Discussing the article: "Swing Extremes and Pullbacks (Part 4): Dynamic Pullback Depth Using Volatility Models"

Very nice article!!! Congratulations!!!

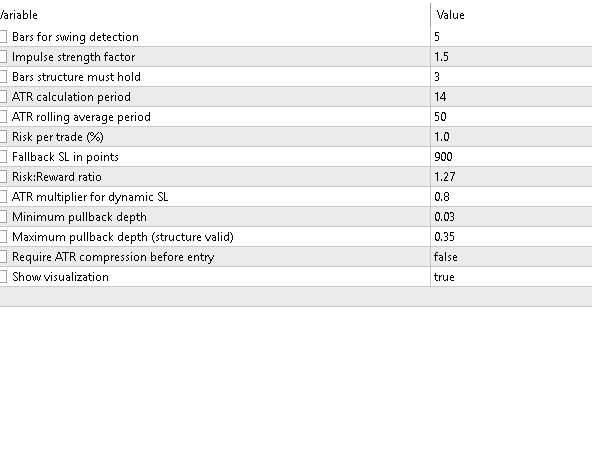

The version published on Mql5 site doesn't open trades and it has not the same params as the article.

You are missing trading opportunities:

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration

Log in

You agree to website policy and terms of use

If you do not have an account, please register

Check out the new article: Swing Extremes and Pullbacks (Part 4): Dynamic Pullback Depth Using Volatility Models.

This article replaces binary swing validation with a volatility‑normalized pullback model. Retracement depth is measured as a ratio of the prior impulse and calibrated to a rolling ATR regime, while entries require a minimum quality score and confirmation by structure or liquidity signals. The five‑layer design integrates detection, validation, liquidity mapping, regime‑aware scoring, and execution, helping you filter weak corrections and size stops dynamically to current conditions.

The EA detects swing highs and lows using a lookback window. Each candidate undergoes multiple validation checks, including a structure break (new high or low), candle size displacement, liquidity sweep, and time-based respect. Valid swings form the foundation for market structure and liquidity zone mapping. A state machine then classifies the market as accumulation, expansion, distribution, or reversal based on swing progression and sweep failures.

How Mapping Market Architecture goes about:

Author: Hlomohang John Borotho