NZDUSD Technical Analysis 2014, 08.06 - 15.06: Moving along Kumo

I agree completely, there is a bearish trend for 4 week

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.06.07 11:07

Forex Weekly Fundamentals - Outlook June 9-13Rate decision in New Zealand and Japan, employment data in the UK, Australia and the US and US retail sales are the highlights of this week. Here is an outlook on the main market-movers coming our way.

Last week, US Non-Farm Payrolls showed a 217K gain in jobs in May reinforcing estimates that the five-year-long recovery has accelerated this spring. April’s jobs addition was the best in more than two years. Meanwhile the unemployment rate remained unchanged at 6.3% in May, matching the lowest level since September 2008. Analysts expected a lower job addition of 214,000 and a higher unemployment rate of 6.4%. May’s advance tops the average monthly gain of about 200,000 during the past year. Will this positive trend continue?

- UK employment data: Wednesday, 8:30. U.K. jobless claims declined less-than-expected in April, down 25,100 from 30,600 in the previous month while economists expected a contraction of 30,700 claims. However the rate of unemployment declined to 6.8% in the three months to March from 6.9% in the three months to February, in line with market forecast. The average earnings increased by a seasonally adjusted 1.7% in the three months to March, the same as in the prior three months, lower than the 2.1% rise expected. The number of unemployed is expected to decline further by 25,000 and the unemployment rate is expected to decline to 6.7%.

- US Federal Budget Balance: Wednesday, 18:00. The US government posted a large $106.9 billion surplus in April, lowering deficit to $305.8 billion for a dramatic 37% improvement from this time last year. Receipts were on the rise led by a11% fiscal year-to-date increase in corporate taxes and a 7% increase in individual taxes. The rate of improvement indicates a positive trend of deficit contraction. Us Federal budget is predicted to show a 142.8billion deficit this time.

- NZ rate decision: Wednesday, 21:00. Governor of the Reserve Bank of New Zealand, Graeme Wheeler decided to raise rates by 25 basis points to 3.0% in April in light of positive growth in New Zealand’s economic activity. The rate hike was in line with market forecast. Prices for New Zealand’s export commodities remain very high, despite a 20% drop in auction prices for dairy products in recent months. Domestically, the long period of low interest rates and the strong expansion in the construction sector led to strong recovery. The RBNZ is expected to increase rates once more by 0.25% to 3.25%.

- Australian employment data: Thursday, 1:30. Australia’s unemployment rate remained steady at 5.8% in April, amid positive signs of recovery in the labor market. The number of people employed increased by 14,200 to 11.57 million in April. Full-time employment edged up 14,200 to 8.05 million during the period. Part-time employment remained unchanged at 3.53 million. If the rate of improvement continues, the RBA may have to consider raising rates. Australian job addition is expected to reach 10,300, while the unemployment rate is expected to grow to 5.9%.

- US retail sales: Thursday, 12:30. U.S. retail sales were slow in April after strong gains posted in the previous two months, but the overall growth trend for the second quarter remains robust. Retail sales edged up 0.1% affected by declines in receipts at furniture, electronics and appliance stores, restaurants and bars and online retailers. Retail sales edged up 1.5% in March after a 1.1% advance in February following stagnation during the cold winter season. April’s low reading may reflect growing caution amid consumers waiting to confirm economic recovery. Meanwhile, Core sales, excluding automobiles, remained unchanged in April after advancing 1.0% in March, much lower than the 0.6% rise anticipated by analysts. U.S. retail sales are expected to grow by 0.5% , while core sales are predicted to gain 0.4%.

- US unemployment claims: Thursday, 12:30. The number of US jobless claims rose last week to 312,000 from 304,000 in the prior week, but the general trend continues to point to a strong labor market. Analysts expected a smaller increase to 309,000. The four-week average fell 2,250 to 310,250, the lowest level since June 2007. Even if job growth slows in May as expected, economists say it should not be viewed as a loss of momentum in the labor market and the economy as payrolls would still be above the average for the preceding six months. US jobless claims are expected to reach 306,000 this week.

- Stephen Poloz speaks: Thursday, 15:15.BOC Governor Stephen Poloz will speak in Ottawa. Market volatility is expected.

- Mark Carney speaks: Thursday, 22:00.BOE Governor Mark Carneywill speak in London. Carney may talk about the BOE’s latest rate decision and the reasons for maintaining monetary policy in June. Volatility is expected.

- Japan rate decision: Friday. The Bank of Japan maintained rates in May, renewing their commitment to boost monetary base by 60-70 trillion yen per year. The bank statement said Japan’s economy is progressing according to forecasts and capital spending is expected to advance in the coming weeks. Exports are stable and will remain unchanged according to the forecast. No change in rates is exected.

- US PPI: Friday, 12:30. The prices that U.S. finished goods increased 0.6% in April, following a 0.5% rise in March indicating a rising inflation trend. The reading was above market forecast of a 0.2% increase. The increase was led by higher food prices and greater retailer and wholesaler profit margins. On a yearly base, producer prices increased 2.1%, the biggest rise in more than two years. US producer prices are expected to gain 0.1% this time.

- US Prelim UoM Consumer Sentiment: Friday, 13:55. US consumer sentiment declined to 81.8 and in May from 84.1 in April mainly due to lower rating in the current conditions index, down to 95.1 from 98.7 in April. Analysts expected the index to rise to 84.7. The outlook component also slipped to 73.2 from 74.7. However, overall data indicates consumer sentiment continues to its positive trend despite recent financial market volatility. US consumer moral is expected to rise to 83.2.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.06.09 12:12

NZD/USD Fundamental Analysis June 10, 2014 Forecast

The NZD/USD gained 17 points to trade at 0.8517 moving towards the top of its trading range climbing steadily after the roll out of ECB big guns, which should benefit the commodity currencies. The addition of stimulus supports small nations and emerging nations by increasing money flow and also demands for exports to fuel growth. Over the weekend Chinese trade data was released showing a surge in exports but a drop in imports. The main focus this week will be the RBNZ where governor Graeme Wheeler is expected to hike the official cash rate a quarter point to 3.25 percent this Thursday and traders are mulling whether he will soften his projection for future rate rises given recent weakness in milk prices, and labour and inflation data. Still, many say the market has gone too far in pulling back expectations for future hikes by 65 basis points over three years, given the strength of the local economy which is underpinned by strong migration and government spending.

“The Reserve Bank should surprise to the upside because markets have priced in too much of a downgrade to the OCR track,” said Imre Speizer, senior market strategist at Westpac Banking Corp. “We think that the Reserve Bank will revise its track down a little but we are only talking in the order of 10 basis points, not in the order of 65. The market is basically saying they will take the equivalent of two full hikes out of the multi-year tightening programme. We don’t agree with that. We think that they will just take a little bit out and as a result the markets will then be disappointed at the failure of the Reserve Bank to endorse its pricing and interest rates then will need to bounce on the day and that will push the kiwi/US higher.”

The US dollar remains strong trading at 80.44 to start out the week after a smart release of US nonfarm payroll data on Friday. The US economy might have contracted in the first quarter but it has rebounded quickly, with non-farm payrolls posting its strongest four-month period in two years.

Non-farm payrolls rose by 217,000 in May, consistent with expectations, following solid gains since February. Job creation in April was revised down to 282,000 (from 288,000).

This was the first time in 14 years that non-farm payrolls rose by 200,000 in four consecutive months and it was the strongest four-month gain since April 2012. To put this in perspective there have been just three four-month periods with this level of job creation in the past eight years.

Upcoming Economic Events that affect the AUD, NZD, JPY and USD:

Date | Currency | Event | Forecast | Previous |

|---|---|---|---|---|

Jun. 10 | AUD | 0.2% | -0.9% | |

| AUD | 6 | ||

| CNY | Chinese CPI (YoY) | 2.4% | 1.8% |

| CNY | Chinese PPI (YoY) | -1.5% | -2.0% |

| CNY | Chinese CPI (MoM) | -0.1% | -0.3% |

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.06.08 09:59

NZD/USD forecast for the week of June 9, 2014, Technical AnalysisThe NZD/USD pair went back and forth during the course of the week, basically finishing unchanged. Because of this, a longer-term trader can look at this large range and place a trade based upon which direction we break. Ultimately though, we do feel more comfortable buying a break above the top of the candle, and going long. There is quite a bit of noise underneath this area, and as a result we feel that selling could be a bit more difficult. Nonetheless, we will simply follow where the market leads us.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.06.08 15:36

Forex Fundamentals - Weekly outlook: June 9 - 13The dollar pushed higher against the other major currencies on Friday after the nonfarm payrolls report for May indicated that the U.S. labor market is continuing to gradually improve.

The Department of Labor reported that the U.S. economy added 217,000 jobs last month, just under expectations for jobs growth of 218,000, while April's figure was revised to 282,000. The unemployment rate remained steady at a five-and-a-half year low of 6.3%.

EUR/USD initially touched a two-week high of 1.3677 following the release of the data, before pulling back to 1.3642 late Friday. For the week, the pair was 0.34% higher.

The U.S. jobs report came one day after the European Central Bank unveiled a package of measures to avert the threat of persistently low inflation in the euro area, briefly sending the single currency to four month lows of 1.3502 against the dollar, before later erasing the day’s losses.

The ECB cut the main refinancing rate in the euro area to a record low 0.15% and imposed negative deposit rates on commercial lenders, in a bid to stimulate lending to businesses.

The bank also implemented a new Long-Term Refinancing Operation, designed to help banks lend to small companies and said it would "intensify" its preparatory work on the 'asset-backed security' market.

The ECB acted after a report showed that the annual rate of inflation in the euro zone slowed to 0.5% in May, far below the ECB’s target of close to but just under 2%.

The dollar inched higher against the yen on Friday, with USD/JPY at 102.47 at the close of trade, recovering from session lows of 102.12 struck immediately after the jobs data was released.

The dollar was also higher against the pound and the Swiss franc, with GBP/USD slipping 0.11% to 1.6801 and USD/CHF rising 0.24% to 0.8933.

Elsewhere Friday, the Canadian dollar ended slightly lower against the U.S. dollar following the release of a lackluster domestic jobs report.

Statistics Canada reported that the economy added 25,800 jobs in May, above expectations for 25,000, but gains were due to the creation of part time positions, while the unemployment rate ticked up to 7.0% from 6.9% in April.

USD/CAD touched highs of 1.0948 before settling at 1.0931 late Friday.

In the week ahead, investors will be looking ahead to Thursday’s U.S. retail sales report for further indications on the strength of the economic recovery. A rate review by New Zealand’s central bank and the latest U.K. jobs report will also be in focus.

Monday, June 9

- Markets in Australia are to remain closed for a national holiday.

- Japan is to release revised data on first quarter growth, as well as reports on the current account and bank lending.

- Canada is to publish data on housing starts.

- Japan is to release data on tertiary industry activity.

- Australia is to publish private sector data on business confidence, as well as official data on home loans.

- China is to produce data on consumer and producer prices.

- In the euro zone, France is to publish data on industrial production. Elsewhere in Europe, Switzerland is to release data on retail sales, the government measure of consumer spending, which accounts for the majority of overall economic activity.

- The U.K. is to release data on industrial and manufacturing production.

- Japan is to publish the latest reading of its BSI manufacturing index.

- Australia is to release private sector data on consumer sentiment.

- The U.K. is to publish data on the change in the number of people employed and the unemployment rate, as well as data on average earnings.

- The Reserve Bank of New Zealand is to announce its benchmark interest rate and publish its rate statement, which outlines economic conditions and the factors affecting the monetary policy decision. The bank is also to hold a press conference to discuss the monetary policy decision.

- Japan is to produce data on core machinery orders.

- Australia is to release data on the change in the number of people employed and the unemployment rate, and a private sector report on inflation expectations.

- The euro zone is to release data on industrial production, while the ECB is to publish its monthly bulletin.

- Canada is to publish data on new house price inflation, while Bank of Canada Governor Stephen Poloz is to speak at an event in Ottawa.

- The U.S. is to release the weekly report on initial jobless claims, in addition to data on retail sales and import prices.

- BoE Governor Mark Carney is to speak at an event in London.

- New Zealand is to release private sector data on manufacturing activity.

- The Bank of Japan is to announce its benchmark interest rate and publish its monetary policy statement, which outlines economic conditions and the factors affecting the bank’s decision. The announcement is to be followed by a press conference.

- China is to release data on industrial production and fixed asset investment.

- Canada is to publish data on manufacturing sales.

- The U.S. is to round up the week with data on producer price inflation and preliminary data on consumer sentiment from the University of Michigan.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.06.10 13:40

NZDUSD - Sell The Rumour, Buy The Fact?

- I expect sideways trading until the rate decision and for 25bps will be added to bring rates to 3.25%

- This should see NZDUSD break up through 0.852 and target 0.864 and eventually 0.87 highs

- Fundamentally still strong, I do not expect 'jaw-boning' from RBNZ and for NZDUSD to become bullish after Thursday

- Talk of intervention to bring down NZD would have more bearish impact upon NZD than not raising rates

- 0.840 is a pivotal swing low and for NZDUSD to return to the bullish trend

Despite the fact RBNZ are paying the highest interest rates among G10 currencies traders have continued to short NZD when RBNZ hinted the rate hikes may not be aggressive as previously thought. They also talked of potential intervention by shorting NZD if the overpriced Kiwi Dollar remains among poor fundamental data. Price has been within a steady downtrend for the past month until price reached 0.840.

0.840 is a key level of support which was successfully defended following last Thursday's' ECB meeting, and the Greenback sell-off. NZDUSD posted its single largest day gain since March '14, respecting the 200-day eMA and closing the week with a Spinning Top Doji to warn of a weakness the sell-off from the May Highs.

Friday and Monday produced 2 failed attempts to break above 0.8517

resistance, however price continues to hover around the 0.850 handle and

I expect this sideways trading to continue leading up to the release.

If we do break above 0.8520 then we have resistance close by around 0.857 which I expect to hold upon first attempt, so ideally we will see basing patterns above 0.850 and for buying pressure to increase whilst the trend is established.

COUNTER-BIAS

A break below this week's range should target 0.843 and 0.840, with a break below 0.840 being quite bearish for the Kiwi and for losses to gain momentum. For this scenario we would have to keep rates fixed at 3% and for NZD to strengthen talk of intervention.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.06.08 16:19

NZD/USD Fundamentals - weekly outlook: June 9 - 13The New Zealand dollar rose to a seven-day high against its U.S. counterpart on Friday, before paring gains to end little changed after the closely-watched U.S. nonfarm payrolls report for May yielded no surprises.

NZD/USD hit 0.8554 on Friday, the pair’s highest since May 28, before subsequently consolidating at 0.8500 by close of trade on Friday, up 0.01% for the day and flat for the week.

The pair is likely to find support at 0.8420, the low from June 5 and resistance at 0.8554, the high from June 6.

The Department of Labor said Friday that the U.S. economy added 217,000 jobs last month, just under expectations for jobs growth of 218,000. The unemployment rate remained steady at a five-and-a-half year low of 6.3%.

The data disappointed some market expectations for a more robust reading but indicated that the U.S. economy continued to shake off the effects of a weather-related slowdown over the winter, bolstering the outlook for the broader economic recovery.

The kiwi rallied along with other risk-sensitive assets on Thursday after the European Central Bank unveiled a package of measures to avert the threat of persistently low inflation in the euro area.

The ECB cut the main refinancing rate in the euro area to a record low 0.15% and imposed negative deposit rates on commercial lenders, in a bid to stimulate lending to businesses.

Data from the Commodities Futures Trading Commission released Friday showed that speculators modestly decreased their bullish bets on the New Zealand dollar in the week ending June 3.

Net longs totaled 17,531 contracts as of last week, compared to net longs of 17,994 contracts in the previous week.

In the week ahead, investors will be looking ahead to Thursday’s U.S. retail sales report for May for further indications on the strength of the economic recovery.

The outcome of a monetary policy meeting by the Reserve Bank of New Zealand will also be in focus.

Tuesday, June 10

- China is to produce data on consumer and producer prices. The Asian nation is New Zealand’s second-largest trade partner.

- The Reserve Bank of New Zealand is to announce its benchmark interest rate and publish its rate statement, which outlines economic conditions and the factors affecting the monetary policy decision.

- The central bank is also to hold a press conference to discuss the monetary policy decision.

- Later in the day, the U.S. is to release the weekly report on initial jobless claims, in addition to data on retail sales and import prices.

- New Zealand is to release private sector data on manufacturing activity.

- China is to release data on industrial production and fixed asset investment.

- The U.S. is to round up the week with data on producer price inflation and preliminary data on consumer sentiment from the University of Michigan.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.06.12 09:59

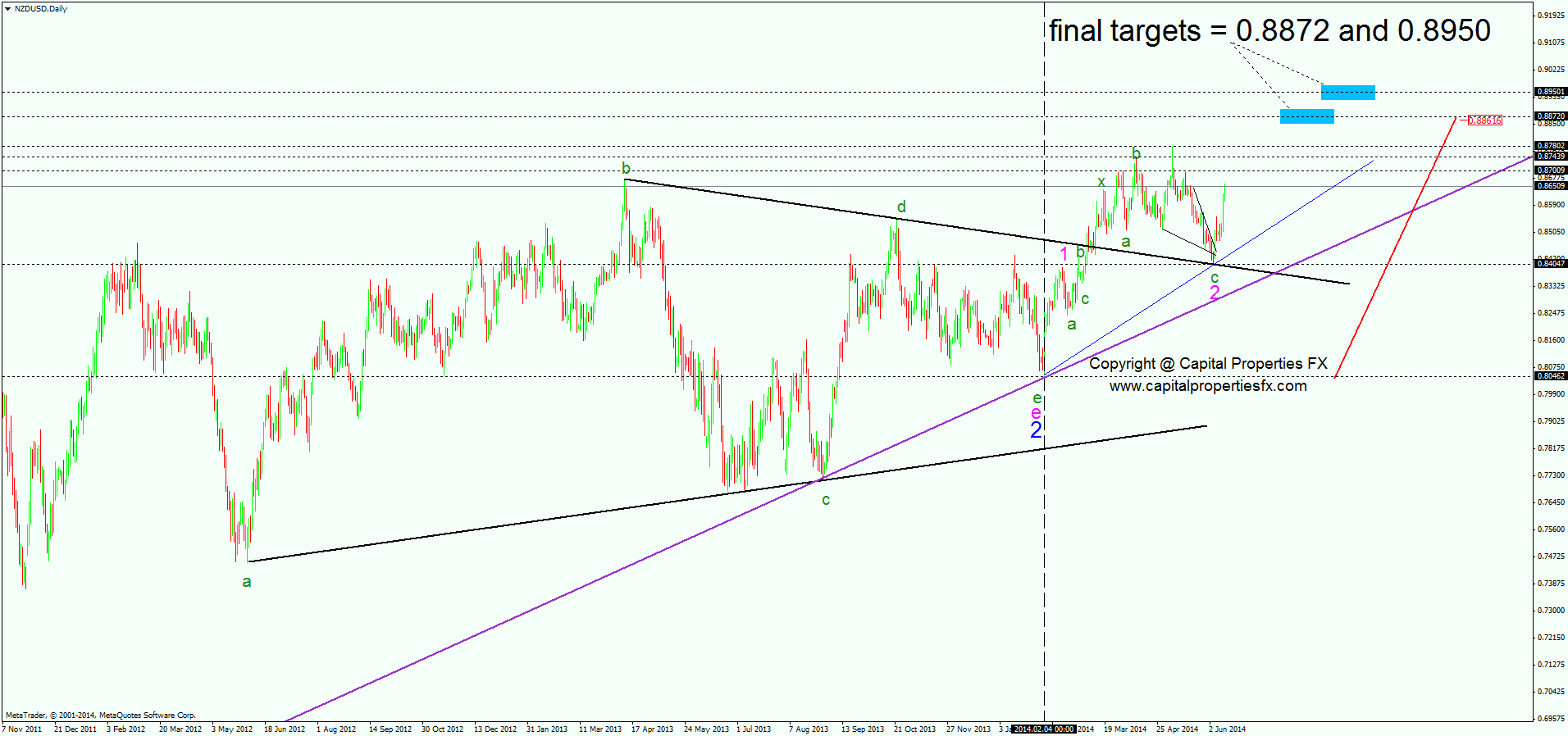

Top Trade Idea For June 12th, 2014 – NZDUSD

In light of the recent RBNZ interest rate decision and looking at how the kiwi pairs reacted to the rate hike down under, I would like to focus on the nzdusd today and to made a case about why the pair is not going to stop anywhere around these levels and why it should attack the all important 0.90 area.

Yes, I know we are only in the 0.8650 and recent highs are still holding but the pattern above on the daily chart is a contracting triangle that broke higher somewhere in February this year, price made an impulsive move, or a five waves structure if you want for wave 1 pink in the chart above and then for the second wave it made a complex correction, namely a double running flat.

The second flat pattern there kissed the broken now b-d trend line, like a good bye kiss, and then price exploded.

But the info above is only one side of the bullishness on the pair. The bigger degree triangle you are seeing there has a measured move, the so called thrust of a triangle and this one points minimum to, well, 0.8872 to come.

The 0.8950 target is given by the fact that the double three running pattern on the bigger degree charts is always being followed by a third wave extension, and it means now we are looking for a 3rd wave pink that should be bigger than 161.8% when compared with the value of wave 1 pink. Minimum.

That gives us 0.8938 for the extension and I will book profits in that area, up to 0.8950. Why? Well, we want to avoid the classical behavior markets make around psychological level (check recent failures eurusd and gbpusd did at almost 1.40 and 1.70).

And all this should happened while price stays above the blue line in the chart above, as piercing that line will invalidate the whole pattern.

Forum on trading, automated trading systems and testing trading strategies

newdigital, 2014.06.13 07:01

2014-06-12 12:30 GMT (or 14:30 MQ MT5 time) | [USD - Retail Sales]

---

U.S. Retail Sales in May Grow Slower than Estimated

The US Commerce Department reported on Thursday that retail sales in May

rose 0.3 percent, much lower than analysts’ estimate of 0.6 percent

gain and April’s revised 0.5 percent growth.

“The continued gains during the first two months of the second quarter suggests that consumers are continuing to hold their side of the bargain, building on the strong momentum at the end of the last quarter,” Millan Mulraine, a New York-based deputy chief economist at TD Securities, told Reuters.

Separately, the Labor Department announced that initial applications for

unemployment insurance rose 4,000 to 317,000 in the week through June

7. Nonetheless, recent data shows that the US labor market continues to

improve steadily.

Employers in the country absorbed 217,000 new workers

in May, marking the fourth straight month that the figure has stayed

above 200,000. This has seen all the 8.7 million jobs that were shed in

the financial recession recouped back.

Most analysts expect the economic growth in the second quarter to

range from 3 percent to 4 percent, riding on the back of the resurgent

services and manufacturing sectors. The economy posted a 1 percent

decline in the first quarter owing to the harsh winter weather.

Another data released by the Commerce Department on Wednesday showed

that business inventories grew the most in the six months through April.

The core retail sales, which are adjusted for food, gasoline,

automobiles and building materials, remained unchanged in May. The

figures in April were readjusted to show an increase of 0.2 percent as

opposed to the earlier estimate of a 0.1 percent decline.

- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

You agree to website policy and terms of use

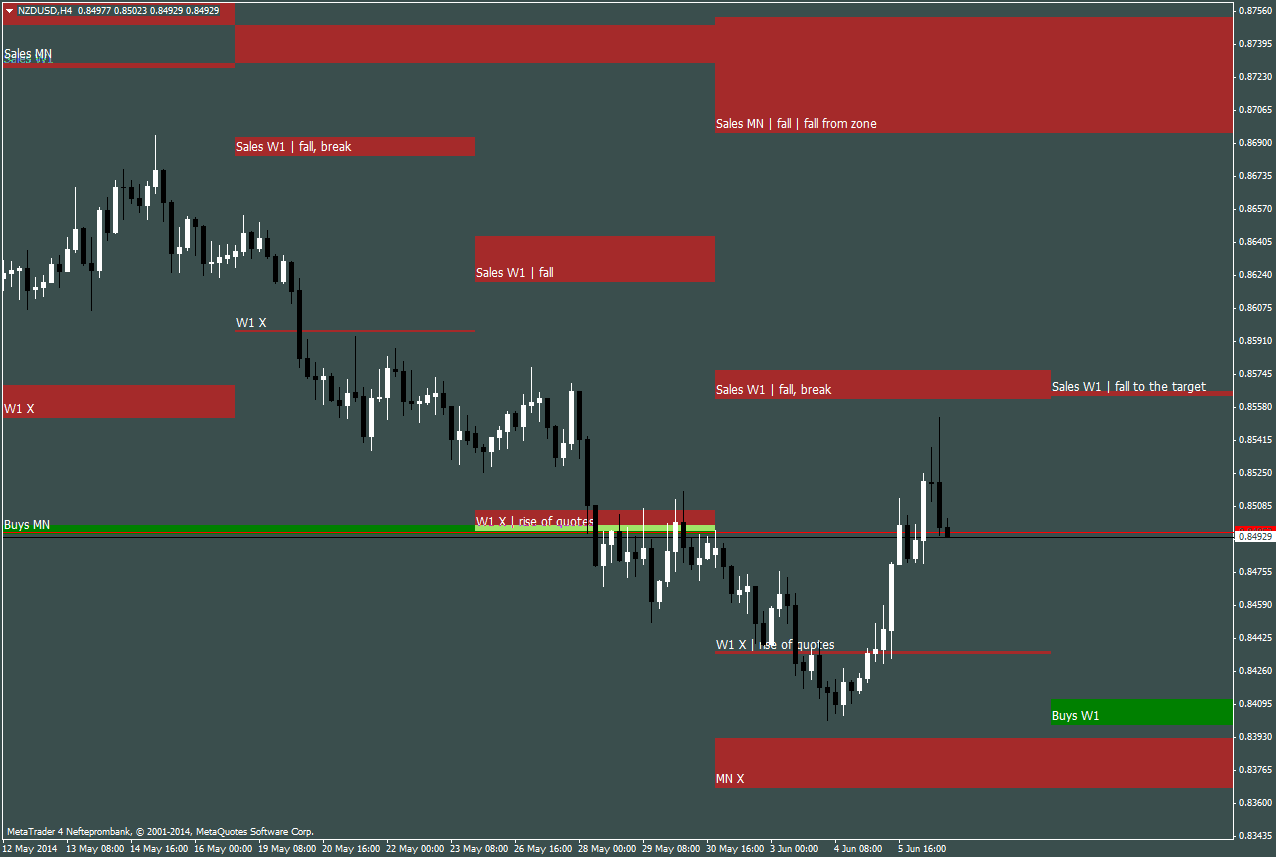

D1 price is moving along the border of Ichimoku cloud/kumo (Sinkou Span B line) for market rally within primary bearish condition.

H4 price is moving along the border of Ichimoku cloud/kumo as well trying to be reversed from primary bearish to primary bullish market condition.

W1 price is on bullish ranging between 0.8450 support and 0.8779 resistance levels.

If D1 price will break 0.8515 so we may see the ranging market condition within primary bearish (the price will be inside kumo).

If D1 price will break 0.8401 support level so the primary bearish will be continuing (good to open sell trade).

UPCOMING EVENTS (high/medium impacted news events which may be affected on NZDUSD price movement for this coming week)

2014-06-08 02:30 GMT (or 04:30 MQ MT5 time) | [CNY - Trade Balance]

2014-06-09 22:45 GMT (or 00:45 MQ MT5 time) | [NZD - Manufacturing Sales]

2014-06-10 01:30 GMT (or 03:30 MQ MT5 time) | [CNY - CPI]

2014-06-11 18:00 GMT (or 20:00 MQ MT5 time) | [USD - Federal Budget Balance]

2014-06-11 21:00 GMT (or 23:00 MQ MT5 time) | [NZD - Official Cash Rate]

2014-06-12 12:30 GMT (or 14:30 MQ MT5 time) | [USD - Retail Sales]

2014-06-12 22:30 GMT (or 00:30 MQ MT5 time) | [NZD - Business NZ Manufacturing Index]

2014-06-13 05:30 GMT (or 07:30 MQ MT5 time) | [CNY - Industrial Production]

2014-06-13 12:30 GMT (or 14:30 MQ MT5 time) | [USD - PPI]

2014-06-13 13:55 GMT (or 15:55 MQ MT5 time) | [USD - UoM Consumer Sentiment]

Please note : some US (and CNY) high/medium impacted news events (incl speeches) are also affected on NZDUSD price movement

SUMMARY : bearish

TREND : ranging

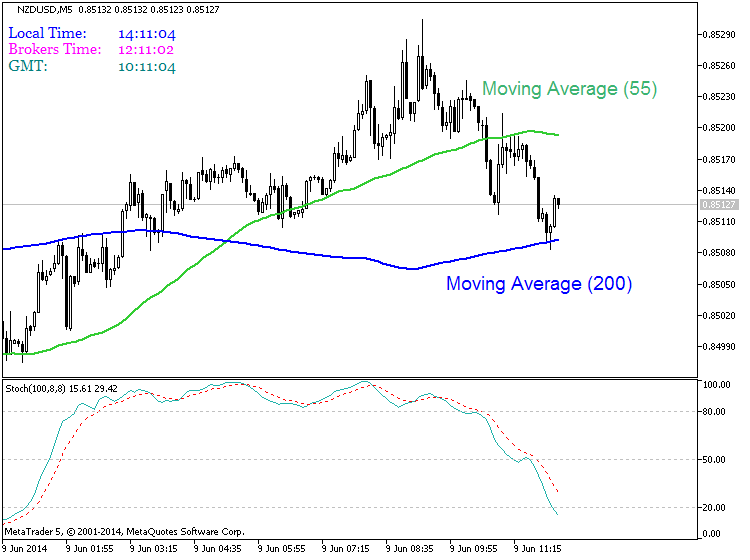

Intraday Chart