Negative skew

Hello.

I opened this topic because i see the that this subject it is less known and discussed among the traders.

To understand in simple terms what negative skew means i will define it: a trading system has negative skew when most of the time you make small profits but occasionally you take a very large loss.

Many trading systems show a smooth equity curve and high win rate but to achieve this they often use a large initial stop loss and an aggressive trail stop.

Statistically is well known that it comes a time when that big loss or series of big losses will happen and it is just a matter of time.

Every trader must know if his system used for trading has a positive or negative skew because ultimately his long term success depends on it.

It's one thing to state that a potential pitfall exists. It's quite another to do something about it.

For algorithmic trading, drawdown can be statistically analyzed in the MT5 Testing Report: Testing Report - Algorithmic Trading, Trading Robots - MetaTrader 5 Help

For live trading/manual trading, drawdown can be statistically analyzed in the MT5 Trading Report: Trading Report - Trading Operations - MetaTrader 5 Help

Just because your car can go 150 MPH doesn't mean you should. Just because you have a lot of margin, doesn't mean you should use it. Control your risk.

Risk depends on your initial stop loss, lot size, and the value of the symbol. It does not depend on margin or leverage. No SL means you have infinite risk (on leveraged symbols). Never risk more than a small percentage of your trading funds, certainly less than 2% per trade, 6% account total.

-

You place the stop where it needs to be — where the reason for the trade is no longer valid. E.g., trading a support bounce, the stop goes below the support. Then you compute your lot size.

-

AccountBalance * percent/100 = RISK = OrderLots * (|OrderOpenPrice - OrderStopLoss| * DeltaPerLot + CommissionPerLot) (Note OOP-OSL includes the spread, and DeltaPerLot is usually around $10/PIP, but it takes account of the exchange rates of the pair vs. your account currency.)

-

Do NOT use TickValue by itself - DeltaPerLot and verify that MODE_TICKVALUE is returning a value in your deposit currency, as promised by the documentation, or whether it is returning a value in the instrument's base currency.

MODE_TICKVALUE is not reliable on non-fx instruments with many brokers - MQL4 programming forum (2017)

Is there an universal solution for Tick value? - Currency Pairs - General - MQL5 programming forum (2018)

Lot value calculation off by a factor of 100 - MQL5 programming forum (2019) -

You must normalize lots properly and check against min and max.

-

You must also check Free Margin to avoid stop out

-

For MT5, see 'Money Fixed Risk' - MQL5 Code Base (2017)

Most pairs are worth about $10 per PIP. A $5 risk with a (very small) 5 PIP SL is $5/$10/5 or 0.1 Lots maximum.

I don't just state Ryan L Johnson. I want to make aware the traders of this less known problem: negative skew.

Behind a smooth return equity curve or a high win rate often it's hidden this negative skew which in the end will hit hard in your trading account.

Using variable position size based on rsi, adx or other oscillator, taking partial profits based on a certain criteria affects your system skewness.

Backtesting is a useful tool but it does not say the full story. You can have impressive results in backtests and in real trading the system to be bad.

If the backtest results would be the solution we would trade a system with the best results.

To be even more clear if you toss a coin you have a 50% win rate in the long run. If when you get head you win 1point and when you hit tail you loose 1 unit in the long run you don't win anything. Now if when you hit head you win 1.1 points in the long run you are going to accumulate points.

This is positive expectancy for your system or positive skew.

To conclude backtests are not the magical answer because they can help as much as they can deceive.

Just because your car can go 150 MPH doesn't mean you should. Just because you have a lot of margin, doesn't mean you should use it. Control your risk.

Risk depends on your initial stop loss, lot size, and the value of the symbol. It does not depend on margin or leverage. No SL means you have infinite risk (on leveraged symbols). Never risk more than a small percentage of your trading funds, certainly less than 2% per trade, 6% account total.

-

You place the stop where it needs to be — where the reason for the trade is no longer valid. E.g., trading a support bounce, the stop goes below the support. Then you compute your lot size.

-

AccountBalance * percent/100 = RISK = OrderLots * (|OrderOpenPrice - OrderStopLoss| * DeltaPerLot + CommissionPerLot) (Note OOP-OSL includes the spread, and DeltaPerLot is usually around $10/PIP, but it takes account of the exchange rates of the pair vs. your account currency.)

-

Do NOT use TickValue by itself - DeltaPerLot and verify that MODE_TICKVALUE is returning a value in your deposit currency, as promised by the documentation, or whether it is returning a value in the instrument's base currency.

MODE_TICKVALUE is not reliable on non-fx instruments with many brokers - MQL4 programming forum (2017)

Is there an universal solution for Tick value? - Currency Pairs - General - MQL5 programming forum (2018)

Lot value calculation off by a factor of 100 - MQL5 programming forum (2019) -

You must normalize lots properly and check against min and max.

-

You must also check Free Margin to avoid stop out

-

For MT5, see 'Money Fixed Risk' - MQL5 Code Base (2017)

Most pairs are worth about $10 per PIP. A $5 risk with a (very small) 5 PIP SL is $5/$10/5 or 0.1 Lots maximum.

To conclude backtests are not the magical answer because they can help as much as they can deceive.

If you're deceived by your MT5 Tester Report, then you're not proficient with the Tester. New traders, manual traders, and new programmers frequently have trouble: properly coding Tester-complaint EA's (especially those that evaluate tick data); inputting average spread, average slippage, and/or commissions (all based on their live accounts); and overly auto-optimizing to undersized data samples. Accurately backtesting on Custom Symbols/charts adds another layer of complexity.

Of course, it's much easier to blame the MT5 Tester than it is to learn the nuances of the MT5 Tester and trading ticks whatsoever.

If your system has negative expectancy(negative skew) in the long run it does not matter how systematic, low risk trader you are because the system works against you.

As professional traders frequently say, the problem is "your code."

Similarly, your problem is not "the system." It's your system. Please don't tell me that you're trying to blame the market now. If you're using variable position sizing, e.g., Kelly Criterion, etc., and it's failing, then that is simply part of the system that you designed.

William Roeder has already provided you with the resources needed to remedy a negative expectancy in Post #2. If you've seen that information posted elsewhere in the Forum, it's because your problem is not as "subtle" as you suggest.

I think this is why martingale strategies fail.

A lot of small wins, suddenly a crash in the graph.

I think this is why martingale strategies fail.

A lot of small wins, suddenly a crash in the graph.

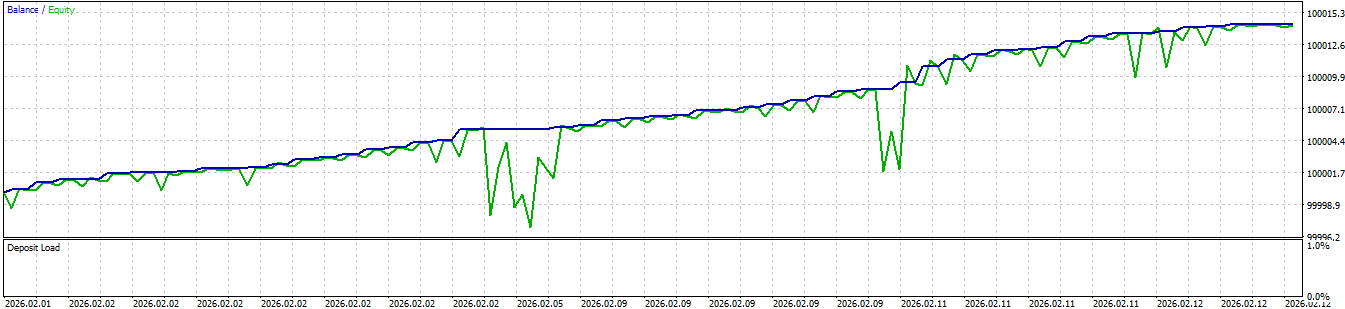

Also think that this type of graphs are an indicator for negative skew:

This is an easy way to visually spot problems. These unrealized equity losses are a warning signal. In those 2 situations the market eventually reversed in the trade direction but the danger of big losses was there. Next time the trader might not be lucky.

For an easy understanding of a positive skew and negative skew i will use the following visual representation.

You can see that a positive skew trading method has many small losses but limited in magnitude. Often this translates in low win rate, under 50% and small amount losses in % from the account balance. To the right is opened to big gains which will cover the losses and also will generate profits. A trading system with negative skew will do the opposite.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Hello.

I opened this topic because i see the that this subject it is less known and discussed among the traders.

To understand in simple terms what negative skew means i will define it: a trading system has negative skew when most of the time you make small profits but occasionally you take a very large loss.

Many trading systems show a smooth equity curve and high win rate but to achieve this they often use a large initial stop loss and an aggressive trail stop.

Statistically is well known that it comes a time when that big loss or series of big losses will happen and it is just a matter of time.

Every trader must know if his system used for trading has a positive or negative skew because ultimately his long term success depends on it.