I need an experienced programmer who has specifically done this before as I am on time constraints, so respectfully only apply if you have done this successfully before thank you.

- I do have an include file and a sample EA that I have been trying to implement it on but cannot get OOS data/parameters to populate or if OOS data populates it's incorrect.

- If you wish to modify my code to get it fully working that is acceptable.

- If you wish to just start fresh and create you're own version that does rolling walk forward analysis that is fine as well.

- I need it as an include that holds all of the functions because I plan on using this with many EA's so it's need to be minimal on the EA side so it's universal and can be used easily with any EA.

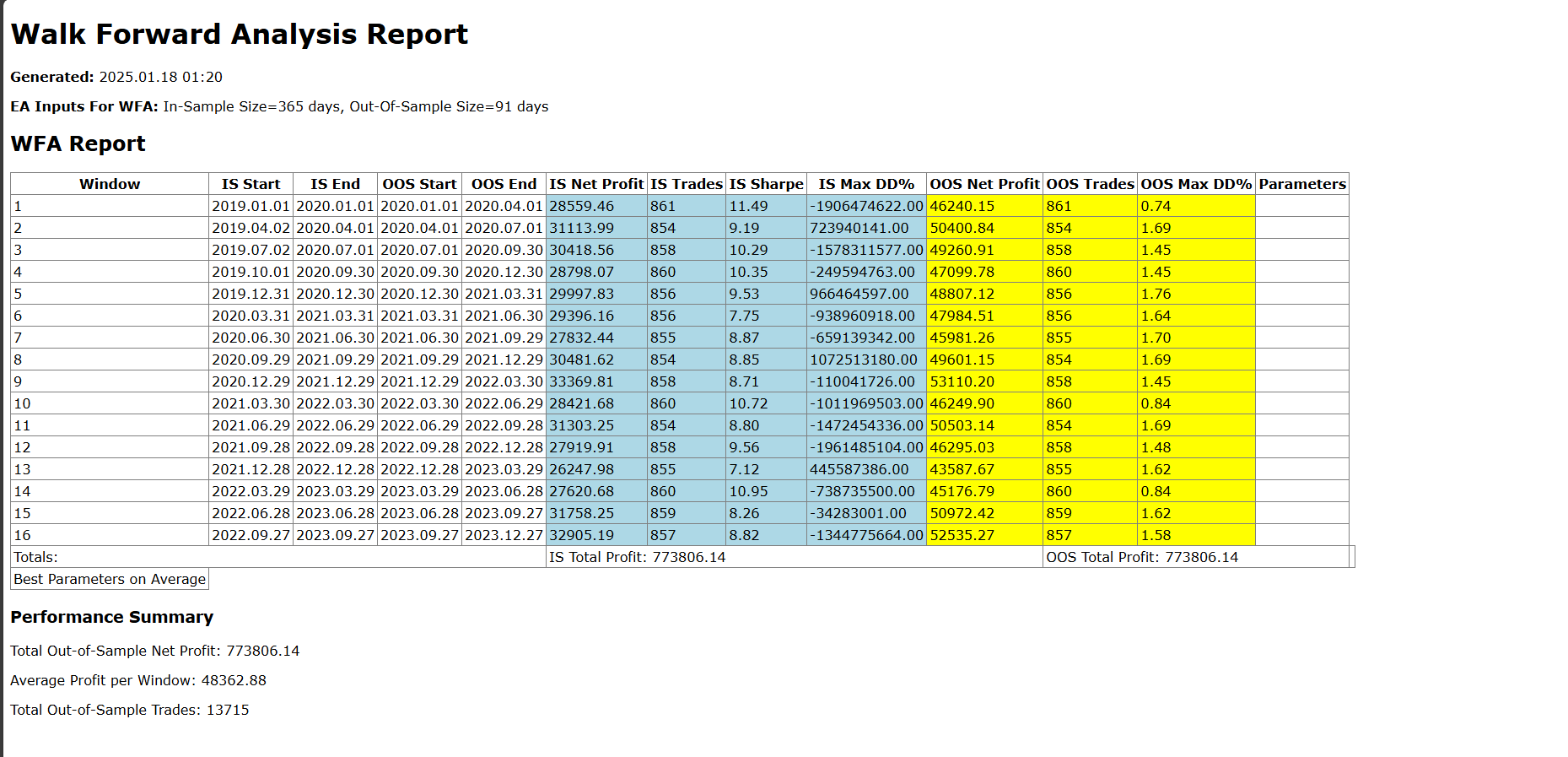

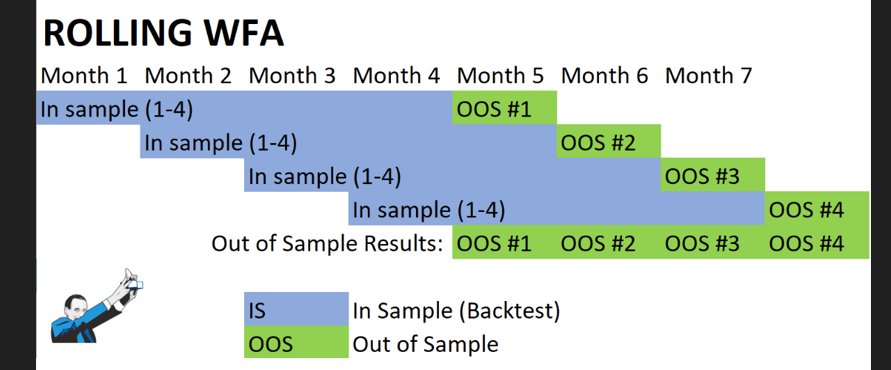

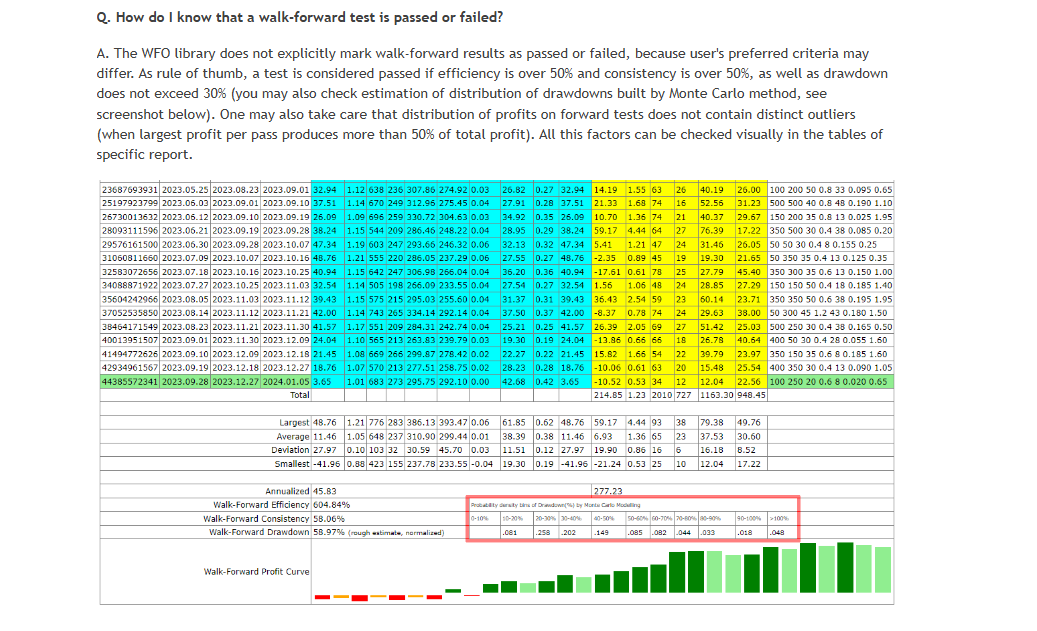

Attached is a screenshot of what mine currently produces, what an operational one looks like and a illustration of rolling WFA theory.

This was my theory framework for building the code initially:1. Decide on Your Core "Engine" Approach

When we talk about walk-forward optimization in MetaTrader, there are two main approaches to orchestrating it entirely inside the platform’s built-in tester:

“In-sample/out-of-sample in each pass”:

Let each pass of the tester trade only on a “window” (the first part of the pass) and measure performance there.

In that same pass, trade the “step” (forward test) only for measuring the out-of-sample performance, not for returning the fitness to the tester.

Return the fitness from the window portion to the tester (so the tester picks the best parameters for the window).

The library internally records the forward test performance in a CSV or other structure.

“Single full-period pass for each parameter set, then post-process the data”:

Each pass trades the entire date range (the “big” range D), and logs daily or bar-by-bar data (balance, drawdown, etc.) in a file.

After optimization completes, an offline script or library function “cuts” that entire date range into windows + steps (like W + S) for each pass, measuring them in a post-processing step.

In other words, you let the EA trade from the earliest date to the latest date. Then your library or script extracts the in-sample and out-of-sample slices (walk-forward slices) offline. This has the advantage of requiring no “meta-parameters” (wfo_windowSize, wfo_stepOffset, etc.) but has the disadvantage that the tester doesn’t actually optimize on the smaller window. It simply picks the best parameters for the entire date range. Then you filter them out in a “fake” window. This can bias the results, so the library is basically faking the rolling windows in post-processing.

Similar orders

Привіт. Шукаю когось, хто б застосував мій код як бота . Я торгую індексом Aus_200 SFE (не XJO). Бот базується на MACD входу/виходу, RSI, стохастиці та vwap. Як тільки роботу приймуть, мені потрібно внести кілька коректив; однак, нічого суттєвого. Дякую

a { text-decoration: none; color: #464feb; } tr th, tr td { border: 1px solid #e6e6e6; } tr th { background-color: #f5f5f5; } Purpose: The EA will run on a Vantage Markets MT5 account and will later be used for copy trading. Requirements: - Fully automated trading - Adjustable lot size - Adjustable Stop Loss and Take Profit - Risk management per trade - Maximum daily drawdown protection - Trading hours filter - News

Custom MT5 EA for buy stop and sell stop breakout strategy.’ ‘Requirements, develop a custom Expert Advisor for MetaTrader 5 that places buy-stop and sell-stop pending orders based on defined breakout rules.’ ‘All important values adjustable via inputs.’ ‘Includes stop loss, take profit, trailing stop, and configurable risk management.’ ‘One trade at a time, works on demo before live.’ Provide source code and

A good trend predicting indicator is the one which can identify the trend change as soon as it happens on the chart. when a new candle is formed it should tell whether its going to go up or down. I have already seen a lot of repainting trend predictors so if your indicator is repainting then please don't bother contacting. I would like to see the demo version and then if satisfied , I would want the source code too

Platform MetaTrader 5 (MT5) MQL5 Source Code Required Compatible with Exness MT5 both standard and cent accounts/ICMarket accounts Works on EUR/USD only (initial version) ⸻ Objective Develop a fully automated AI Expert Advisor based on ICT Smart Money Concepts (SMC). The EA must only execute high-probability trades that satisfy all required conditions before opening a position. The EA must avoid overtrading and

Bonjour, je recherche un développeur MQL5 expérimenté pour créer un Expert Advisor pour MetaTrader 5 basé sur une stratégie de trading intégrant des principes de gestion des risques rigoureux et d'intelligence financière. Le robot doit être capable de gérer plusieurs paires de devises et d'optimiser automatiquement les entrées et sorties en fonction de conditions de marché prédéfinies."

Hello everybody, I'm looking for an experienced MQL4/MQL5 developer to optimize a High-Frequency Trading (HFT) Expert Advisor for both MT4 and MT5. The EA performs consistently and profitably on demo accounts, but when it is run on Raw and Standard live accounts under what appear to be the same trading conditions, it begins generating losses. I do not have the original source code (.mq4/.mq5); I only have the

I'm looking for an experienced NinjaTrader 8 (C#) developer to build a fully automated futures trading strategy. Please apply only if you have proven experience developing and testing NinjaTrader strategies. Project Overview Develop a fully automated NinjaTrader 8 strategy. Designed for Apex funded and evaluation accounts. Primary instruments: NQ/MNQ Futures (with flexibility to support other futures later). Trading

I need an Expert Advisor for MT5 on XAUUSD 1min timeframe using SMC concepts. STRATEGY RULES: SELL: 1. Identify previous day High/Low as liquidity 2. Entry only during London-NY session: 15:00-19:00 GMT+3 or broker clock. 3. If price sweeps previous day High and closes back below it 4. Check for bearish 1min FVG below sweep candle 5. Wait for BOS - lower low 6. Entry: Sell/buy at 50% of the FVG 7. SL: 10 pips above

Code An Loss Rate 90-100% MT5 EA , that can blow a 100 USD account a day ,with fixed TP of 3000 points and SL of 3000 For better Rate Calculations get an strategy that can lead to so

{kind=link}

{kind=link}

{kind=link}