GBPUSD Technical Analysis 2014, 21.12 - 28.12: Ranging Bearish with 1.5540 Key Resistance - Ready For Next Breakdown?

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.12.19 19:27

Forex Weekly Outlook December 22-26 (based on forexcrunch article)GDP data from Canada and the US, US Durable Goods Orders, New Home Sales, Unemployment claims, Haruhiko Kuroda’s speech are the major topics in Forex calendar. heck out these events on our weekly outlook.

Last week, Federal Reserve Chair Janet Yellen switched the phrase “considerable time” with the word “patience” in referral to rate hikes, at the FOMC press conference. The move was made to calm markets awaiting sharp policy shifts. Three Fed officials registered their dissent expressing discomfort with the Fed’s message. The Jobless claims came out better than expected with a drop to 289K, reaffirming US labor market’s strength. Philly Fed Manufacturing index came below expectations reaching 24.5 following the steep rise in November, still maintaining a positive score. New orders plunged from 35.7 to 15.7 and employment down from 22.4 to 7.2 points. Will the US economy continue to strengthen in 2015?

- Canadian GDP: Tuesday, 13:30. Canada’s economy expanded 0.4% in October after higher oil, gas and mining extraction, as well as manufacturing boosted growth. October’s reading was preceded by a 0.1% contraction in August. Since Canada is a major oil exporter, the Bank of Canada estimates that the slide in oil prices will reduce Canadian economic growth by 1/3 percentage points, somewhere between 2% and 2.5% in 2015. Poloz is also worried by household imbalances risking financial stability, leaving the door open for additional guidance in the future. Markets expect Canadian GDP to rise 0.1% in November.

- US Durable Goods Orders: Tuesday, 13:30. U.S. durable goods orders picked up in October beating expectations for a 0.4% fall. New orders rose by 0.4%, reaching $243.8 billion. Meanwhile, demand for manufactured goods, excluding transportation dropped 0.9% to $167.6 billion in October, after a 0.1% rise in the prior month. Analysts believe the decline suggests that business capital spending is weakening in Q4.The Fed expects GDP to slow to 2.5% in the fourth quarter. Long lasting product orders are expected to surge by 3%. While core orders are predicted to 3edge up 1.1%.

- US GDP: Tuesday, 13:30. On The second estimate of real gross domestic product for the third quarter of 2014 showed an annual rate increase of 3.9%, weaker than the 4.6% gain posted in the second quarter. However, this forecast was upwardly revised from the advance estimate of 3.5% released in October. Personal consumption expenditures and nonresidential fixed income investment increased more than expected, but export growth was slower than previously thought. The final GDP release for the third quarter is expected to reach 4.3%.

- New Home Sales: Tuesday, 15:00. Sales of new U.S. homes rose modestly in October, following a pickup in activity in the Midwest. New home sales increased 0.7% to a seasonally adjusted annual rate of 458,000. Economists expected a higher figure of 471,000. Sales of existing homes rose 1.5% in October to a seasonally adjusted annual rate of 5.26 million, adding another positive sign that the housing market is recovering. Analysts exdpect new home sales to reach 461,000 in November.

- US Unemployment Claims: Wednesday, 13:30. Fewer Americans filed claims for unemployment benefits last week, indicating increasing confidence among employers. The weekly unemployment claims dropped 6,000 to a seasonally adjusted 289,000, the lowest level since late October. The four-week average dropped 750 to 298,750. In the first 11 months of this year, employers have added 2.65 million jobs, posting the best hiring since 1999. The number of new claims is expected to reach 291,000 this week.

- Haruhiko Kuroda speaks: Thursday, 3:45. BOE Governor Haruhiko Kuroda speaks in Tokyo. Bank of Japan Governor Haruhiko Kuroda stated the bank will meet its 2% inflation target and continue to increasing base money, or cash and deposits at the bank, at an annual pace of 80 trillion yen ($674 billion). Kuroda said Japan’s economy continues to recover moderately after the tax hike effect subsides.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.12.23 09:12

Technical Analysis for USDJPY, GBPUSD and EURUSD (based on dailyfx article)

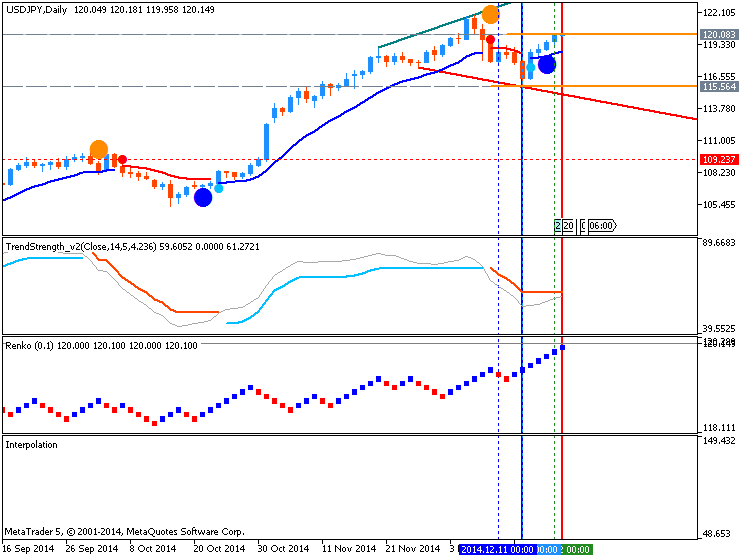

USDJPY

- USD/JPY has moved steadily higher over the past few days since finding support from just above the 38% retracement of the October low

- Our near-term trend bias is higher in USD/JPY while above 117.40

- A confluence of Gann and Fibonacci levels around 120.50 suggests this should be the next important action/reaction area

- A close back under 117.40 would turn us negative on the exchange rate

| Instrument | Support 2 | Support 1 | Spot | Resistance 1 | Resistance 2 |

|---|---|---|---|---|---|

| USD/JPY | 117.40 | 118.50 | 119.75 | 120.10 | 120.50 |

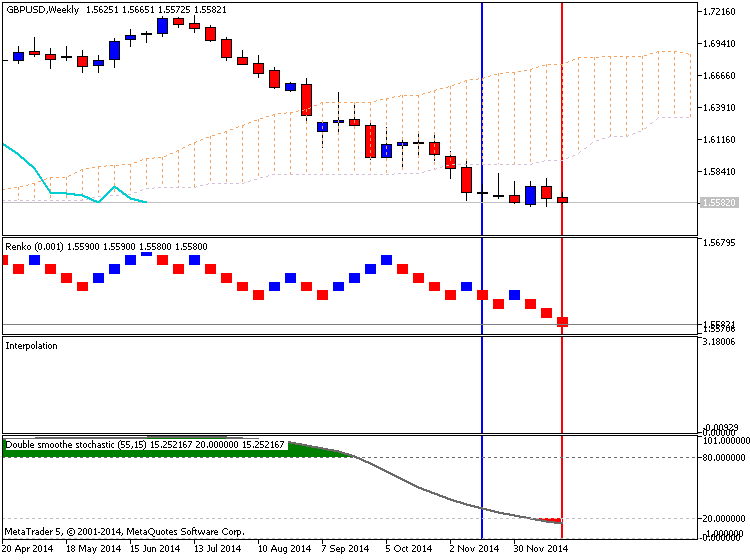

GBPUSD

- GBP/USD registered a new low for the year last week, but has since rallied back into the middle of the month-long range

- Our near-term trend bias is negative while below 1.5790

- A close under 1.5540 is needed to confirm the start of a more important leg lower

- A close over 1.5790 would turn us posiitve on Cable

| Instrument | Support 2 | Support 1 | Spot | Resistance 1 | Resistance 2 |

|---|---|---|---|---|---|

| GBP/USD | 1.5370 | 1.5540 | 1.5610 | 1.5675 | 1.5790 |

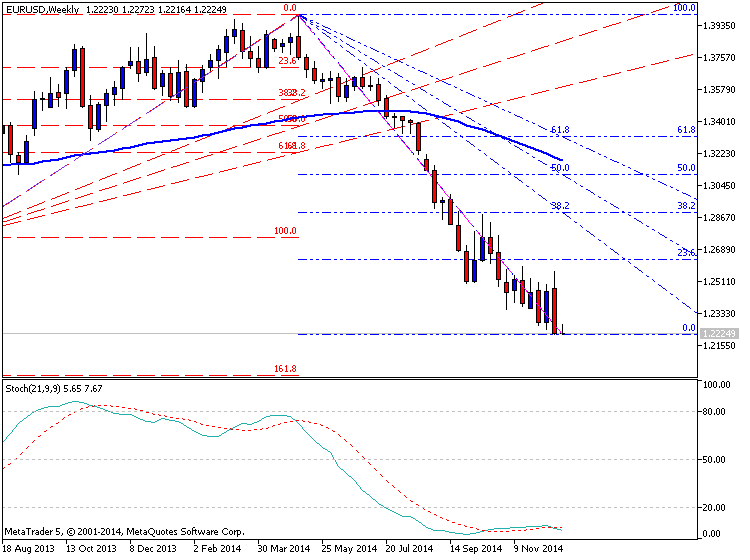

EURUSD

EUR/USD has managed to buck the historically positive seasonality of late December with aggressive weakness over the past few days taking the exchange rate to new lows for the year. The resumption of the broader trend has come earlier than we were expecting and has caught us a bit by surprise. We are now open to the possibility of a cyclical inversion early next year. Attention now turns to the next major downside pivot around 1.2135 as this marks the 50% retracement of the all-time low and the all-time high in the euro. Traction under this level in the weeks ahead would signal the start of a more important run lower in the exchange rate. A potential positive for the euro is the sentiment picture which saw the DSI fall to just 6% bulls on Friday. Extreme negative sentiment has accompanied every break to new lows over the past few months and warns too many traders are looking for the same thing. However, the next cyclical turn window of significance is not seen until closer to year-end.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.12.23 11:00

2014-12-23 09:30 GMT (or 11:30 MQ MT5 time) | [GBP - GDP]- past data is 3.2%

- forecast data is 3.0%

- actual data is 2.6% according to the latest press release

if actual > forecast (or actual data) = good for currency (for GDP in our case)

[GBP - GDP] = Change in the inflation-adjusted value of all goods and services produced by the economy. It's the broadest measure of economic activity and the primary gauge of the economy's health

==========

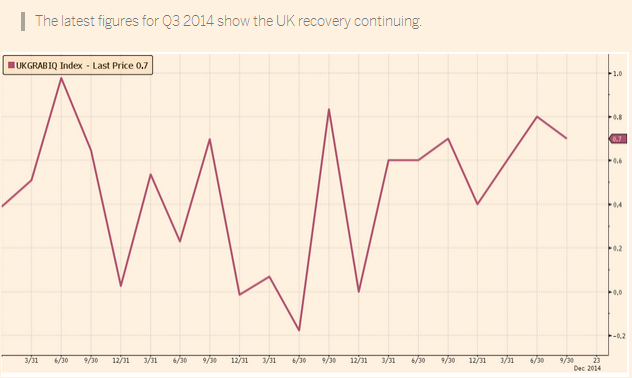

UK third quarter GDP growth confirmed at 0.7%

The UK's third-quarter economic growth has been finalised at 0.7 per cent, year-on-year, confirming the nation's status as one of the most rapidly growing advanced economies.

But the original year-on-year growth figure of 3 per cent was revised downward to 2.6 per cent, the Office for National Statistics said in its final version of the data.

The UK economy is rebounding as unemployment has declined to 6 per cent while pay rises are nudging ahead of low inflation. A supermarket price war and low fuel prices are encouraging consumer spending.

Meanwhile, low interest rates have spurred house price rises of 8 per cent or more, year-on-year, for 12 consecutive months, according to Nationwide.

MetaTrader Trading Platform Screenshots

MetaQuotes Software Corp., MetaTrader 5

GBPUSD M5: 37 pips price movement by GBP - GDP news event

Forum on trading, automated trading systems and testing trading strategies

Something Interesting in Financial Video December 2014

newdigital, 2014.12.24 15:18

Strategy Video: A Lesson for 2015 from Past Financial Crises (based on dailyfx article)

- Before financial market crises unfolder there is a steady erosion of the system's structure

- In 2008, an appetite for leverage and need for return led to implosion triggered by Bear Stearns

- The 1998 failure of Long Term Capital Management offers a similar story to the conditions we face today

Financial crises often explode from periods of exceptional market

performance and their appearance is usually catches the investing

community off guard. Yet, as dramatic as the market reactions may be;

these disruptive periods of rebalancing are not so obscure when the

underlying structural circumstances of the financial system are

accounted for. Back in 2008, the Great Financial Crisis was built upon

an appetite for excessive return and leverage through high finance. It

was, however, subprime and Bear Stearns' collapse that receives the

blame. Further back, 1998 draws a strong corollary to today's market

with an Asian financial crisis and Russian default leading to the

dramatic failure of Long Term Capital Management. Heading into 2015, we

have: excessive leverage; exposure to exceptionally risky assets; low

returns; a dependency on low volatility; and growing investor doubt. We

discuss the importance of appreciating a big-picture structural risk

heading into 2015.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.12.26 19:33

Forex Weekly Outlook Dec 29- Jan 2 ( based on forexcrunch article)We end 2014 with US CB Consumer Confidence and Unemployment Claims

and open 2015 with US ISM Manufacturing PMI. Join our weekly outlook

with the main market movers to impact Forex trading. Happy 2015!

Last week, the final revision to US GDP in Q3 came out better than

expected, crossing the 4% growth rate for the second consecutive

quarter. US economy expanded 5% between July and September, beating the

preliminary estimate of 3.9% and the median forecast of 4.3%. The

strong expansion indicates the US economy will close 2014 on a strong

note. More positive data was released from the US labor market with a

continued decline in the number of initial unemployment claims, noting

the US job market continues to improve with increased hiring and fewer

dismissals. Will the US economy continue to expand in 2015?

- US CB Consumer Confidence: Tuesday, 15:00. U.S. consumer confidence declined in November to a five month low of 88.7 after posting 94.5 in October. Consumer’s confidence regarding current-business conditions and short-term outlook dropped considerably. Analysts expected confidence to rise to 95.9. Economists expect consumer sentiment will reach 94.6 in December.

- US Unemployment Claims: Wednesday, 13:30. The number of new applications for unemployment benefits declined last week to its lowest level since early November, indicating the job market continues to demonstrate strength. Initial jobless claims dropped by 9,000 to a seasonally adjusted 280,000. Economists expected claims to reach 290,000. The less volatile four-week moving average fell 8,500 to 290,250 indicating companies seek to hold on to their workers and hire new ones. The number of weekly claims is expected to reach 287,000 this week.

- US ISM Manufacturing PMI: Friday, 15:00. The U.S. manufacturing sector lost momentum in November, reaching 58.7 after a 59 points reading in the prior month. Economists expected a lower figure of 57.9. New Orders Index increased to 66, from October’s reading of 65.8; the Production Index reached 64.4%, down from the previous reading of 64.8; and the Employment Index declined to 54.9, compared to the precious reading of 55.5. Lower energy prices gave a boost to the manufacturing sector, increasing consumer’s demand and the continued strength of the Us labor market also contributes to growth. Manufacturing PMI is forested to reach 57.6 this time.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

D1 price is on primary bearish market condition with secondary ranging:

W1 price is on primary bearish market condition with 1.5540 support level.

MN price is on bearish breakdown by breaking 1.5589 support level with Chinkou Span line of Ichimoku indicator crossed the price from above to below on close W1 bar.

If D1 price will break 1.5540 support level so the primary bearish breadown will be continuing

If D1 price will break 1.5785 resistance level so the market rally will be started with possible reversal to bullish condition

If not so we may see the ranging within bearish market condition.

UPCOMING EVENTS (high/medium impacted news events which may be affected on GBPUSD price movement for this coming week)

2014-12-22 15:00 GMT (or 17:00 MQ MT5 time) | [USD - Existing Home Sales]

2014-12-23 09:30 GMT (or 11:30 MQ MT5 time) | [GBP - Current Account]

2014-12-23 13:30 GMT (or 15:30 MQ MT5 time) | [USD - GDP]

2014-12-23 15:00 GMT (or 17:00 MQ MT5 time) | [USD - New Home Sales]

2014-12-24 13:30 GMT (or 15:30 MQ MT5 time) | [USD - Unemployment Claims]

Please note : some US (and CNY) high/medium impacted news events (incl speeches) are also affected on GBPUSD price movement

SUMMARY : bearish

TREND : ranging