Join our fan page

- Views:

- 5161

- Rating:

- Published:

- 2018.11.20 12:54

-

You are missing trading opportunities:

You are missing trading opportunities:- Free trading apps

- Over 8,000 signals for copying

- Economic news for exploring financial markets

Registration Log inYou agree to website policy and terms of use

If you do not have an account, please register

-

Need a robot or indicator based on this code? Order it on Freelance

Go to Freelance

Need a robot or indicator based on this code? Order it on Freelance

Go to Freelance

The idea and the simplest algorithm are provided in the article "Random decision forest in reinforcement learning"

The library has advanced functionality allowing you to create an unlimited number of "Agents".

In addition, variations of the "Arguments group accounting method" are used

Using the library:

#include <RL gmdh.mqh> CRLAgents *ag1=new CRLAgents("RlExp1iter",1,100,50,regularize,learn); //created 1 RL agent accepting 100 entries (predictor values) and containing 50 trees

An example of filling input values with normalized close prices:

void calcSignal() { sig1=0; double arr[]; CopyClose(NULL,0,1,10000,arr); ArraySetAsSeries(arr,true); normalizeArrays(arr); for(int i=0;i<ArraySize(ag1.agent);i++) { ArrayCopy(ag1.agent[i].inpVector,arr,0,0,ArraySize(ag1.agent[i].inpVector)); } sig1=ag1.getTradeSignal(); }

Training takes place in the tester in one pass with the parameter learn=true. After training, we need to change it to false.

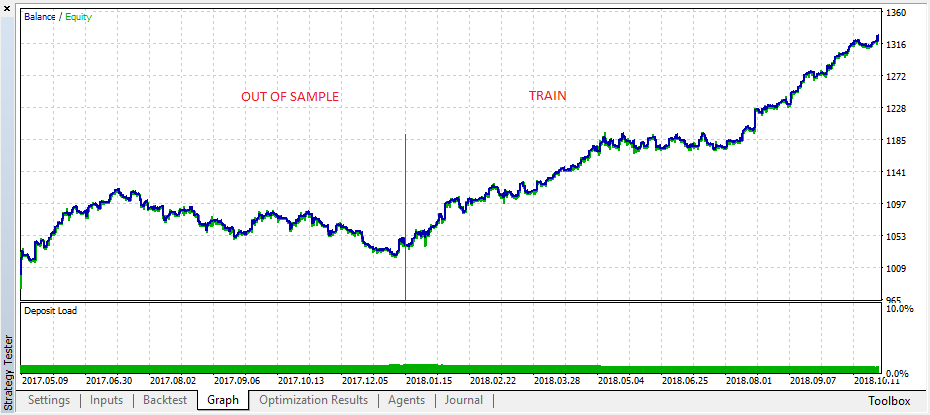

Demonstrating the trained "RL gmdh trader" EA operation on training and test samples.

Translated from Russian by MetaQuotes Ltd.

Original code: https://www.mql5.com/ru/code/22915

Contrarian trade MA

Contrarian trade MA

Working by iMA (Moving Average, MA) and OHLC of W1 timeframe

Exp_XFisher_org_v1

Exp_XFisher_org_v1 Expert Advisor based on XFisher_org_v1 oscillator signals.