How is missing data treated in MT5 Strategy Tester?

Hi,

I am currently Investigation the data Quality used in the Strategy Tester.

Therefore, I was wondering how the Tester treats missing data. For instance, let's say, for one month we have only tick data for 4 fictive time Points in H1 (not quite realistic but for the case of demonstration):

1. 2018.01.01 - 03:04:52

2. 2018.01.06 - 06:03:41

3. 2018.01.20 - 01:01:13

4. 2018.01.27 - 04:23:57

What happens in the backtest now? Is the Tester interpolating between the timepoints or does it just create 4 bars placing it next to each other?

Thanks for your Input!

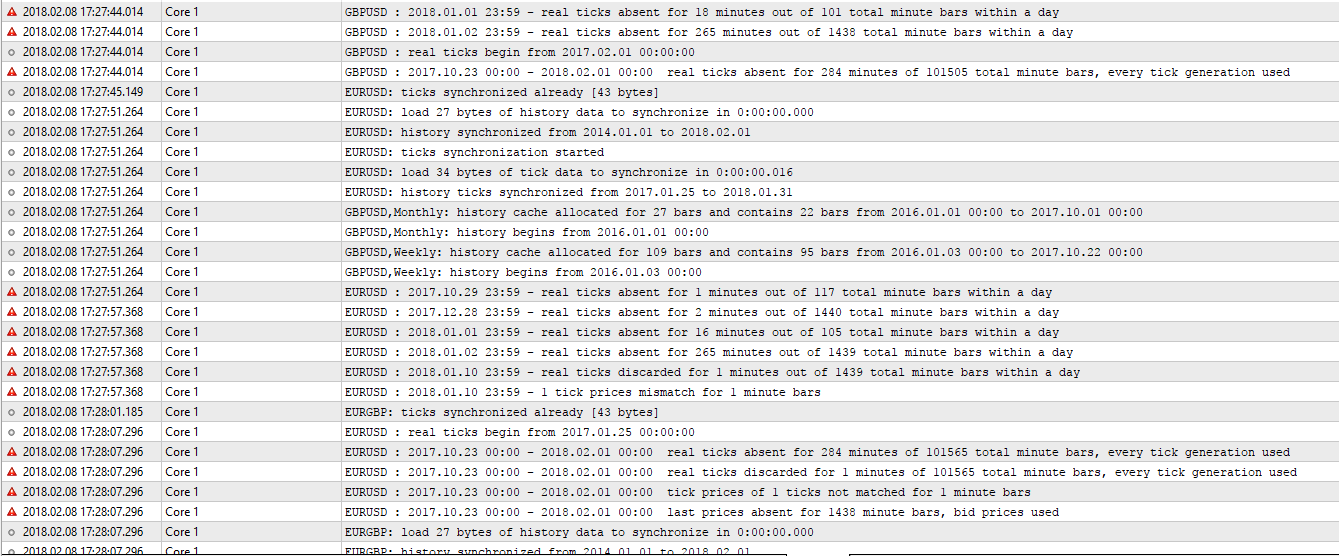

You can check the journal to see how the data is treated.

When the test is started, data is downloaded, sycnhronized and corrected for missing data. The journal states what has been done to the data.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

Hi,

I am currently Investigation the data Quality used in the Strategy Tester.

Therefore, I was wondering how the Tester treats missing data. For instance, let's say, for one month we have only tick data for 4 fictive time Points in H1 (not quite realistic but for the case of demonstration):

1. 2018.01.01 - 03:04:52

2. 2018.01.06 - 06:03:41

3. 2018.01.20 - 01:01:13

4. 2018.01.27 - 04:23:57

What happens in the backtest now? Is the Tester interpolating between the timepoints or does it just create 4 bars placing it next to each other?

Thanks for your Input!