To generalize the economic problems of Europe, focus on demand: the lack

thereof. In essence, Europe is relying on the European Central Bank to

add incremental growth but the logic of growth without demand is

illusory at best. The ECB’s latest stimulus plans seem as impotent as

previous programs such as the much maligned OMT. Add to this the fact

that ECB Head, Mario Draghi, did not seem his hyper confident self at

his last press conference where he announced the details of the Asset

Backed Securities purchase program. Again, the ECB has demonstrated that

after hand wringing and institutional-speed (molasses-like…)

deliberations, the ECB will act. The question is whether anything the

ECB does now is sufficient and whether monetary policy at all, can be

counted on to spur economic growth rather than just financial asset

price increases.

At this point of the Eurozone economic cycle, the bad news about ECB

comes in two varieties: that whatever the new stimulus program, the

magnitude will not be large enough; and/or, the real problems with the

Eurozone are fiscal and political. The former is entirely negative

because it may prove that final demand, in the current state of the

Eurozone cannot be stimulated by monetary policy. The latter is

self-evident and far harder to implement, solve or promote across

disparate economies that are part of the EZ.

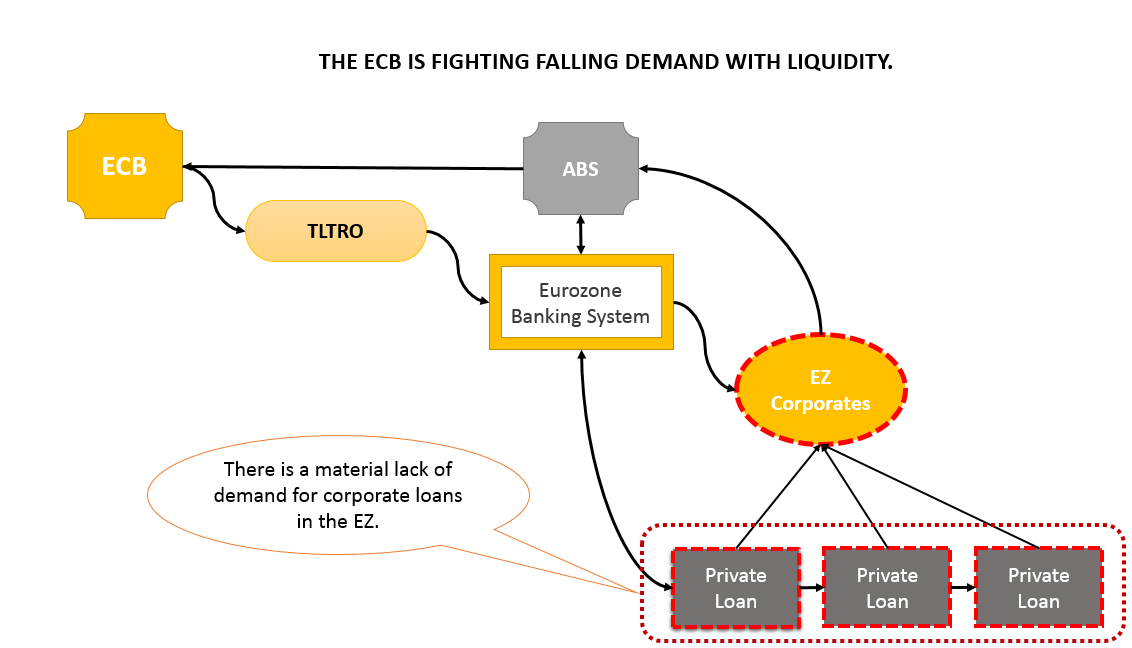

The ECB must know that investor realization of monetary sterility may, in and of itself, further clog transmission mechanisms and banish any existing animal spirits. That would logically decrease already weak Eurozone final demand. The also recently announced Targeted Long Term Refinancing Operation consisting of a total of $400 billion Euros to EZ banks at an interest rate of 0.15% (i.e., virtually free) was a notable failure in that only €82.6 billion has so far been requested. Remember, the “T” in the LTRO stands for “Targeted” and thus unlike the first LTRO versions this program requires EZ banks to on-lend this capital via loans to private companies. What a halcyon thought: that large companies and SME’s within the Eurozone would like to borrow money so they can expand their companies in order to make more money. The facts do not point to that demand quotient however. European companies are simply not applying for loans.

To illustrate the point, lending to businesses fell

€1 billion in August from July event though M3 money supply was up 2%

in the same period. As it relates to the Eurozone and these ECB efforts

it is useful to keep the following in mind because of the potential

for a continued and further divergence between real economy effects and

asset prices:

- Banks are less likely to load up on new loans, even if credit risks are completely covered by TLTRO funds, prior to the completion of the ECB’s “Asset Quality Review” (“AQR”) of European banks. Surveys suggest that EZ banks are likely to draw on €175 billion of TLTRO funds in the December tranche. This rationalizes the idea that the AQR will act as a damper to higher acceptance of TLTRO by the banks until the AQR is completely over.

- Both of the TLTRO and the ABS programs show that the most powerful investment driver in the Eurozone continues to be the run up to an actual ECB announcement. That is, the old mantra of “buy the rumor, sell the news” seems to continue. Therefore, watch for what is next. Perhaps either excessive nervousness or relief over the AQR?

- The ECB’s goal is to stoke inflation back towards the acceptable 2.0% level. The relationship between private sector loan growth and inflation cannot be ignored. With private sector loans in the Eurozone contracting by 1.8% over the past two years, it is not clear how slowing the shrinkage of loans will equate to inflation. The more realistic reading of recent ECB efforts may be of stabilization rather than viewing them as growth propellants.