decision of the Standard & Poor's to raise the outlook for the USA sovereign credit rating from negative to a stable one had almost no effect on the markets. S&P announced that such decision shows a stronger economic momentum in the USA this year and the improvement of government’s budget situation.

The euro rose on the back of mixed industrial production data in France and Italy and also the growth of Sentix index of investors’ confidence. The euro was also supported by the statements of Fed president Mario Draghi who said that “the euro-zone will not get out of the debt crisis through inflation and that the ECB will not intervene only in order to help countries to maintain solvency”.

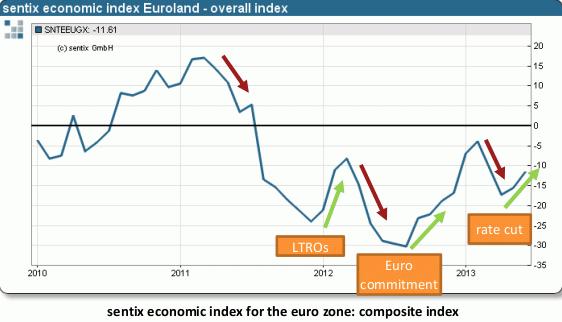

Industrial production growth in France amounted to 2.2% m/m, while 0.2% growth was expected and in annual terms industrial production decreased only by 0.5% with the forecast of 4% fall. At the same time industrial production in Italy decreased by 0.3% m/m in April while no changes were expected. Italian GDP rates of growth were revised downwards for the first quarter to -0.6% q/q from -0.5% before. Sentix investors’ confidence index rose up to -11.6 in June in comparison with -15.6 in May having shown the second monthly growth in a row but it turned out a little weaker than forecasted.

Source: sentix.deECB board member Joerg Asmussen said in the interview with the newspaper Bild that the potential decision of the German court against the ECB program of buying back government bonds of troubled euro-zone countries could mean new risks for the single currency. On Tuesday in Karlsruhe starts a two-day session of the Federal Constitutional Court of Germany, the highest judicial body of the country. The judges will consider the legitimacy of government bond purchase program "Outright Monetary Transactions" (OMT), which was announced by the ECB President Mario Draghi in September 2012. The court will also consider the question of the constitutionality of euro-zone stabilization fund - the European Stability Mechanism (ESM).

The Australian dollar dropped on Monday and fell lower 0.94 for the first time since October, 2011 after the publication of foreign trade data and inflation in China on weekend. Imports unexpectedly fell by 0.3% in May, while exports grew by only 1%, and the result was significantly lower than expected. Base metals imports decreased including copper and aluminum and also there was a sharp decrease of coil imports. The main supplier of these goods is Australia. Goldman Sachs lowered the outlook for Australian GDP for 2013 to 2.0% from 2.4% and expected that the AUDUSD would trade at 0.85 against 0.90 in 12 months.

By MasterForex Company

Overview of the main economical events of the current day - 12/06/2013

The Bank of Japan disappointed the market participants

The dollar fell by almost 3% against the yen on Tuesday having shown the biggest daily decline since May, 2010. After the 2-day meeting that was over on Tuesday the Bank of Japan kept the monetary policy line without changes having abstained from extra economic support measures including the expected prolongation of credit operation period which is used to decrease the volatility at the debt security market. The market participants had some hopes that the Bank of Japan would approve credit operations for at least one year.

However the central bank didn’t meet the market expectations. As a result the yen rose sharply. An extra factor of the dollar decline was the result of the auction for the sale of 3-year U.S. Treasury notes, which showed a rather weak result. Securities yield rose to 0.581% from 0.354% the previous month, which is higher by more than 58%. The US Treasury 2-year and 3-year securities are traditionally popular for purchases from Japanese investors. The analysts of the Bank of America believe that further scale back of USDJPY positions can push it into 91 area.

The dollar crash against the yen weakened the dollar against other major currencies: euro, pound and franc. Commodity currencies managed to compensate its fall by the end of the day and closed almost at zero. EURUSD exceeded the level of 1.33 on the back of the German constitutional court meeting about the legitimacy of ECB peripheral bonds purchase program (OMT). The ECB representative Asmussen said at the hearings that the ECB was ready for unlimited purchases of government bonds by the OMT; and that “the financial markets need a strong signal that the OMT program is unlimited”.

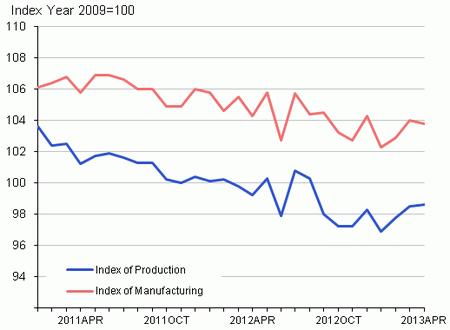

The pound rose on Tuesday and exceeded the level of 1.56 despite rather mixed industrial production statistics. According to the Office for National Statistics survey the production in the manufacturing industry of the country decreased by 0.5% in April in annual terms while a drop by 0.3% was forecasted. However the base industrial production indicator turned out better than expected as in April it rose by 0.1% vs March while the reading was not expected to change. RICS House Price Balance in May was better than expected.

Source: ons.gov.ukThe franc rose amid the publication of SECO economic forecasts. The Swiss government raised the forecast of the GDP growth in 2013 up to 1.4% from 1.3%. Meanwhile NFIB Small Business Index in May grew up to its high for a year having exceeded the expectations; and inventories at wholesalers in April increased by 0.2% as expected.

The Australian dollar updated an annual low against the dollar on Tuesday after the release of business confidence data in Australia but by the end of the day leveled almost all losses. According to the National Australia Bank data released on Tuesday the business confidence in Australia remained at the negative territory in May and was minus one point as the prior month. Negative indicator means that the number of pessimists is higher than the number of optimists. The biggest pessimism was found among mining companies.

By MasterForex Company

Overview of the main economical events of the current day - 13/06/2013

Dollar keeps on falling

Dollar weakened on Wednesday against the most majors backed by suspense surrounding the FRS stimulation program, at that again no notable macro statistics was issued in the US. Yen refreshed its weekly high against dollar on the ground of stock markets decline and Nikkei futures depreciation to the week’s low. Traders keep on taking profits and closing USDJPY long positions.

Euro resumed increasing on Wednesday to consolidate higher than 1.33 in EURUSD. Euro zone’s production industry statistics in April turned out to be exceeding expectations. Industrial production increased by 0.4% month-to-month, although it was supposed to remain unchanged according to forecasting. On an annualized basis it decreased by 0.6%, although decrease by 1.1% was predicted. Euro zone’s industrial production keeps increasing for three months on end, which might be an early symptom of economic rehabilitation.

Euro’s appreciation was also supported by ECB’s representative Asmussen saying that ECB won’t buy up obligations at a price which is too high, and ECB is more conservative than FRS. Moreover, Euro’s growth is caused by short-term loans interest rates growth in Europe, which indicates that expectations regarding the ECB rates’ future decrease reduced significantly.

Source: epp.eurostat.ec.europa.euThe Pound appreciated on Wednesday reaching 4-months high against dollar backed by good looking employment data. Claimant Count Change decreased dramatically in May exceeding expectations of most experts. According to the Office for national statistics’ report quantity of applications decreased by 8.6 thousand as compared to the April’s value 11.8 thousand reconsidered to be lower. Average Weekly Earnings (3M/y) increased by 1.3% as compared to the last year’s similar period, while growth by only 0.2% was expected. The previous quarter’s value increased as well from 0.4% to 0.6%.

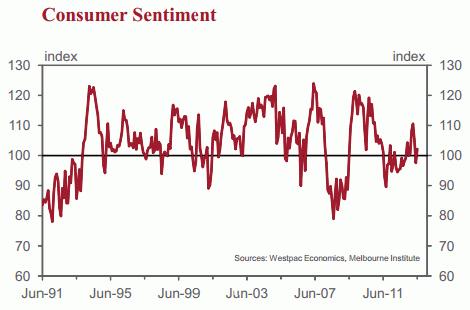

Australian dollar moved out of the three years low supported by consumer confidence increase inside the country. After two months of depreciation Westpac’s Consumer confidence index increased in June by 4.7% to 102.2 as compared to 97.6 in May. The index’s value exceeding 100 indicates there are more optimists than pessimists out there. The statistics made traders take their profits from Australian currency short positions, as, technically, Aussie looks overbought for quite a long time.

Source: westpac.com.auOn Wednesday New Zealand dollar also kept rebounding from the year’s lows. NZ Card Spending – Retail increased in May by 0.5% conforming to forecasts. NZ Card Spending increased in May by 0.6% after decreasing by 1.1% last month. REINZ House Sales increased by 7.5% on an annualized basis in May turning out to be the best May's result in the last 6 years. REINZ Housing Price Index increases for 5 months on end, and May’s growth amounted to 0.7% as compared to April's value.

Dollar keeps falling with FRS meeting waiting ahead on June, 18-19. It keeps increasing for 4 weeks in succession. While the first three days of the week almost lacked US events, at last important retail sales report is about to be issued on Thursday, just as traditional weekly Unemployment Claims.

By MasterForex Company

Overview of the main economical events of the current day - 14/06/2013

Retail sales turned out to be better than expected, though dollar dropped

Dollar could not turn the negative tendency and kept on decreasing in price on Thursday against most majors, in spite of encouraging retail sales and unemployment claims data happened to be better than expected.

Initial unemployment claims decreased last week by 11 thousand to 334 thousand against the expected increase to 350 thousand. US retail sales increased in May by 0.6% with expected increase by 0.4% - it’s the fastest growth rate in three months. Sales in April and March were reconsidered to be increasing.

Dollar dropped below 94.00 against Yen for the first time since the beginning of April due to dramatic decrease of Japanese stock index Nikkei that tumbled down by 6.4% on Thursday and already moved over to bear market for it fell from maximum points by more than 20% already. Negative mood was stimulated by the World Bank worsening its world economy forecasts, and news of Japanese investors that keep selling foreign bonds and stocks.

Euro and Pound managed to get back all that was lost during first half of the day and ultimately even increased a little. Euro was negatively affected by loan costs for Italy increased to maximum since March during the bond auction. Weighted average return of 3Y bonds increased to 2.38% against 1.92% of the previous auction held on May, 13. Pound got higher than 1.57 against dollar for the first time in 4 months.

Australian dollar kept up retracing and increased significantly on Thursday after employment data was issued. According to Australian Bureau of Statistics Employment Rate increased by 1.1 thousand people in May, while the value was expected to decrease by 10 thousand. Unemployment Rate remained unchanged and amounted to 5.5%, while it was expected to increase by 5.6%.

New Zealand dollar appreciated significantly as well after Reserve Bank of New Zealand decided to leave the rate unchanged at the level of 2.50%. RBNZ Governor Graeme Wheeler displayed his taste for tight-fisted policy but to a lesser degree than it was expected.

By MasterForex Company

Overview of the main economical events of the current day - 17/06/2013

Main events of the upcoming week

Summarizing Friday’s results dollar’s price almost didn’t change according to dollar index, though it kept on decreasing against Yen. In the beginning of the day it tried to rebound, but then tumbled down after June's Preliminary University of Michigan Consumer Sentiment happened to be worse than expected. The index fell down to 82.7, though it was expected to remain unchanged at 84.5.

The US Industrial Production also happened to be worse than expected in May: It remained unchanged, though expected to rise by 0.2%. Dollar was pushed down by The Wall Street Journal's article saying FRS will, probably, fall short of expectations and QE-3 shutting down process will supposedly linger a lot.

However, according to the week's results dollar index lost 1.25%. It’s worth mentioning that the DJIA stock index lost almost the same value within the week – it decreased by 1.17%. Analysts notice recent close correlation between dollar and American stock market. DJIA reached high on May, 22, and dollar index did the same the next day - then both indexes started to decrease.

The upcoming week will be quite rich for events judging by macro statistics that is going to be issued. German ZEW Economic Sentiment is issued on Tuesday in Europe. On Thursday Flash Manufacturing PMI & Flash Services PMI is published to show data on France, Germany and Euro Zone. Similar HSBC Flash Manufacturing PMI on China will be issued on Thursday.

In Britain production and consumer inflation data will be published on Tuesday, and retail sales data – on Thursday. On Friday inflation and retails sales data might be published on Friday. The 1st-quarter GDP data is to be issued in New Zealand on Thursday.

On Tuesday and Wednesday Meeting Minutes of Australia’s and UK's central banks will be published. Next scheduled Swiss National Bank’s quarterly meeting is to take place on Thursday. The Citi’s experts believe that to fight deflation SNB might start acting more aggressively and increase depth of negative interest rates.

But the main event of the week that might show markets' direction for the following months is Federal Open Market Committee (FOMC) meeting, results are to be announced on Wednesday. Market participants will wait for FOMC Statement with particular attention, as well as for FOMC Press Conference hosted by Ben Bernanke, that will be held half an hour after the statement announcement. FOMC Economic Projections on GDP growth, inflation and rates will be issued along with the press-conference. They are issued once per a quarter, usually in a quarter's end.

During his recent speech B. Bernanke let everyone know that the authority might start gradual shutting down of QE-3 within the following “few meetings”. Although, recent macro statistics obviously doesn’t count in favor of it. And in case the head of FRS won’t say anything about shutting the program down or will say something blurry, dollar’s rate might keep on falling further. CNNMoney’s polling among economists and analysts shown that almost two-thirds of them expect that FRS won’t cut monthly asset acquisition, at least until this December.

By MasterForex Company