|

5+ años

experiencia

|

0

productos

|

0

versiones demo

|

|

0

trabajos

|

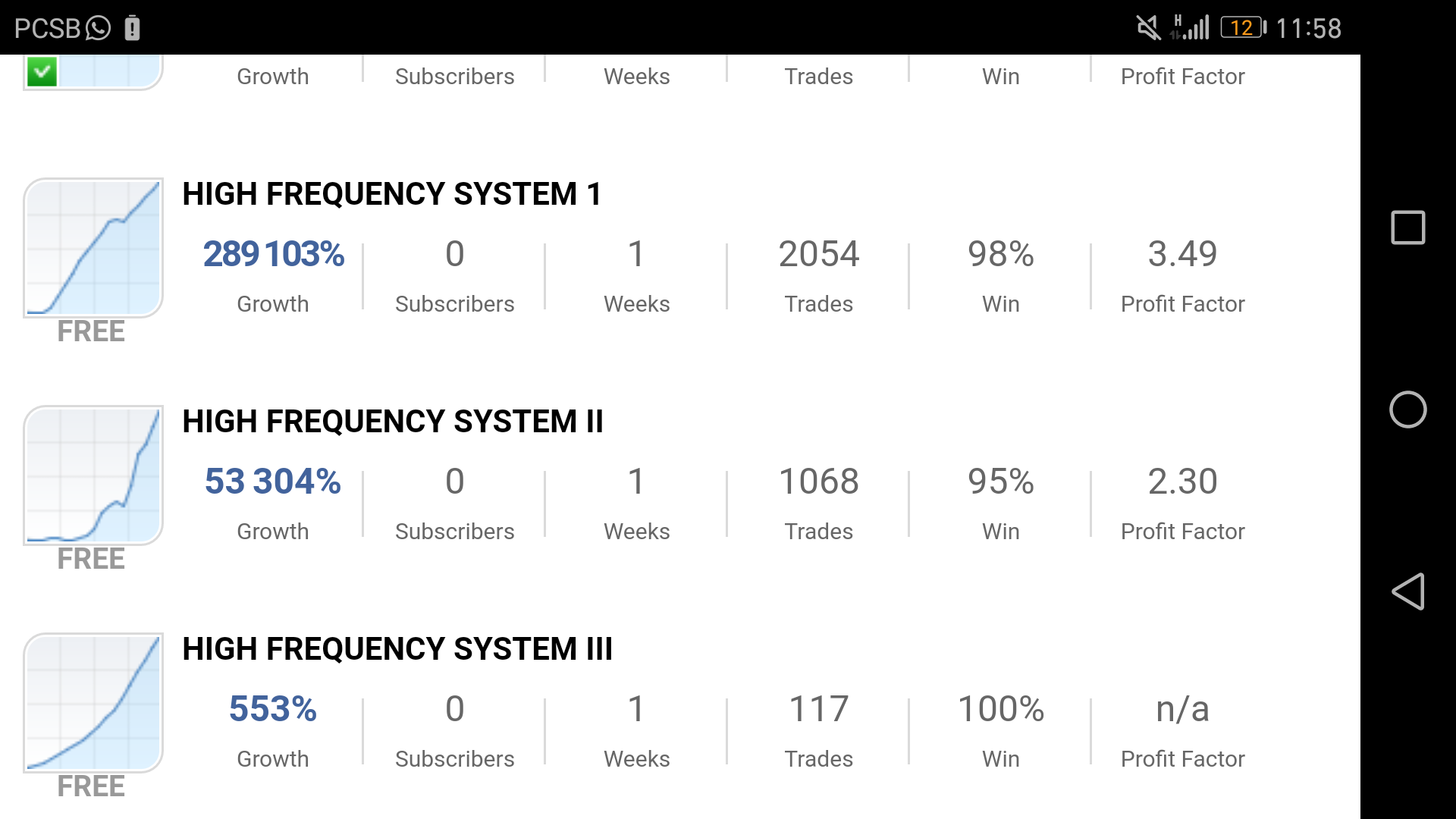

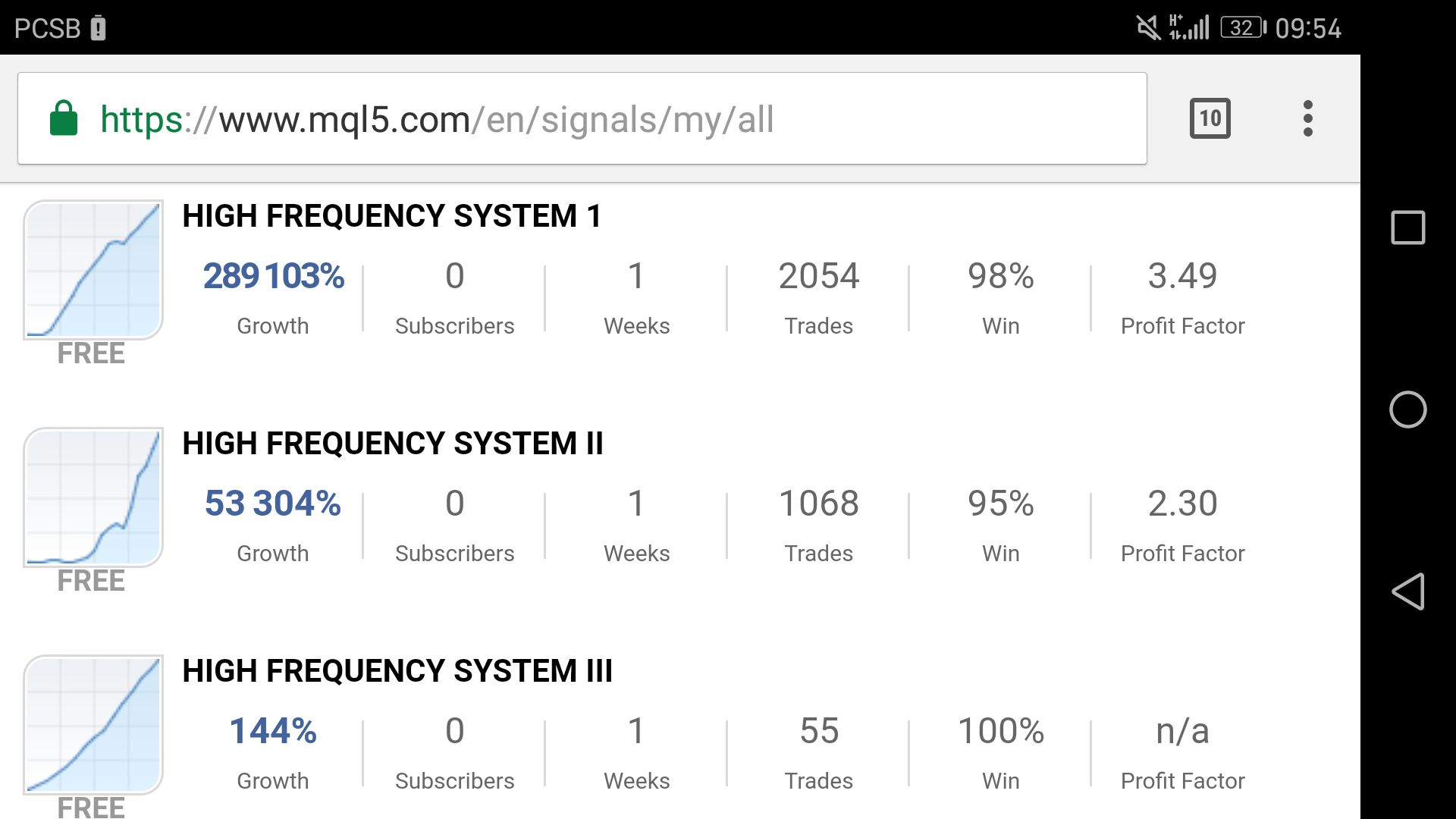

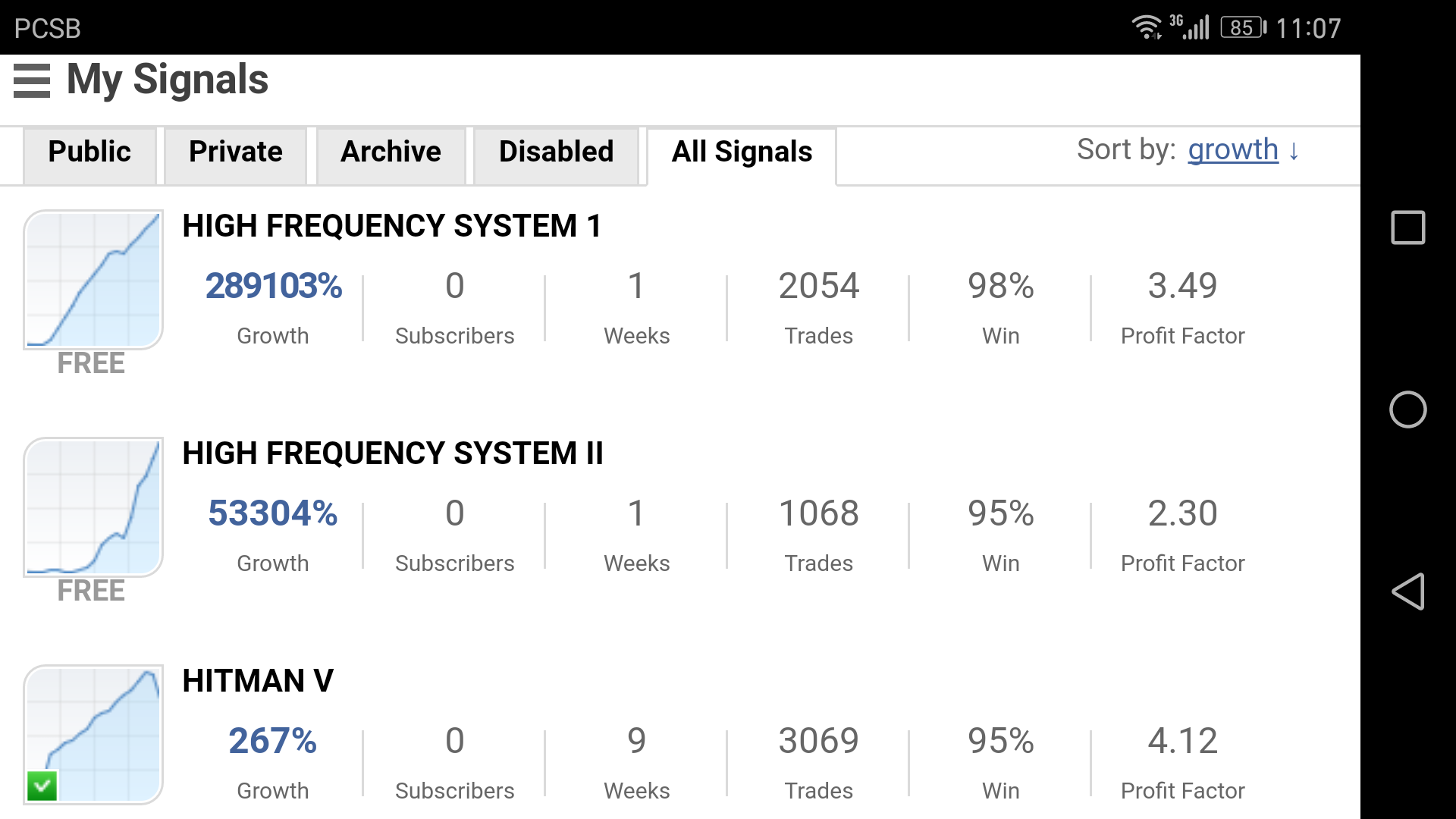

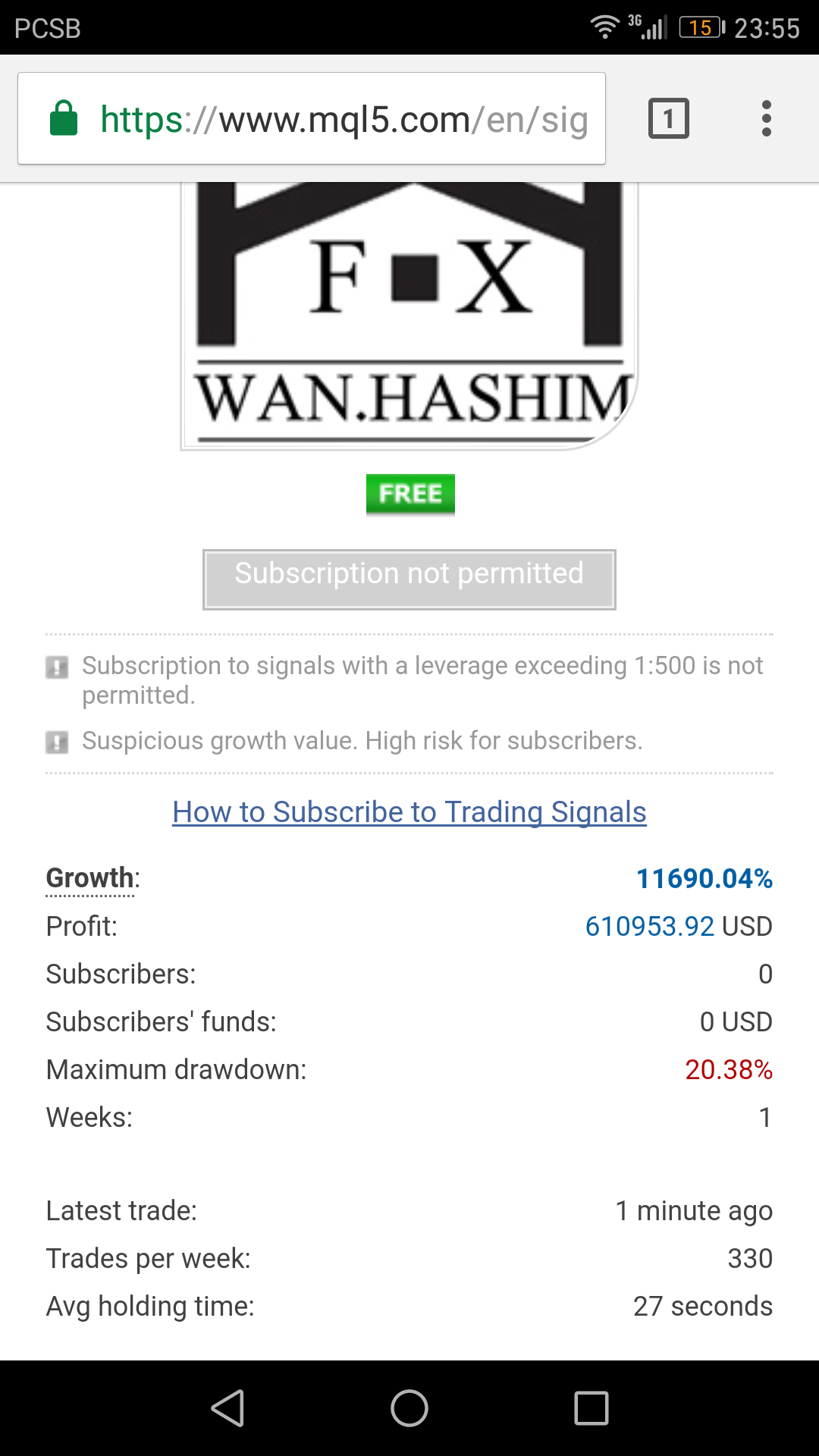

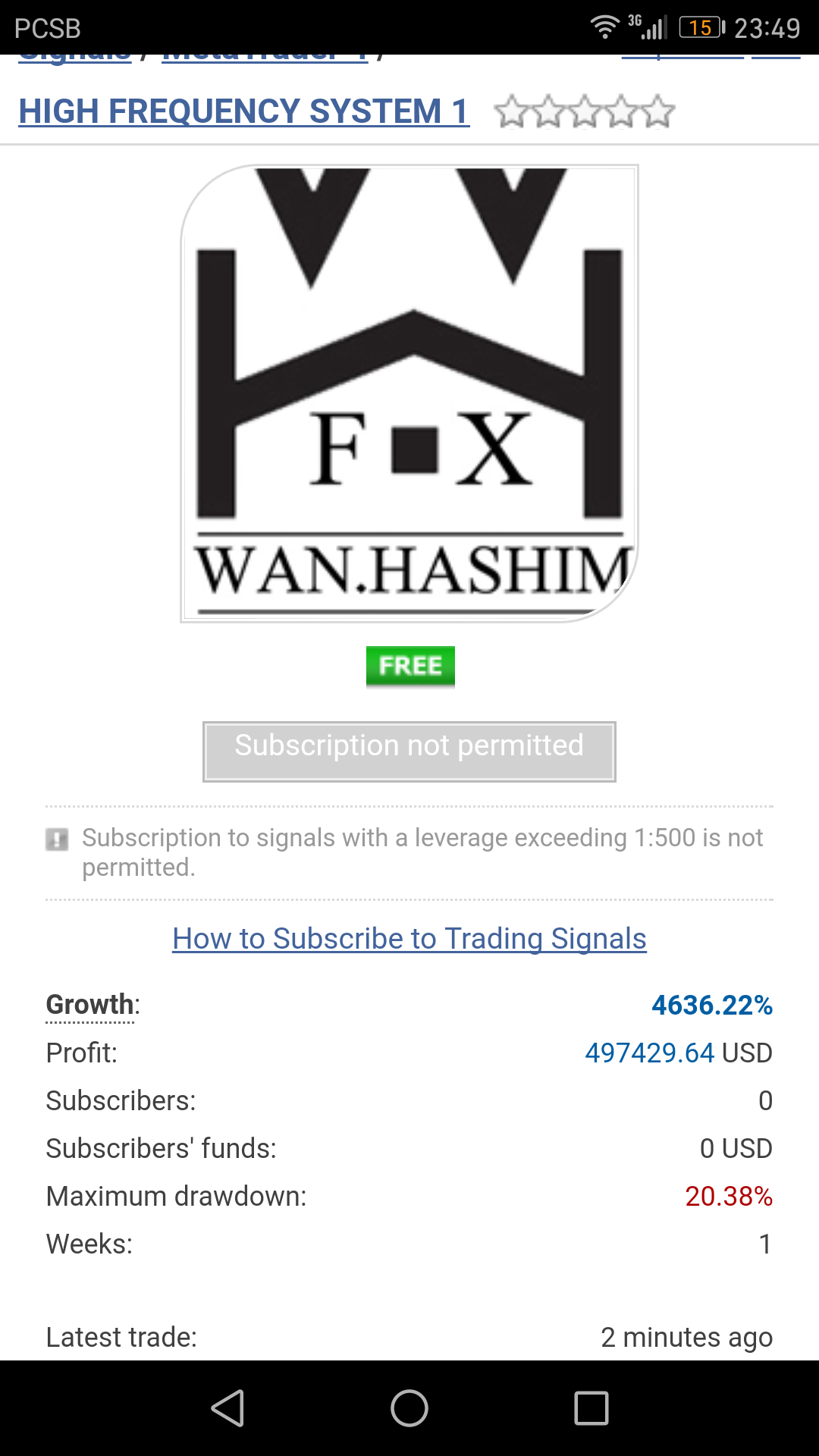

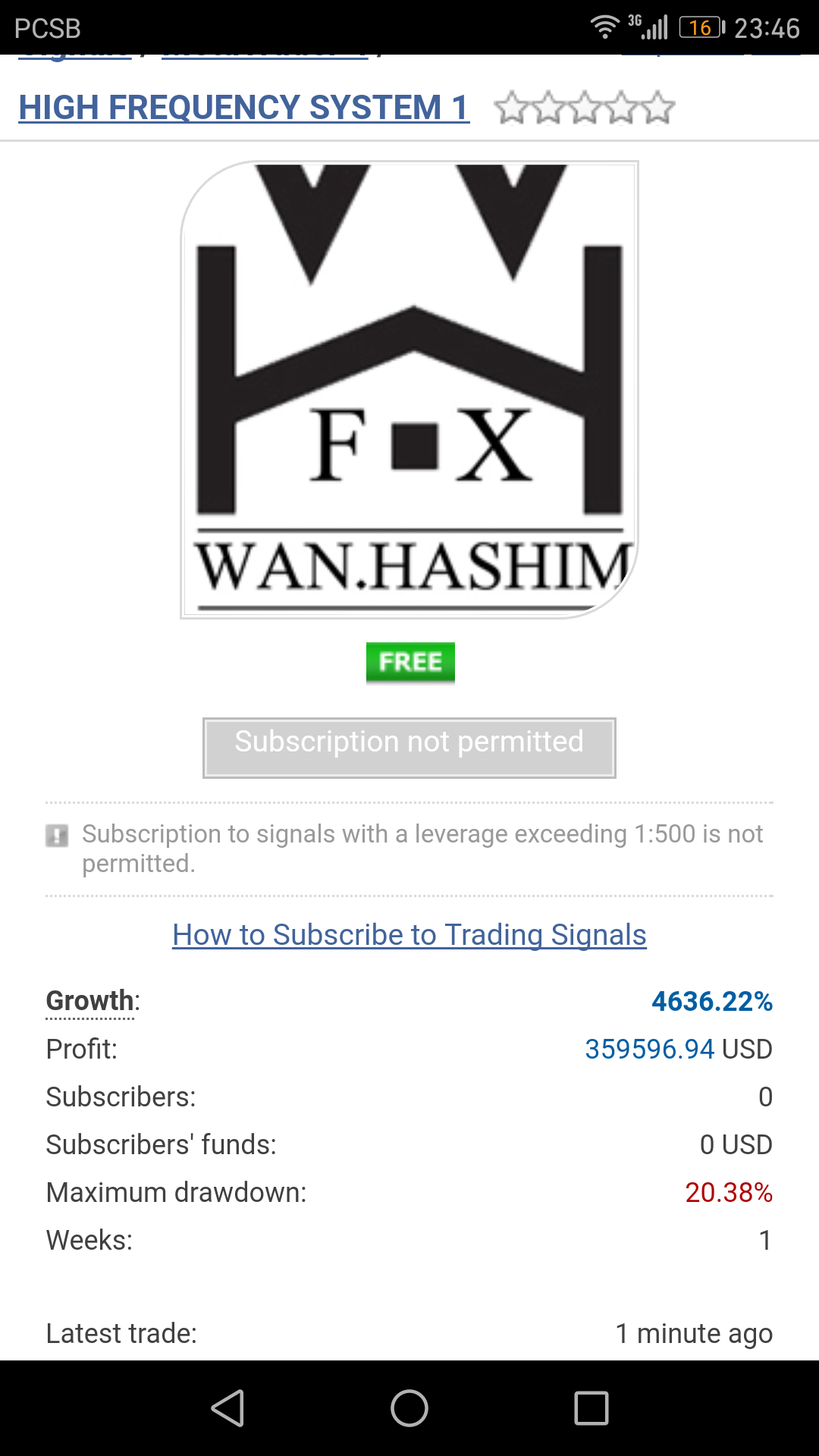

0

señales

|

0

suscriptores

|

Pg Md Radzuan Pg Hashim

· 1

[Eliminado]

2017.03.12

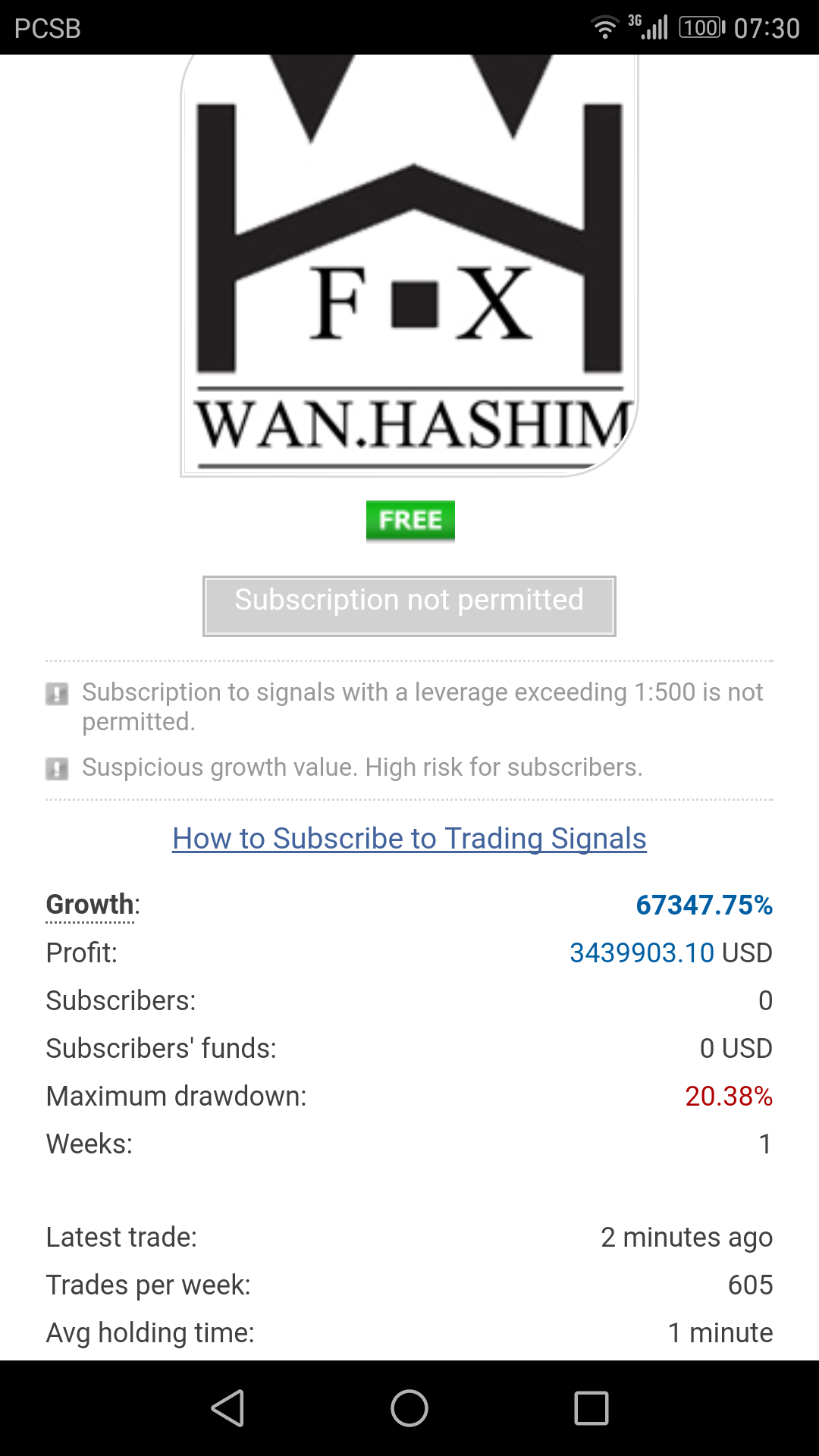

This is Demo Account, please try it with Real Account. Thank you.

Pg Md Radzuan Pg Hashim

· 5

Pg Md Radzuan Pg Hashim

2017.01.25

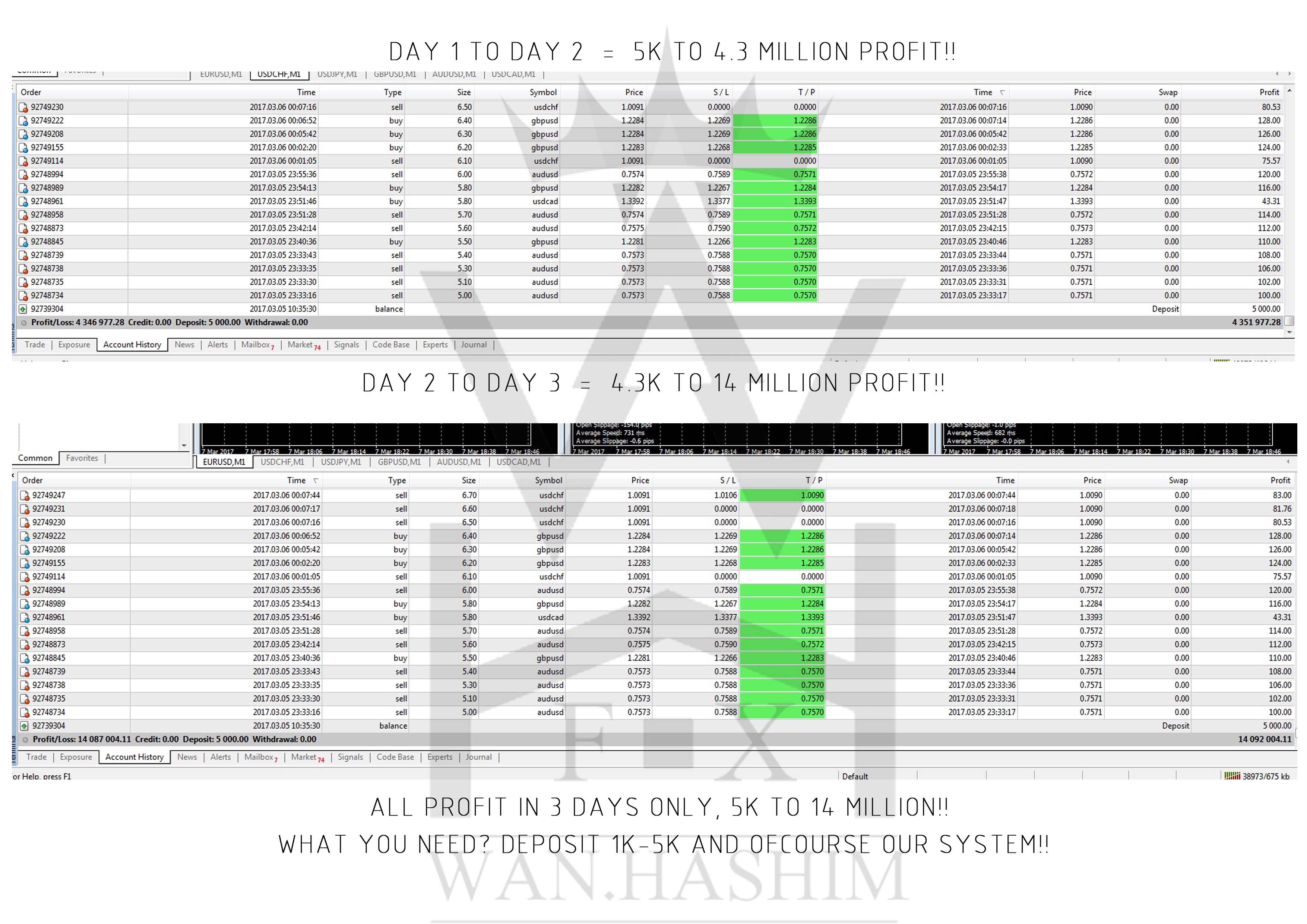

No more looking for other system, This system consider Holy Grails!!!