Very low quality historical data issue of broker!

On live account with MT5 while running EA tests I should be able to access all historical data on the server with "99% quality" as soon as the broker connects to the trading server. (At least I know it is.)

I have reported the problem to my broker and have yet to receive a response. I suspect I missed an important detail about this that I should know or do in MT5.

I would be glad if you share your experience and suggestions about the quality ratios of historical data obtained from your live servers while performing backtests (?)

Best.

Don't overestimate this percentage. In MT4 it can be written by a program providing test quotes. In MT5 (I think and don't know for sure) it depends on what you have selected: every tick, 1 min OHLC, only open,....

If you are not sure about the quotes check for holes. On the other hand if your EA is able to manage holes or interruptions it is more robust.

Don't overestimate this percentage. In MT4 it can be written by a program providing test quotes. In MT5 (I think and don't know for sure) it depends on what you have selected: every tick, 1 min OHLC, only open,....

If you are not sure about the quotes check for holes. On the other hand if your EA is able to manage holes or interruptions it is more robust.

Don't underestimate it !

It doesn't depends of the selected mode (EDIT: it should not) and only means a very poor history data which should not be used at all for serious backtests.

Testing and debugging, or having a robust EA is something else entirely.

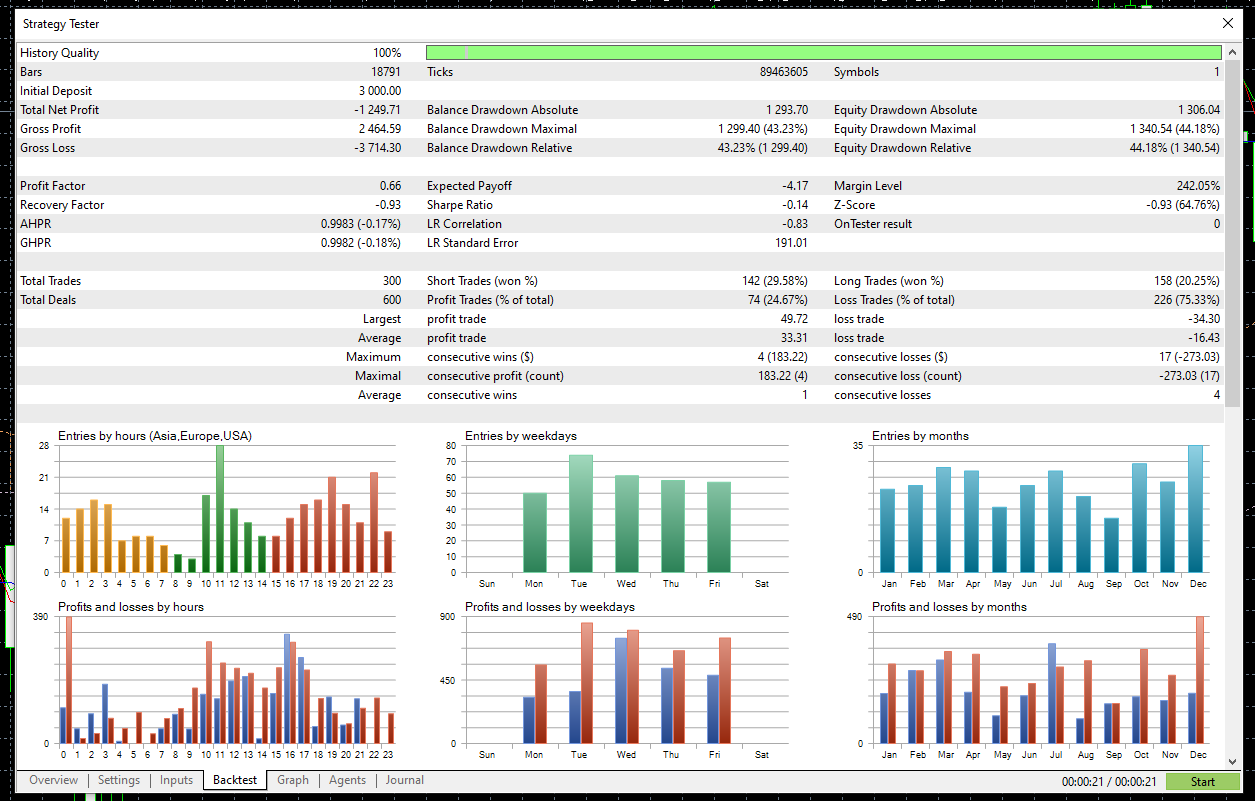

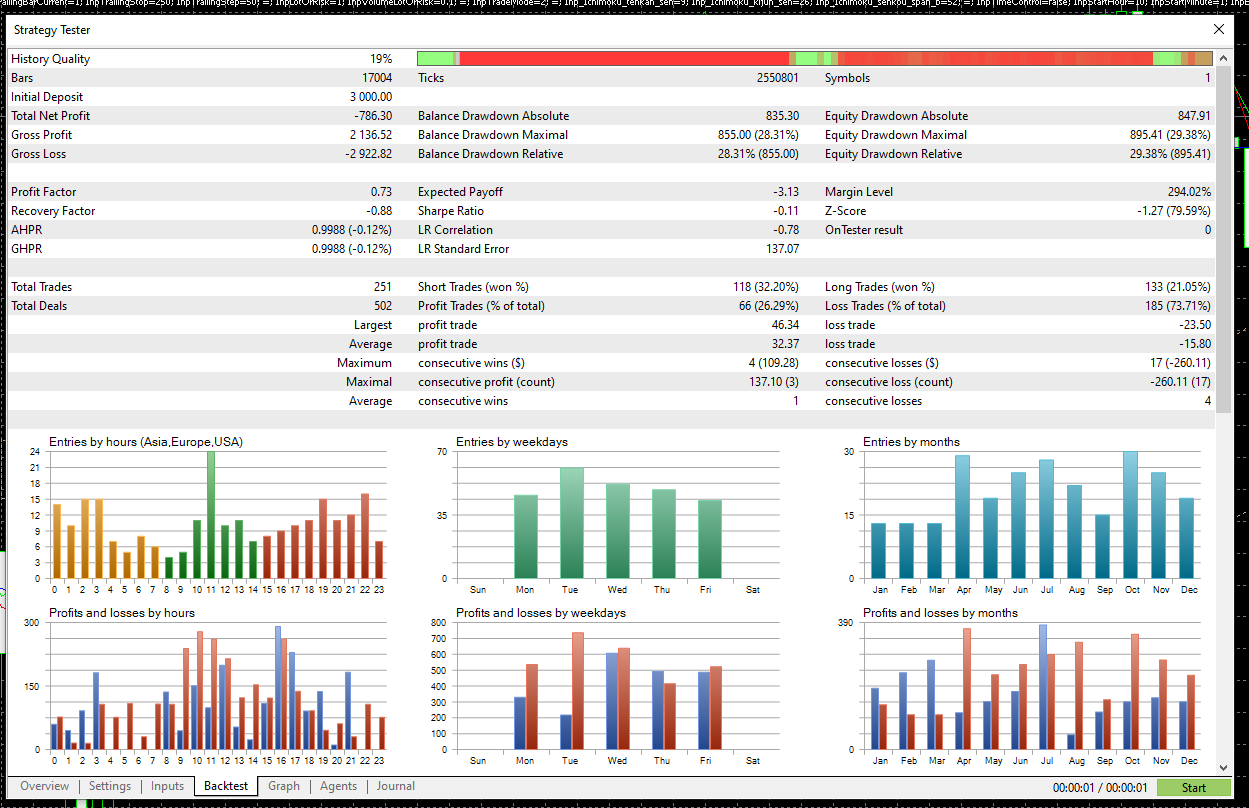

But when I do the same test with "1 minute OHCL", the quality drops to 19%.

I think the historical data presented in the broker is in tick data format, not "M1" format.

Never use broker data.

Import data with Tickstory or similar. (Google for it)

Never use broker data.

Import data with Tickstory or similar. (Google for it)

Import data with Tickstory or similar. (Google for it)

I think @Bernhard Schweigert meant to find in Google more information about this topic

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

On live account with MT5 while running EA tests I should be able to access all historical data on the server with "99% quality" as soon as the broker connects to the trading server. (At least I know it is.)

I have reported the problem to my broker and have yet to receive a response. I suspect I missed an important detail about this that I should know or do in MT5.

I would be glad if you share your experience and suggestions about the quality ratios of historical data obtained from your live servers while performing backtests (?)

Best.