Société Générale: Greenback ceased to be safe haven, it is rather a barometer of global mood

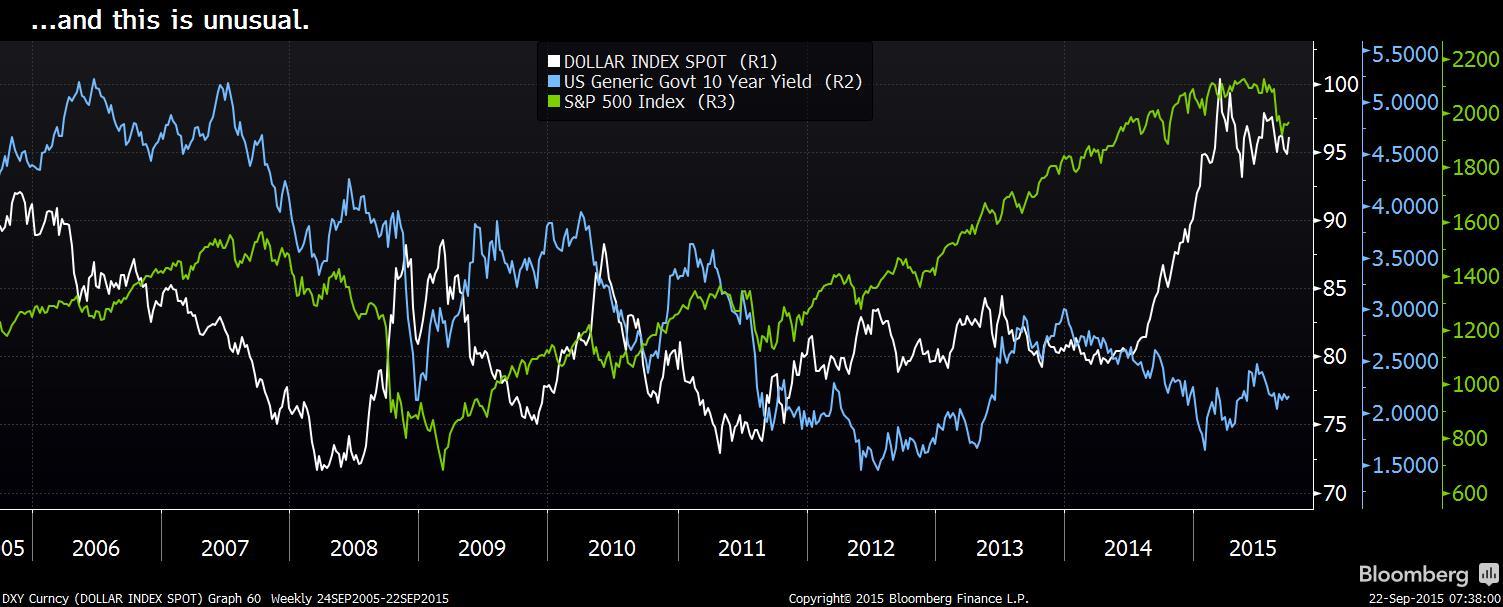

Kit Juckes, global strategist at Société Générale, has noted that for the past two months, the movements of the world's reserve currency - the U.S. dollar - have been extraordinary.

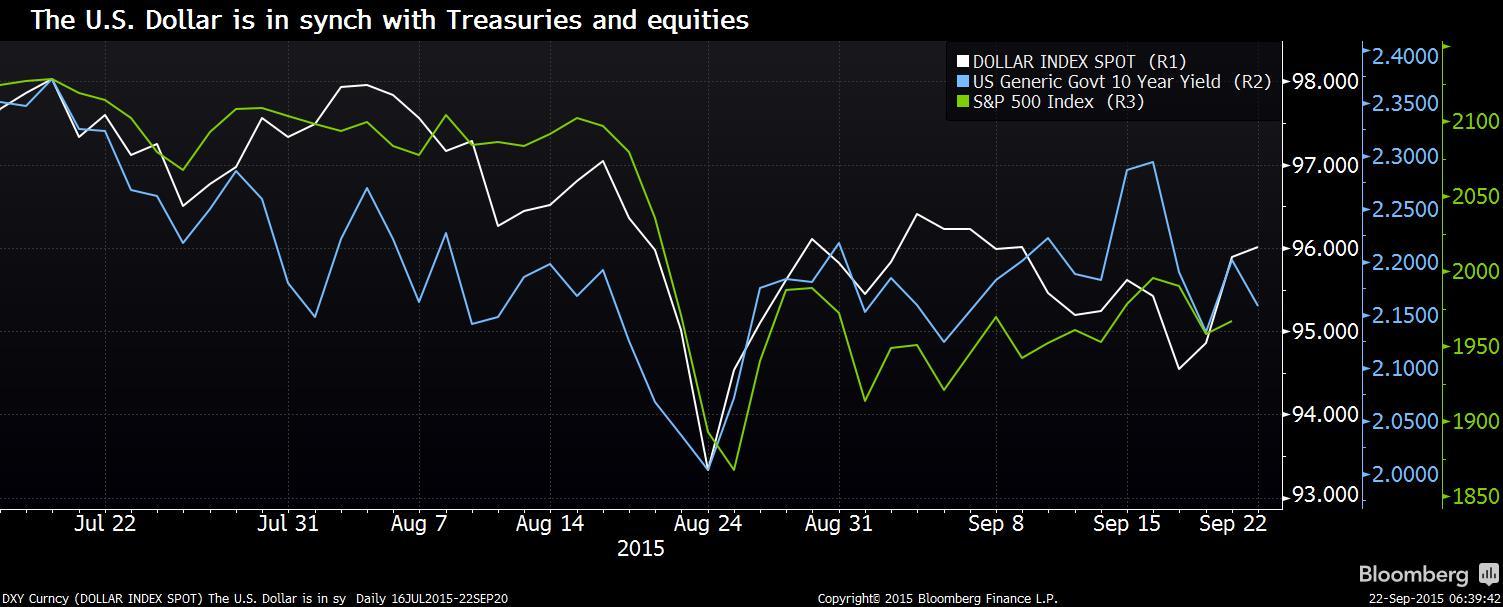

The greenback has been correlating with both stocks and bond yields since mid-July:

Over the past two months, on days when equities and yields rise, the U.S. dollar has tended to gain relative to a weighted basket of the euro, yen, pound, Canadian dollar, Swedish krona, and Swiss franc.

And Juckes thus notes that the dollar has lost its status as a funding or safe haven currency. "Instead, it is a barometer of the global mood."

Positioning provides a hint as to how the greenback managed to reinvent itself: mostly, market players have been net long the dollar and the S&P 500 gauge while short U.S. Treasuries in 2015. This is a far cry from how the U.S. dollar was treated a few years ago and how it has historically been viewed.

Usually, during stressful times, traders rush to the world's reserve currency. That didn't occur during August's carnage, at least for the currencies in the DXY index.

A calming factor in this instance

is that the upheaval has been capped to financial markets, rather than

the real economy.

In the event that economic conditions were worsening significantly around the world (i.e. widespread contractions, not only slower growth), the dollar could potentially regain its safe-haven status.

And in the aftermath of the Great Recession, which triggered a high degree of unconventional monetary policy in response, the softer U.S. dollar, lower bond yields, and shrinking growth outlook drove a pickup in the use of the U.S. currency as a funding one. That is, market players would sell U.S. dollars and use the proceeds to purchase higher-yielding foreign assets in what is commonly known as a carry trade.

Due to the fact that longer-dated U.S. Treasuries

command a substantial premium relative to most debt denominated in other

major currencies, the euro has largely forced out the greenback in its role as a funding currency.

Currently, further dollar strength depends "on both longer-dated U.S. yields and equities rising," wrote Juckes.

That is possible in a subdued trade. But if we take more risk-averse markets, the greenback will hardly outperform the yen and euro, "even as all three do well against everything else."