In the first section of this blog, the notion of diversifying a portfolio following a correlation matrix was briefly introduced. Based on this concept, the decision was made to construct a portfolio for the NEXUS expert advisor.

For those unfamiliar, this expert advisor represents a grid averaging system with lot multiplier. It is crucial to recognize that this approach entails inherent risks.

Therefore, in the development of this portfolio, 8 symbols were selected for an account of 200,000 euros. Each of them was allocated an equitable distribution of the balance, i.e., 25,000 euros per symbol.

It is noteworthy that each symbol was configured with a maximum limit of 4 to 7 open trades, after which a loss would be considered, and the trades would be closed. This approach aims to mitigate associated risks.

To counterbalance the potential adversities of one symbol with the favorable moments of another, the following currency pairs were selected: AUDUSD, AUDCAD, EURUSD, EURGBP, EURJPY, GBPNZD, USDCAD, and USDCHF. Various sets were created in which levels of Take Profit, Step, and maximum number of allowed trades (between 4 and 7) were optimized.

These sets were adjusted for a 5-year period, and the most favorable results were taken, seeking an optimal Sharpe Ratio and a number of trades that supported the validity of the analysis.

Below are the various selected sets. Please refer to the attached image for more details.

Once this preliminary portfolio was constructed, a real account was opened and the portfolio was put into action. However, it was soon observed that the losses outweighed the gains, indicating potential flaws in the portfolio concept. It had been an impulsive decision, and it was evident that a new layer of verification was needed before proceeding.

The first test conducted was to rerun the backtests on another broker, verifying the results obtained through the initial optimization process. It was quickly noticed that the USDCHF set performed well on the first broker but not on the second. Therefore, instead of falling into the trap of over-optimizing the set, it was discarded.

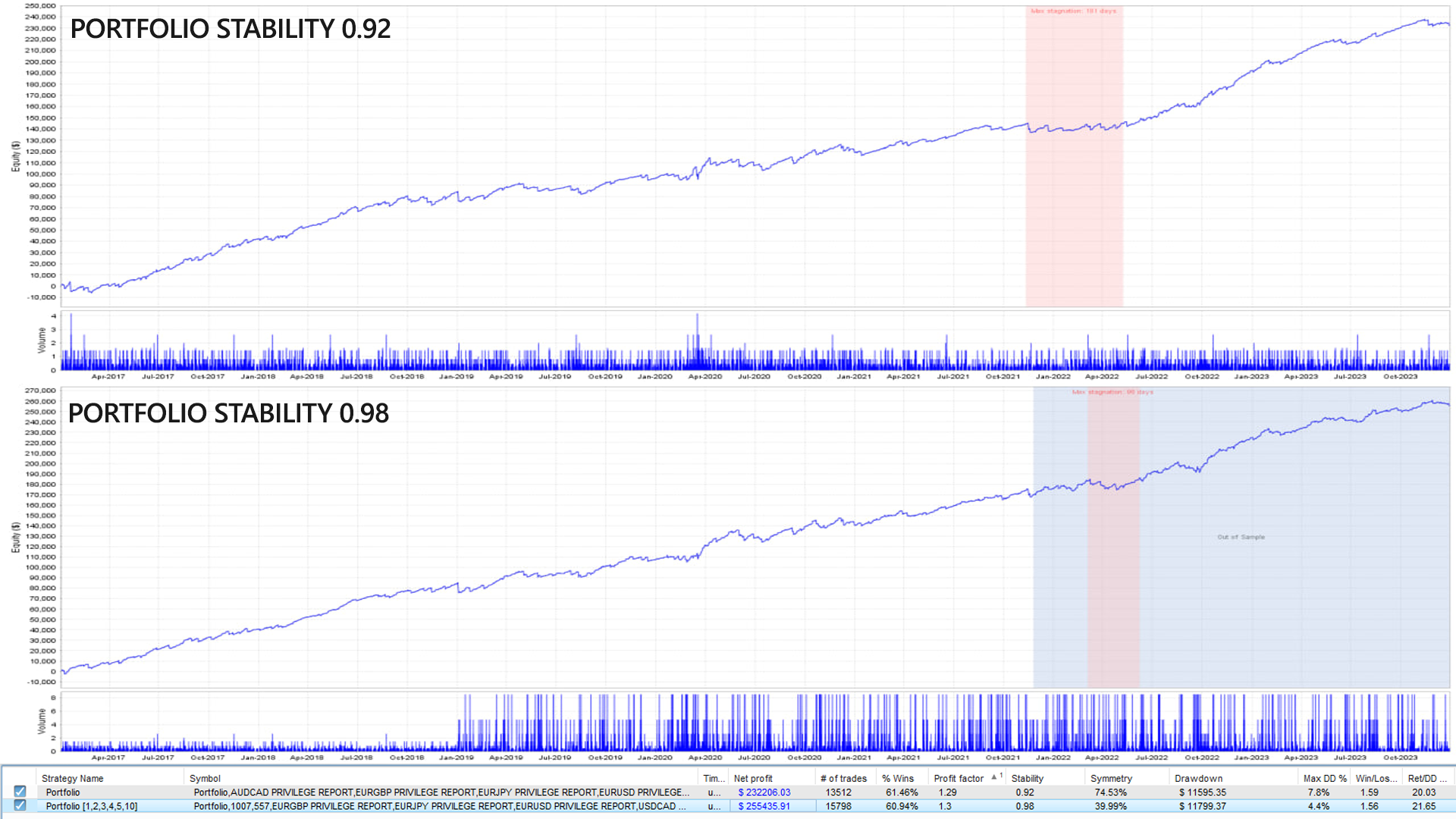

Consequently, it was decided to visualize the portfolio on a single graph and obtain additional data for a deeper analysis. The attached image provides a clear representation of these elements:

The blue curve represents the balance and shows the overall growth of the portfolio. However, one noteworthy data point in the image is the period of stagnation, evidenced by 140 days where the account experienced no growth.

Despite this stagnation, the shape of the curve was encouraging and satisfying. Nevertheless, the need to apply another layer of information to refine the system and address identified flaws was recognized.

One of the potential errors that could have been made is the excessive correlation between the different configurations and symbols within the portfolio. To address this concern, a genetic tool was used to combine the diverse results of each backtest in order to search for significant correlations.

In this context, it was established as a criterion that any resulting combination should not show a correlation exceeding 30%. After the analysis, the program suggested the exclusion of 2 of the remaining 7 sets, as the results of AUDUSD and GBPNZD showed significant correlation with the results of other symbols.

The attached image illustrates the current portfolio composition, consisting of AUDCAD, EURGBP, EURJPY, EURUSD, and USDCAD, after this selection and adjustment process. This approach aims to reduce excessive correlation between configurations and symbols, thus promoting greater diversification and robustness in the portfolio.

In the presented image, it can be observed that while the portfolio curve appears more uniform after the adjustments to reduce correlation, the period of stagnation has slightly increased to 181 days. At this point, this phenomenon is attributed to the reduction in the number of trades within the system.

Faced with this situation, the question arises as to what the next steps should be to improve and grow the system. In this regard, the idea is to detail in the next blog entry a plan to optimize a new set of strategies. This new approach will focus on basing trade exits on market hours, i.e., establishing strategies that accept losses during specific market hours and close trades outside of those intervals.

This approach aims to capitalize on market variability based on hours, allowing for more precise risk management and potentially increasing trading activity during more favorable times. In the next blog entry, this optimization plan will be detailed, and the results obtained upon implementation will be shared.

14/02/2024 UPDATE

Remember that this is a puzzle, it is not about a set being good not individually, but rather that it fits well at the level of correlation with the other pieces of the puzzle.