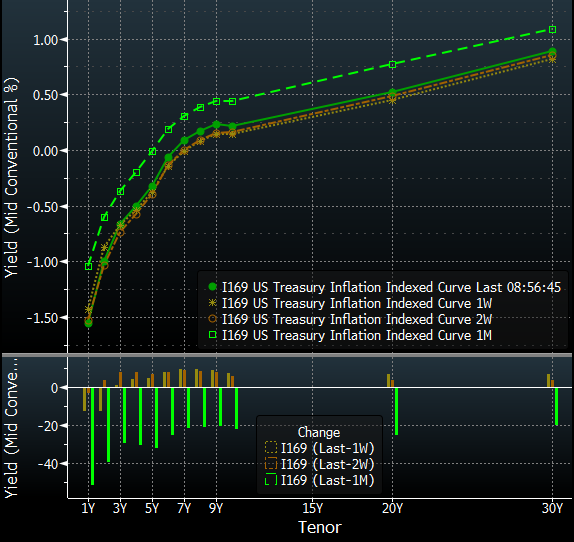

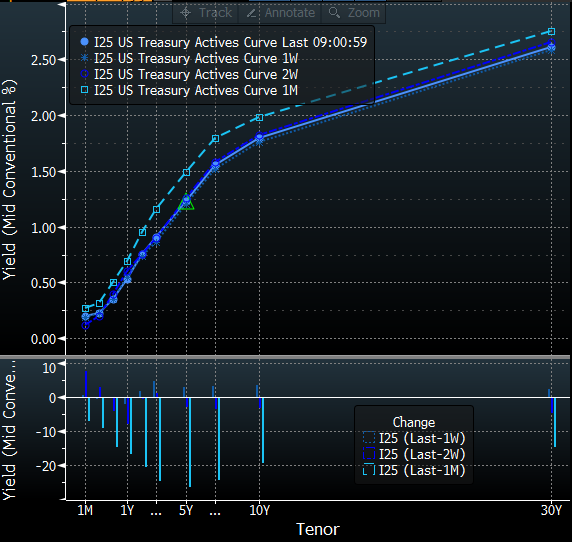

Treasuries saw decent-sized 7-year-led losses Tuesday after having rallied to just above the February lows in yields late last week and then having held near there the prior couple trading sessions. Losses were part of a broader riskon trade seen also in a 1.0% rally in the S&P 500 and 2 bp tightening in the IG CDX index, as market sentiment was boosted by a 4.5% rally in oil prices to a five-month high above $42 a barrel for front-month WTI on reports of an OPEC/Russia production freeze agreement coming together and also the first rise in dollar/yen in eight trading sessions, a slight rebound to 108.5 after a drop from 112.6 on March 31 to 107.9 on Monday. Despite the upside in oil prices and stocks and another drop in the trade-weighted dollar, TIPS performed badly again, with all of the rise in nominal yields coming in real rates, as not quite as flat a Fed rate outlook in futures apparently added to expectations that 2% PCE inflation is never going to be achieved. Domestic economic news was light again ahead of a number of key reports in the next few days, in particular retail sales on Wednesday and CPI on Thursday, so U.S. rates markets were mostly focused again on overseas market developments while preparing for supply, which started with a solid 3- year Treasury auction Tuesday and continues with 10-year and 30-year auctions the next two days. The overall bid/cover at the 3-year auction of 2.72 was little changed from the last two months, making for a run of seven-year lows. That’s reflected a continued trend down in primary dealer auction participation. Dealers bid enough to cover the auction 1.9 times, so it wasn’t like there was any concern about a failed auction or anything, but that was down from close to 2.5 at the April 3-year auctions in each of the prior four years. Increasing pressure on balance sheets has contributed to substantially less dealer demand like that across Treasury auctions at all maturities in the past year, a trend that probably isn’t going away and could start to be more of a concern for the Treasury Department’s debt managers if it continues. Generally recently, however, and Tuesday’s auction, there’s been healthy demand from investors to take up the slack from dealers. The combined indirect (56.0%) and direct (11.5%) bidder share of 67.4% was one of the highest on record for a 3-year auction, and the 0.890% auction award was near the cheapest levels of the day, but slightly stronger than the 1:00 WI yield. At 3:00, benchmark nominal Treasury yields were 3.5 to 6 bp higher, which left them 7 to 14 bp above the February 11 lows after what’s now been a 12 to 28 bp rally since the March 15 close ahead of the FOMC meeting. The 2-year yield rose 3.5 bp to 0.74%, 3-year 4 bp to 0.88%, 5-year 6 bp to 1.21%, 7-year 6 bp to 1.53%, 10-year 6 bp to 1.78%, and 30-year 4.5 bp to 2.61%. Just about all of that upside in nominal yields came in real rates, with TIPS performing quite poorly for a second day compared to higher oil and gas prices and a lower dollar. The 5-year TIPS yield rose 5 bp to -0.34%, 10-year 6 bp to 0.21%, and 30-year 5 bp to 0.89%. There hasn’t been a sharp renewed turn down, but the recovery from the February historic lows in breakevens that received solid boosts from the FOMC meeting and Chair Yellen’s speech has stalled out over the past couple weeks despite the ongoing recovery to new highs for the year in oil prices and the continued correction in the dollar. From an ex crisis record low of 1.18% on February 11, the 10-year breakeven in constant maturity yield terms got as high as (a still very low) 1.65% on March 30, a day after Yellen’s speech, but is at 1.57% now. The 5-year/5-year forward inflation swap rebounded from 1.82% to 2.11% and is now at 2.02%. Our desk saw a continued recent trend of better real yield selling Tuesday, and investors seem wary of Thursday’s CPI report and apprehensive about taking down the 5-year TIPS auction next week.